Investors in shares must expect market shocks as part of the long-term benefits of owning part of a company. Over time, stock markets fall one year in every five. History provides a valuable guide to how markets normally recover from shocks, and this article illustrates some of the dangers of exiting equities and not reentering.

However, it must be acknowledged that coronavirus did not start as a financial shock, such as a rapid fall in share prices or a market collapse such as the GFC or tech wreck. This started as a social and health scare and has spread into financial markets, which might limit what history can teach us. As supply chains close and countries shut their borders, the wealth created by globalisation will be compromised, and with it, economic growth and business activity.

Morningstar has prepared a series of slides based on US data which show market recoveries and some basic investing principles, and we have selected the following four highlights.

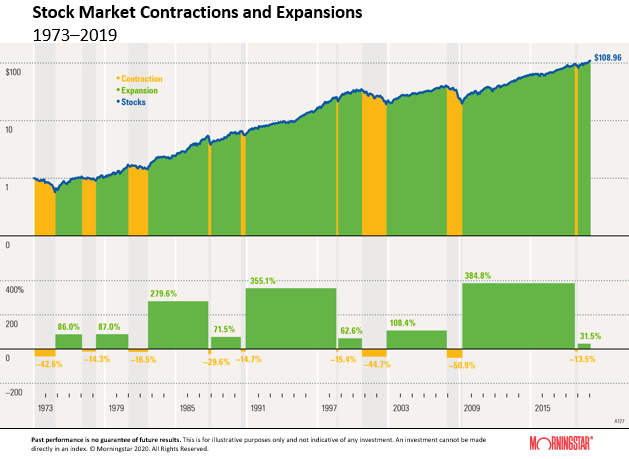

1. Stock market contractions and expansions

The stock market moves in cycles with periods of contraction followed by periods of expansion. There have been eight market downturns in the past 47 years. The regions shaded in orange below highlight a contraction phase of a stock market cycle, and the green regions show an expansion phase. A contraction is defined as a period when the stock market value declines from its peak by 10% or more.

These declines seem to happen at random and last for varying time periods. Expansion measures the recovery of the index from the bottom of a contraction and the subsequent performance of the index until it reaches the next peak level before another 10% decline.

While some periods of decline have been severe, the market has increased over time. For instance, the stock market fell by 14.7% from its peak at month-end May 1990 to its trough in October 1990 but grew by 355.1% from November 1990 to its next peak in June 1998.

No one can predict market declines with certainty. Investors should have a long-term investment horizon to allow their investment to grow over time but returns from stocks are not guaranteed.

Note: Large stocks are represented by the Ibbotson® Large Company Stock Index. The data assumes reinvestment of all income and does not account for taxes or transaction costs.

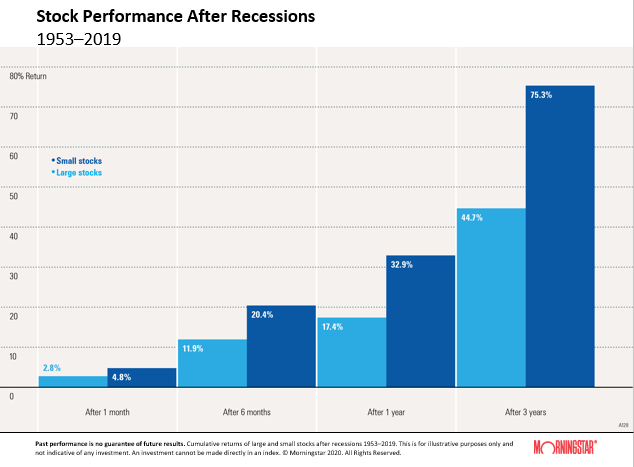

2. Stock performance after recessions

History reveals that small stocks have been among the strongest performers after recessions. Many investors fear the volatility of small stocks, but the potential of this asset class should not be ignored. The chart below shows that, on average, the cumulative returns of small stocks outperformed those of large stocks one month, six months, one year, and three years after the end of a recession.

Diversification does not eliminate the risk of investment losses. Stocks are more volatile than other asset classes. Furthermore, small stocks are more volatile than large stocks and are subject to significant price fluctuations and business risks and are thinly traded.

(On the data, the average cumulative returns are calculated from the end of each of the 10 recessions in U.S. history since 1953. The National Bureau of Economic Research defines a recession as a recurring period of decline in total output, income, employment, and trade, usually lasting from six months to a year and marked by widespread contractions in many sectors of the economy).

Note: Large stocks are represented by the Ibbotson® Large Company Stock Index. Small stocks are represented by the Ibbotson® Small Company Stock Index.

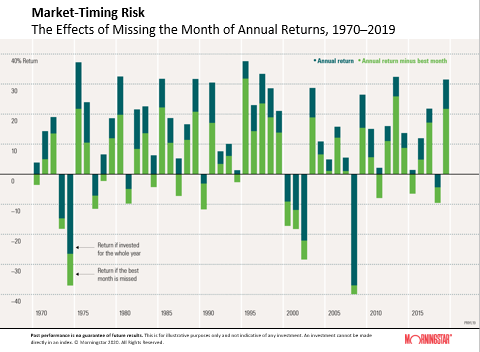

3. Risk of missing the best month each year

Investors who attempt to time the market run the risk of missing periods of exceptional returns, compromising an otherwise sound investment strategy.

Missing the one best month during a year drastically reduces returns in this chart. During years when returns were already negative, the effect of missing the best month exaggerates the loss for the year. In seven of the 49 years shown -1970, 1978, 1984, 1987, 1994, 2011, and 2015 - otherwise positive returns would have been dragged into negative territory by missing the best month.

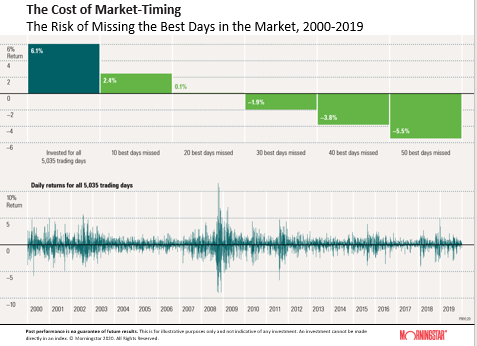

4. Risk of missing the best days over the long term

Investors who attempt to time the market run the risk of missing periods of exceptional returns. The following chart illustrates the risk of attempting to time the stock market over the past 20 years by showing returns if investors had missed some of the best days in the market.

The bottom graph illustrates the daily returns for all 5,035 trading days in the sample.

Investors who stayed in the market for all 5,035 trading days achieved a compound annual return of 6.1% from 2000 to 2019. However, that same investment would have returned 2.4% had the investor missed only the 10 best days of stock returns.

Further, missing the 50 best days would have produced a loss of 5.5%. Although the market has exhibited volatility on a daily basis, over the long term, stock investors who stayed the course were rewarded.

The appeal of market-timing is obvious. Investors want to improve portfolio returns by avoiding periods of poor performance. However, timing the market consistently is extremely difficult, and unsuccessful market-timing (the more likely result) can lead to a significant opportunity loss.

Note: Stocks in this example are represented by the Ibbotson® Large Company Stock Index.

The overall lessons are:

- Timing the market is extremely difficult and likely to lead to suboptimal performance

- The safest way for an investor to gain from the long-term benefits of investing in equities is to stay invested over time

- Responding to short-term falls may mean exiting at the wrong time and struggling for a reinvestment point

- Although recessions and market falls can be painful, so is missing the subsequent recovery.

Graham Hand is Managing Editor of Firstlinks. All data is supplied by Morningstar. This article is general information and does not consider the circumstances of any investor.