The Weekend Edition includes a market update (after the editorial) plus Morningstar adds links to two highlights from the week.

China. Whenever we include that word in an article headline, we know it will not be the most viewed. Maybe it's because few readers hold direct Chinese investments, but there are many levels in which China is fundamental to our economic and investment success. As China faces challenges to its economic growth, health and demographics, the impact on Australia will be profound.

Consider these six snapshots:

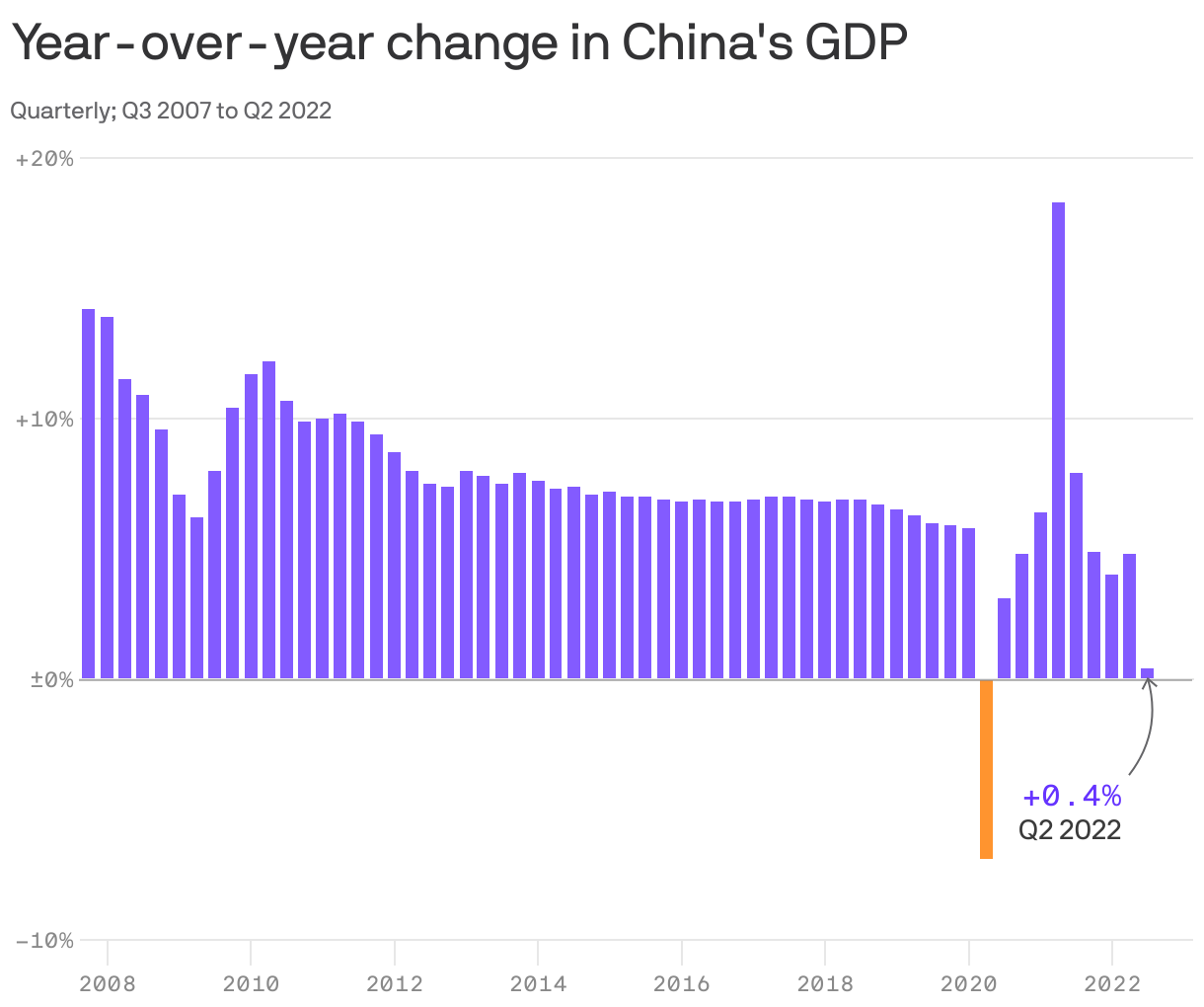

1. Not long ago, markets were worried if Chinese GDP growth fell below 8% a year. Look at the chart below. While China was expected to take a hit at the start of the pandemic in 2020, in the latest quarter, over two years later, economic growth is flat, with implications for Australia's exports to our biggest trading partner. The cheap labour that moved by the million from rural areas to the city to work in factories now costs more than many other low-cost countries.

2. For many decades, the strength of the ruling Chinese Communist Party was based on the ability to raise its population out of poverty. But with economic growth stalling, President Xi is shifting the source of his legitimacy to a national pride and military strength which means more confrontation with the West. The trip this week by US House Speaker Nancy Pelosi to Taiwan led to a cyber attack which crashed Taiwanese websites, while China launched 'targetted military operations' and placed a ban on 100 Taiwanese brands. Russia and North Korea sided with China. Former ADF Chief Angus Houston says Australia is currently facing the worst security conditions he has seen in his lifetime.

3. While the rest of the world moves on from Covid by learning to live with it, China's strict Covid Zero causes a severe loss of productivity and disrupts supply chains each time there is a major outbreak. Xi's arrogance in using only ineffective Chinese vaccines has made the country vulnerable, such as millions of people locked down recently in the manufacturing hub of Shenzhen. Manufacturing surveys show small and privately-owned businesses are suffering from weaker domestic demand. Much of the world now realises it cannot rely on cheap supply chains starting in China.

4. China is massively challenged by its demographics. In his new book, Tomorrow’s People: The Future of Humanity in Ten Numbers, Paul Morland says like many other countries, China's population in declining and the reversal of the one-child policy is having little success. India will soon be the world's most populous country. Says Morland in The Sydney Morning Herald:

"China already has a higher mean age than the United States and is getting old very quickly. If China wanted to keep its population young through migration, it would have to suck in the youth of the world ... China has probably had the world’s largest population since it became a state. This is the first time it will be surpassed for thousands of years. And it will be hit by a demographic tsunami in the coming years. In any case, China was heading for a big slowdown: look at the fall in fertility rates among Chinese communities outside China – Taiwan, Singapore, Malaysia. A society like China, which rapidly urbanised and developed and got educated, was bound to have a sharp fall in fertility rates. It would be a bit less sharp and dramatic had there been no one-child policy, but it would have been a problem anyway. Now, a slightly worse problem than would otherwise have imposed itself will be entirely blamed on the Communist Party for its heartless policy. And any efforts now from the Communist Party to reverse course and get people to have more children will have little credibility."

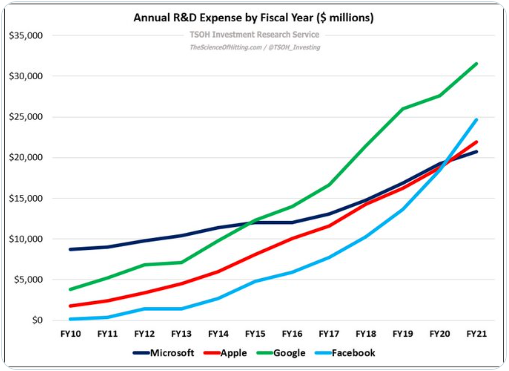

5. Until a couple of years ago, the big China tech stocks like Alibaba, Tencent (owner of WeChat), China Mobile, Baidu and JD.com were considered likely future rivals to the US giants. In 2020, the float of Ant Financial was expected to raise US$35 billion, but the Chinese Government started a regulatory clampdown which forced the transaction to abort. Entrepreneurs like Jack Ma were marginalised. Without major capital injections, it's unlikely China tech will be able to keep up with the innovation driven by the extraordinary R&D investments of their US rivals.

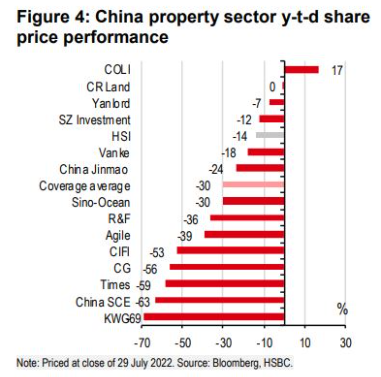

6. Property and infrastructure spending have underpinned Chinese growth, but residential prices and property company share prices are falling quickly. According to Andrew Batson, Research Director at Gavekal Dragonomics:

“Since 90% of residential property sales in China are of uncompleted units, a perception that developers cannot be trusted to finish construction will make people more unwilling to buy new housing, creating an even bigger problem in real estate.”

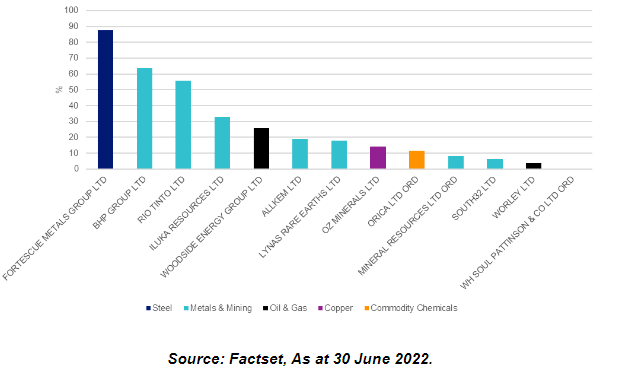

Many Australian companies are currently enjoying high export prices for commodities, and the chart below sourced from VanEck shows the level of dependence on China.

Resources revenue from China for major Australian companies

China accounts for 31% of Australia's total trade with the world. Already, some trade-restrictive measures imposed by China have caused exports to fall significantly since 2019. Although most investors do not directly own Chinese shares, China has become the major geopolitical issue of our times.

***

Sometimes, a few words in a Reserve Bank announcement gain a lot of attention. This week's increase in the cash rate by 0.5% to 1.85% was met by some optimism based on the final five words of the sentence:

“ ... the board expects to take further steps in the process of normalising monetary conditions over the months ahead, but it was not on a set path.”

For example, Andrew Canobi, a Director at Franklin Templeton, said:

“The RBA seems to be communicating a desire to look at the incoming data, going forward, and then address where they’re at. And what we think they’re signalling here is that a big part of the heavy lifting has been done.”

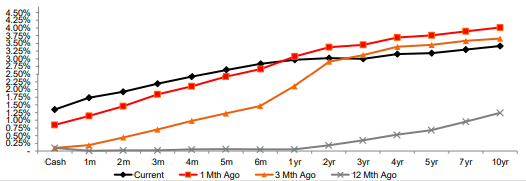

In my view, the words do not sound different than in the past. As shown in this chart sourced from NAB, the current yield curve in black continues to flatten with long rates falling below levels a month or three ago. For example, rates are down a strong 0.4% in a month in the three-year part of the bank curve. The market is now expecting cash rates to top out at 3.2% in March 2023 which is a long way down from 4% in recent months. For the struggling borrowers, it will be a relief.

Westpac’s Bill Evans has revised his cash rate peak to 3.35%, based on stronger growth than Treasury's 3% this financial year and 2% next. Says Evans:

“In effect, we expect (calendar) 2022 to be much stronger than the Treasury while the slowdown in 2023 will be much more severe as the rate hikes bite.”

Meanwhile, NAB's Ivan Colhoun is not going as high:

“NAB’s view is that seeking a return to 2%, 3% inflation will likely require at least a slightly restrictive monetary policy setting, which we suggest is in the 2.6-2.85% cash rate range.”

In this week's articles ...

Experts. We love them and hate them. We quote them and criticise them. We agree and we disagree. Their wisdom from on high is the subject of much financial commentary every day. So let's go to two experts with the highest global profiles, both committed to educating and informing, and see how they differ. Reading Ray Dalio and Howard Marks leads to pondering whether there is a difference between common sense and uncommon sense.

I worked with Michael Witts at CBA more decades ago than either of us care to remember, and after over 40 years in the market and the last 12 as Treasurer of ING Bank in Australia, Mike has retired. He takes a look at some of the changes in the market, especially in mortgages, he has experienced. Enjoy smelling the roses, Mike.

Meg Heffron continues her excellent monthly series on managing SMSFs with some useful tips on whether someone should wait until they set up a pension account before selling an asset with a significant capital gain. Although pension funds are tax free, the best timing is not as obvious as it first appears.

From 1 July 2022, large super funds began rolling out their Retirement Income Covenant statements, and it's expected that lifetime annuities will play a role. David Knox highlights a pricing inequity that needs to be sorted out before their use becomes more common.

While there's no doubt every business is rethinking its office space requirements in the wake of staff working from home, a central meeting place remains essential for corporate culture and collaboration, even if it's not every day as it used to be. In fact, demand for premium space is strong, as Andrew Ballantyne and Steve Bennett report on results of the most recent survey.

Markets hang out for the latest inflation data as the prime determinant of interest rates and direction, so it's no longer acceptable that the Reserve Bank receives only quarterly data. As Lewis Jackson explains, we are far behind every other country in the G20. Change has been discussed for a dozen years.

We were sad to hear of the death of Phil Ruthven last week. Phil has been a wonderful supporter of this publication, delivering popular and high-profile articles to our readers since the start in 2013. We pay tribute to his advice to business leaders across decades by linking to every article written for us, including a short excerpt so you can decide which to read again. Vale Phil.

For the Weekend Edition, two articles from Morningstar. Nicola Chand asks analysts to update the outlook for retail stocks, and it may not be as rosy as FY22. And Nicki Bourlioufas checks when the recovery in global travel is likely to translate into profits for former market darling, Flight Centre.

This week's White Paper is from Western Asset, part of the Franklin Templeton group, looks at US inflation today and how it differs from previous periods based on economic growth, wages, and price disparities.

Graham Hand

Weekend market update

On Friday in the US, the S&P500 was flat, down 0.1% at the close, while the NASDAQ lost 0.5%.

From Shane Oliver, AMP: The rebound in share markets continued over the last week helped by good earnings data and relief that increased China/US tensions resulting from US House Speaker Nancy Pelosi’s visit to Taiwan did not spill over into a more serious conflict (at least not yet). Despite a slight set back on Friday as strong US payrolls data were seen as keeping the Fed hawkish for now, for the week US shares rose 0.4%, Eurozone shares rose 0.3% and Japanese shares gained 1.4%. Chinese shares were the exception and fell 0.3%. For the week bond yields reversed some of their recent falls, mostly after the strong US jobs data. Oil and metal prices fell, but iron ore rose.

We remain of the view that shares are vulnerable to a pull back over the next few months as central banks are still a way off from peaking and actually cutting rates, recession risk is still rising and this runs the risk of significant earnings downgrades and geopolitical risk is still on the rise as highlighted by China/US tensions in the last week and the upcoming November US mid-terms. However, the continuing strength of the rebound (with the direction setting US share market up 13% from its low) raises the possibility that we may have seen the bear market low and any pull back may just be a partial retracement of the rally since mid-June. Either way, on a 12-month horizon we remain optimistic on shares as inflation recedes, central banks become less hawkish and a deep recession is likely to be avoided.

From AAP Netdesk: The Australian share market finished at a two-month high after gaining ground for a third straight week. The benchmark S&P/ASX200 index on Friday finished up 41 points, or 0.6% to 7,016, the first time since 9 June it has closed above the 7000 level. For the week the ASX200 gained 71 points, or 1%.

On the ASX, energy and mining on Friday went in two different directions, with the former the worst-performing sector and the latter the best. Energy was down 1.4% as Brent crude dropped to a six-month low of $US93 a barrel following a surprise buildup of US oil inventories. Woodside dropped 1.3% while Viva Energy fell 4.5% and Whitehaven Coal retreated 3.5%. But the materials sector gained 1.9% with gains across iron ore miners, goldminers and lithium producers. BHP advanced 1.7% to $38.81 and Rio Tinto gained 2.6% to $97.74. Elsewhere, the big banks were mixed, with ANZ up 0.8% to $22.95 and Westpac rising 0.5% to $21.96, but NAB was flat at $30.91 and CBA down 0.4% to $101.41.

***

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

Australian ETF Review from Bell Potter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website