One of the stated aims for the government’s CGT changes was to improve generational inequality.

But will the changes be better for young investors?

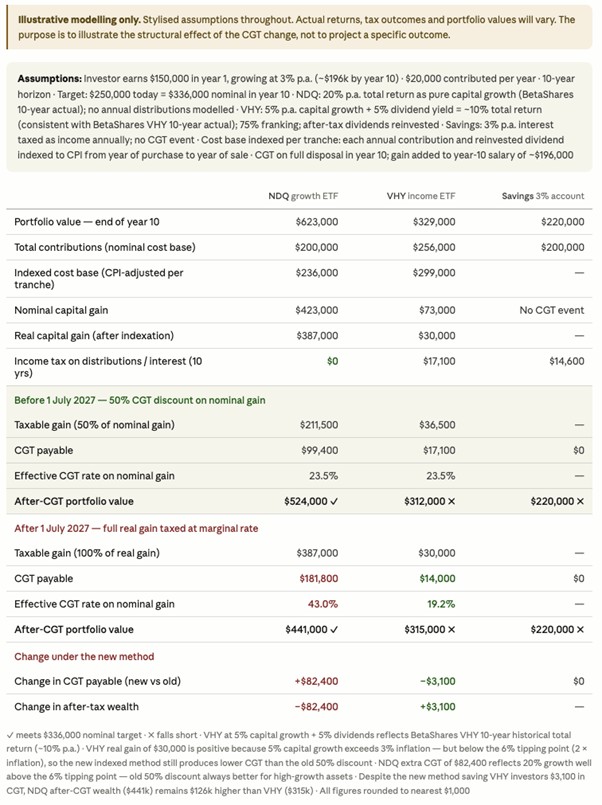

To explore if young investors will benefit from the government’s CGT changes, let’s consider the case of a young person who wants to accumulate a deposit so that they can buy a home. We will explore how well off they are under each of the current and the new CGT arrangements.

In this example, they are on an income of a base salary of $150K a year, which increases each year with inflation, which we will take to be 3%.

They need to build up a home deposit and enough to pay any stamp duties. Let’s say this amount required for their home deposit will be $250K in today’s dollars, and that their goal is to accumulate this home deposit in 10 years. They will make contributions of $20K each year into their investments to work towards that goal.

Let’s consider three scenarios for how they accumulate their home deposit:

1. They invest in a high growth ETF.

To represent this scenario we will imagine that they invest in the Betashares ETF NDQ, which tracks the NASDAQ 100. As I write, the 10-year historical growth for NDQ has been 21.33% per annum. In this scenario, we will assume that NDQ continues on a dream run and grows at 20% a year over the next 10 years.

For modelling purposes we will treat the entire 20% growth as capital growth, consistent with the Betashares total return methodology, which includes reinvested distributions. We will assume that the growth is consistent year on year without any volatility.

2. They invest in a high yield dividend ETF

Let’s say that they invest in a high yield dividend ETF, such as Vanguard’s VHY. The dividend yield is 5% a year each year which is reinvested, and the ETF market price grows at 5% a year.

The total return is therefore 10% a year. This is consistent with the 10-year average performance of VHY of a total return of 10.18% p.a. as of the time of writing this article.

3. They save the money in a bank account, at a 3% p.a. interest rate

They earn 3% p.a. on their capital, and they pay tax on the interest payments to the bank account.

How does this young person fare under the current CGT arrangements, compared to the new CGT arrangements? Indicative results are shown in the following table.

I have used AI as a research tool to perform calculations and produce visuals. If you are using this information to guide your own decisions you should consult a financial advisor, or perform these calculations yourself with your own specific information.

This investor clearly achieves a better outcome when investing in the high growth investment option. This is the case under either set of CGT tax arrangements – nothing has changed in that regard.

But if we focus on whether this young investor is better off under the new CGT arrangements or not, then in this example clearly they are not. If they invest in the high growth option, they are $82,400 worse off than under the current system. If they invest in the income option, they are $3,100 better off than under the current system. The investing approach that gives them the best outcome relative to their goals is hit hardest by the changes to the way CGT is calculated.

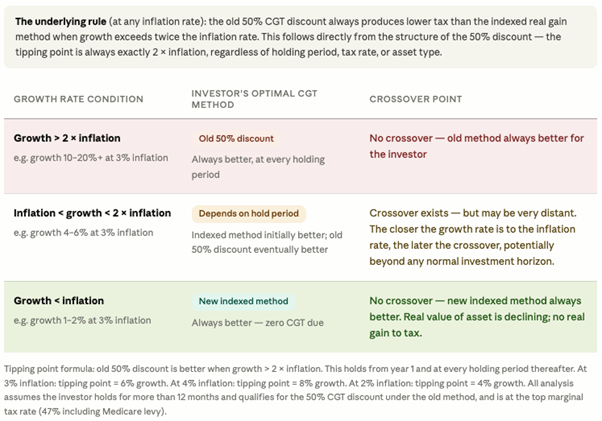

There is a more general pattern here. The higher the capital growth rate that their investment delivers – the higher the growth rate for the investment is above inflation – then the worse the new method of calculating CGT will be for them.

More specifically, if the growth rate for the asset is greater than twice the inflation rate, then as soon as they qualify for the CGT 50% discount (after the first year) then the investor will always be significantly better off under the old 50% discount method for calculating the CGT than they would be the proposed new indexed method. This is shown in the following table.

If the growth rate is more than inflation but less than twice the inflation rate, the new indexing approach to calculating CGT will be better for the investor - until a crossover point is eventually reached and the old CGT 50% discount approach would deliver better outcomes for the investor.

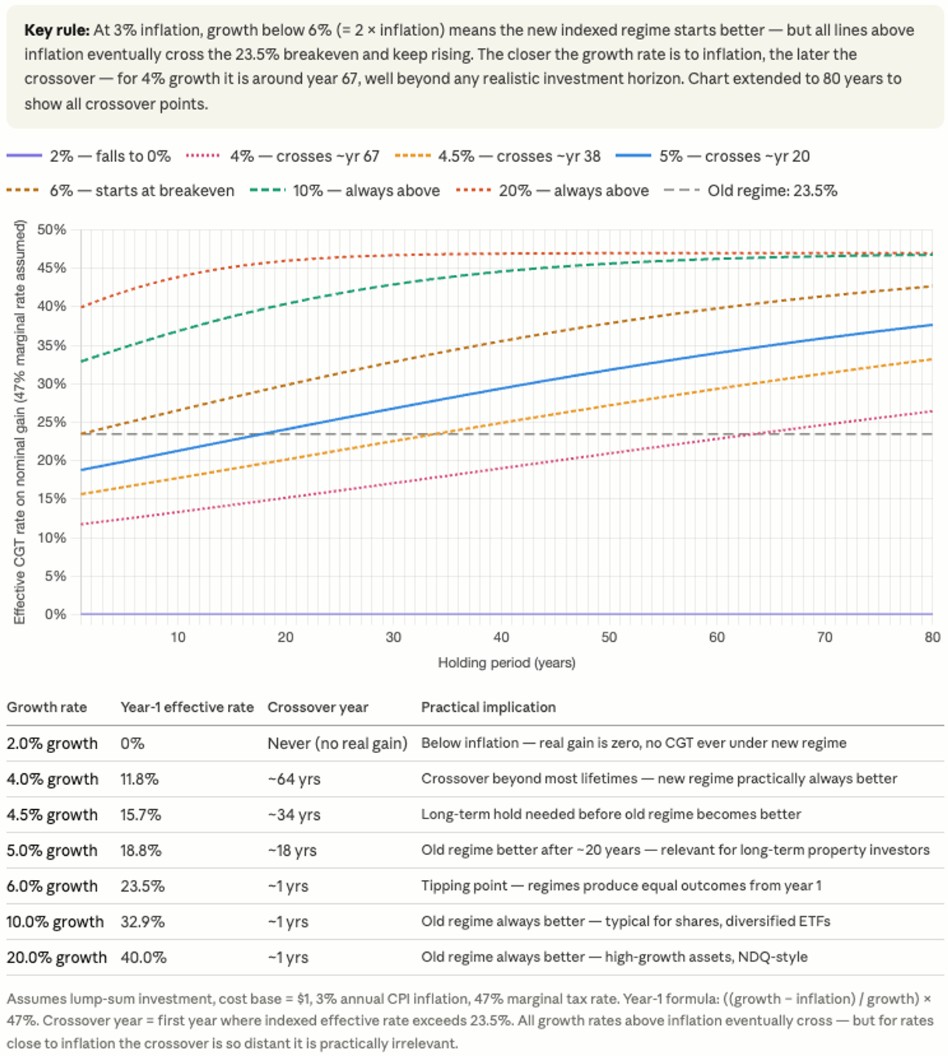

These crossover points are illustrated in the following chart, produced to illustrate which CGT taxation method is better for an investor under the old and new proposed CGT methods when inflation is 3%. Please note again that this chart is for illustrative purposes only, and if you are using this to guide your own decisions you should consult a financial advisor or do the calculations yourself with your own assumptions and in relation to your goals and circumstances.

The crossover point is very sensitive to the investment rate. If the growth rate is close to twice the inflation rate, this crossover point might be reached within two or three decades; if the growth rate is close to the inflation rate, then the crossover point is unlikely to be reached during the lifetime of the investment and for assets with that growth rate the new indexed approach to calculating CGT will always be better.

Young investors are typically in the accumulation phase of investing, and typically seek high growth assets. The new CGT methods proposed are consistently skewed against the interests of young investors and are not the CGT assessment method that they would prefer or that would help them reach their goals.

The new CGT calculation method will raise more revenue for the government — $7 billion a year by Treasury's own projection. It may even be a more economically 'efficient' form of taxation. But it does not seem to do anything to help young investors get ahead. In fact, it would seem to have the opposite effect.

Dr Lauchlan Mackinnon is an independent researcher with interests in capitalism, vocation, and investing. He holds a Ph.D. in Economics and Philosophy from the University of Queensland.