In reference to the proposed new capital gains tax arrangements before parliament, Anthony Albanese told the House of Representatives post-budget that, “we’re moving towards the system that was in place before 1999 to tax real gains, not nominal gains.”

Except that that is not entirely true. Yes, indexing the capital cost base to inflation is being reinstalled to replace the 50% discount on realised capital gains, but the smoothing of gains over five years to alleviate the bunching effect of realising a lump sum in a single year has not been revived.

And a 30% minimum tax on real gains has been introduced that has never existed before, intended as a disincentive to investors realising gains in years of low marginal tax rates due to retirement or by design.

Although sketchy as to how the 30% minimum tax would work when announced, details of its calculation have now emerged.

In a multi-step procedure, the real capital gain is first multiplied by 30% to give the minimum capital gain tax liability. Tax liabilities are then calculated according to the current tax schedule, for both total taxable income including the gain, and for taxable income excluding the gain. If the difference is less than the minimum CGT liability determined prior, then top-up tax to that minimum applies.

A numerical example using the 2025-26 tax schedule:

A real capital gain of $50,000 is realised in a year with $40,000 of additional taxable income.

The minimum CGT liability would be 30% x $50,000 = $15,000.

Tax on the $90,000 total income would be $17,788.

[$4,288 plus 30c for each $1 over $45,000]

Tax on the $40,000 non-capital gain income would be $3,488.

[16c for each $1 over $18,200]

$17,788 - $3,488 = $14,300, which is less than the minimum CGT liability by $700.

$700 top-up tax applies. Which represents 4.7% of the total tax liability.

If however, there was no other income in the year, tax on the $50,000 gain under the tax schedule would be $5,788. Top-up tax in that instance would therefore be $9,212, or 61.4% of the total tax liability, which highlights the punitive nature of the new 30% minimum tax on gains.

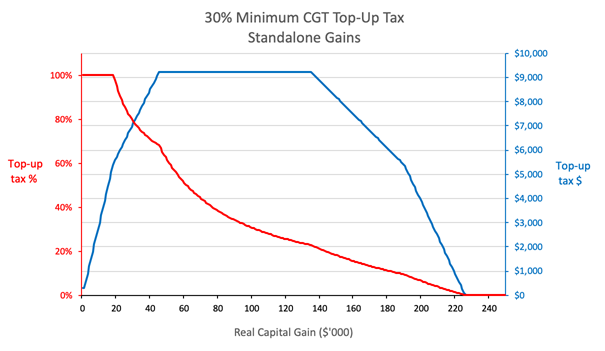

Focusing on gains without other income in a tax year, top-up tax rises steeply with small gains, peaking at $9,212 for gains from $45,000 to $135,000, which coincides with the 30% marginal tax rate band. From $135,000 it begins to run down, reaching zero on a gain of $225,746, the point at which the effective tax rate on income is 30%.

In percentage terms, on a standalone gain of $45,000, top-up tax represents 68.2% of the total tax liability, running down to 22.7% at $135,000, and ultimately 0% at $225,746.

This is a strange pattern. The top-up tax starts out progressive, becomes a virtual flat tax for a $90,000 stretch to $135,000, and from that point is steeply regressive as the top-up tax slides down to $0 at $225,746 and beyond. This tax element creates a reverse-progressive situation for the mid- to upper-tax brackets where the top-up tax falls as the size of the gain increases.

And even if you consider a high-income year with a large gain, let’s say a $200,000 salary with a $250,000 real gain. The gain sits entirely within the 45% marginal tax bracket, attracting $112,500 tax. If the gain was deferred to a year of no income, tax on the gain would fall to $78,638, with no top-up tax because the 30% floor is already exceeded. The tax liability drops by about $34,000, with the effective tax rate falling to 31.5%. The incentive to defer the gain remains enormous, with the 30% minimum tax ceasing to have any effect at this level.

This doesn’t look like a system that would disincentivise those with successful investments, to cash in during years of low other income. Yet the Budget Explainer says that the policy "reduces the benefit of taxpayers deferring capital gains realisation to years where their marginal tax rates are low."

It is a system with a virtual separate capital gains tax schedule superimposed on the ordinary income tax schedule. It takes the 0% and 16% bands and replaces them with 30%. The 30% band is untouched, but then inexplicably, the 37% band drops down to 30%, and even the 45% band drops to 30% for standalone gains between $190,000 and $225,746, before reverting back to 45% beyond that.

When the minimum tax was announced without calculation detail, I had assumed that logically, it would be applied by simply replacing the 0% and 16% brackets with 30% exclusively for capital gains. That would mean a flat 30% for the first $135,000, then leave the 37% and 45% brackets unchanged.

Such an approach would still see the top-up tax peak at $9,212 on a standalone gain of $45,000, but it would be maintained at that amount, and never run-off no matter the size of the gain. And while the size of this penalty would be insufficient to eliminate the incentive to defer larger gains, at least it would reduce that incentive. This system would:

- avoid regressivity.

- maintain a penalty at higher gains.

- ensure a deterrent for deferral of gains, no matter the size.

- simplify the application of the 30% minimum tax without the need for a clumsy multi-step procedure.

Instead though, we have a policy design that uses a flat-rate floor to fix a perceived problem with income timing strategies, but which in the end contradicts the intention of the Bill. Smaller gains suffer reduced progressivity, while larger gains continue to have a pathway to time realisations to their advantage.

Even though the tax package has now passed the Senate, the government continues to bow to pressure and make changes to the legislation. Let’s hope this contentious 30% CGT floor is also under consideration for a rewrite.

Tony Dillon is a freelance writer and former actuary. This article is general information and does not consider the circumstances of any investor.