Much has been written about the tax changes in last week’s budget. But there are some aspects of the property tax changes that have received little attention and are worth expanding on.

1. These reforms have fragmented the property market, essentially creating two tiers of residential property.

We will now have ‘full tax status’ tier 1 property, consisting of new builds purchased directly from developers, and grandfathered existing properties purchased prior to the budget changes. These tax-sheltered properties will see new stock sought after by investors, and a ‘lock-in effect’ on the existing stock as owners are less inclined to sell.

Then there will be ‘restricted tax status’ tier 2 property, consisting of established housing purchased after budget night, including new builds sold by the first owner. These properties should face a drop in investor demand and value in the secondary market.

Specifically, the tax restrictions on tier 2 properties are:

- the 50% capital gains tax discount is removed and replaced by indexation of the cost base for inflation, such that the real gain is taxed. A minimum 30% tax rate is applied to gains, effectively overriding the 0% and 16% tax scale rates.

- the amount by which expenses exceed rental income in a financial year is quarantined and cannot be used to offset wage income. It effectively sits in a ‘loss basket’ able to be possibly used against future property income or realised gains.

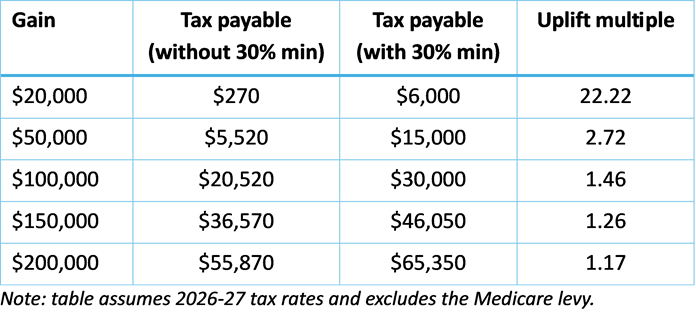

2. The minimum 30% tax rate on capital gains is punitive.

In effect, the 30% minimum CGT rate turbocharges bracket creep. Bypassing the two lower brackets (0% and 16%) causes an immediate spike in tax the moment an asset is sold, with the very first dollar of gains taxed at 30%.

For illustrative purposes, assume gains were the only income in a tax year. Tax payable on gains without and with the 30% tax rate minimum would be:

While investors would often have income from other sources, these numbers illustrate how a 30% minimum disproportionately affects low-income gains, weakening a progressive tax system. And making it more difficult to accumulate wealth prior to retirement.

The 30% minimum also amplifies the ‘bunching effect’ of the capital gain, an effect caused by gains accumulated over possibly many years being treated as a lump sum in the year of realisation. This potentially pushes investors into higher tax brackets than would otherwise be the case had the gains been smoothed over multiple years. The 30% floor then accelerates the push through the progressive tax schedule.

With the previous 50% discount acting to some extent as a shock absorber for the lumpiness of the gain, removing it and applying a 30% tax rate minimum is a double whammy on the taxation of gains.

3. The treatment of inflation is asymmetric.

Net rental losses are quarantined and frozen in nominal terms, such that the real value of future tax relief is steadily eroded by inflation over time. Meanwhile, the cost base of the asset is indexed for inflation.

The new rules are therefore asymmetrical in the sense that the government ignores inflation on what it is liable for. This creates a growing disadvantage with time for investors holding loss making properties.

A fairer way would be to capitalise the losses as they occur and index them in line with the asset’s cost base.

The asymmetry may be intentional by design to discourage investors from holding negatively geared properties for long periods.

4. A less favourable capital gains tax regime is likely inflationary.

When the taxation of capital growth increases relative to income, then the flow of capital would be expected to shift more towards yield. Money moves out of high-growth property development, as well as venture capital, and startups into commercial and regional type property, and high-dividend yield stocks.

And when capital investment stalls, productivity growth slows which impacts the supply side of the economy. That is, the economy cannot respond as well when demand in the economy inevitably rises due to population growth, government deficits, and wages growth. And excess demand in the economy is inflationary.

This is possibly an unintended consequence of a deliberate policy aim to “rebalance a system which is more generous to assets than it is to labour”, according to Jim Chalmers.

Of course, improving the taxation of income relative to assets, if that is the aim, could also be achieved by taxing income less while maintaining the status quo on the taxation of capital. And which should be a productivity enhancing approach.

Indeed this is an option that is being put forward by the Coalition, with Angus Taylor saying that he will take to the next election policies of repealing Labor’s capital gains tax and negative gearing changes, while indexing income tax brackets to inflation to eliminate bracket creep.

Battle lines on major taxation policy have finally been drawn.

Tony Dillon is a freelance writer and former actuary. This article is general information and does not consider the circumstances of any investor.