On May 12, Treasurer Jim Chalmers handed down one of the most unpopular budgets in Australia's history. He claimed the Budget was about fixing intergenerational inequality and making housing more affordable for first-home buyers. Tell him he's dreaming.

For starters, the term "intergenerational inequality" is a social construct dreamed up by Labor to create a whole new class of victims they can encourage to vote for them. Yes, young people have challenges, as young people always have, but so do older Australians.

As for affordable housing, it's fast becoming a pipe dream. Even the Budget papers forecast housing prices will rise by 4% over the next year. A tax cut worth roughly $50 a week for younger workers is hardly going to help much when mortgage repayments keep climbing as interest rates rise. There also seems to be an assumption that the best way to increase housing supply is to make investing in residential property by individuals as unattractive as possible. Clearly, they've never heard the adage: "Money flows to where it's treated best."

Talk to any builder, and they'll tell you they're overworked, prices are going sky-high, and they can't get staff. Furthermore, they're held down by a web of red tape and bureaucracy. Just this week, a builder told me he had a block of apartments all set to go, but couldn't get the plan registered until the Brisbane City Council lodged their landscaping certificate. Can you believe it took the Brisbane City Council 12 weeks to lodge a simple certificate? That was 12 weeks of wasted time, which he said cost him over $200,000 in delayed settlements.

I can't see building prices dropping in this environment.

Capital gains tax

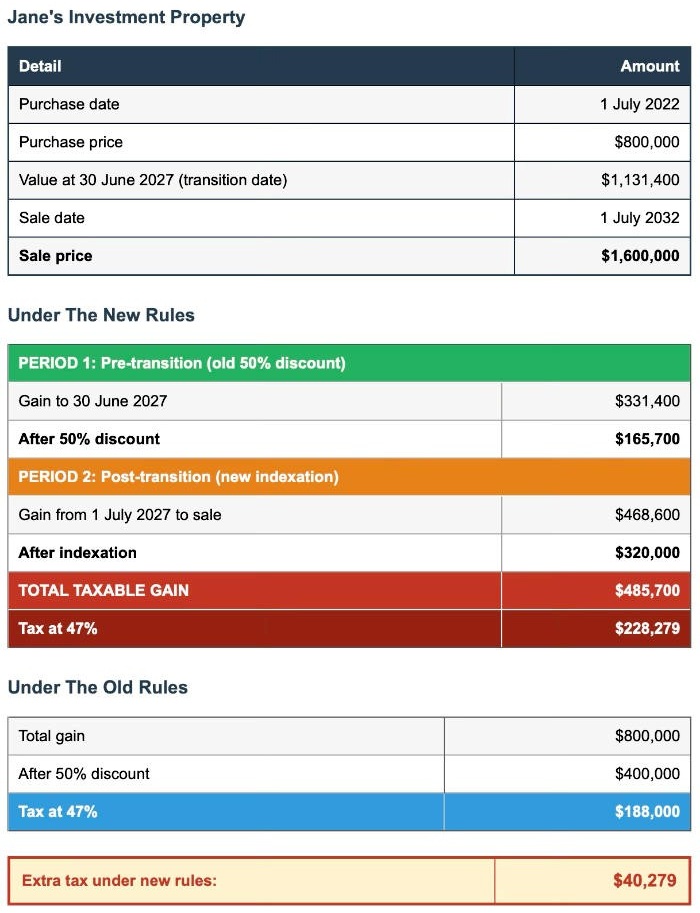

They claim the changes have been grandfathered, but in my view they are only partly grandfathered. Suppose you own a property now worth $800,000 that you bought 10 years ago for $400,000. You will get the 50% CGT discount if you sell the property by 30 June 2027. But if you sell after that date, two sets of rules will apply. A case study may make this clearer.

This example is from the Budget papers, but the numbers have been rounded to make it easier to understand. Jane buys a property on 1 July 2022 for $800,000. She sells it on 1 July 2032 for $1.6 million. Using what the department calls “ATO tools”, she discovers the asset was worth $1,131,400 on 30 June 2027, when the transition came into effect.

The difference between that value and her original cost price is $331,400, which reduces to $165,700 after applying the 50% discount. She then subtracts the 30 June 2027 value of $1,131,400 from the selling price of $1.6 million. This gives her a gain of $468,600 from 1 July 2027 until the property was sold on 1 July 2032. After indexation from 1 July 2027 until the sale date, the adjusted gain would be $320,000.

The total taxable gain is then the sum of $165,700 and $320,000, giving a taxable capital gain of $485,700, which would be added to her taxable income in the year of sale. The tax payable would depend on her other income, but if we keep it simple and apply the top marginal rate of 47%, the total CGT bill would be about $228,279.

Under the old rules, her gain would have been $800,000, which, after the 50% discount, would have reduced to $400,000. Tax at 47% on that amount would have been $188,000, which is about $40,000 less than under the proposed new rules.

I appreciate this is complex, which is why it is so important to get expert advice if you are even thinking about selling a CGT asset. They're summarized in this table to help you understand how it works.

Special treatment for pensioners: The $1 pension loophole

The Budget exempts anyone receiving even one dollar of "income support" from the new CGT rules. That includes pensioner couples with $1.054 million in assets who get a few dollars a fortnight in pension. They keep the full 50% CGT discount. No questions asked.

These same couples can earn $90,000 a year from work without losing a cent of pension. A single renter with no assets is treated in the harshest way imaginable.

Meanwhile, meet Jenny. She's 67, rents for $400 a week, and has no assets apart from a few dollars in the bank. She gets the full single age pension of $30,654 plus rent assistance of $5,616, giving her a total income of $36,254 a year. She considers a job paying $45,000. Sounds good, right?

Here's what actually happens. Once her income exceeds $218 a fortnight, she loses 50 cents of pension for every extra dollar earned. The Work Bonus gives her some temporary relief in year one, but after that it's gone. Her $45,000 salary costs her $13,780 in lost pension. Add $10,516 in tax, and the combined hit is $24,296. She's working full-time for an extra $20,704. That's an effective marginal tax rate of 54%. No-one else in Australia pays tax at that rate.

But a couple with over a million dollars in assets? They can earn $90,000 with zero impact on their pension—and now they're protected from CGT changes too.

The system protects the wealthy and punishes the poor. This Budget just made it worse.

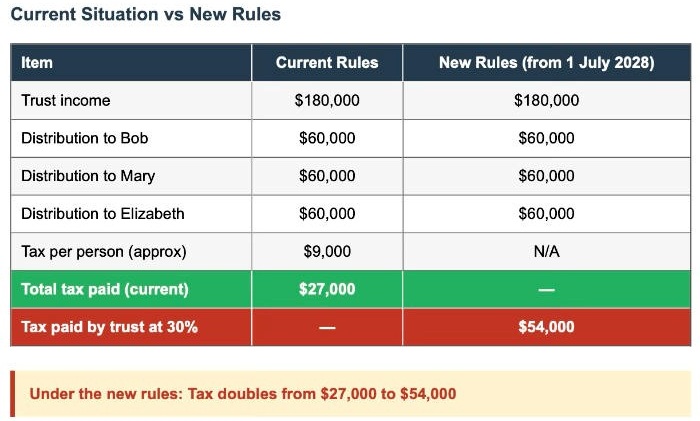

The Trust tax bombshell

From 1 July 2028, family trusts will be hit with a flat 30% tax rate. The impact is brutal.

Bob and Mary run a small business through their family trust. They net $180,000 a year and distribute $60,000 to each of them, plus another $60,000 to their daughter Elizabeth. Tax on these distributions is about $9,000 each – a total of $27,000 a year.

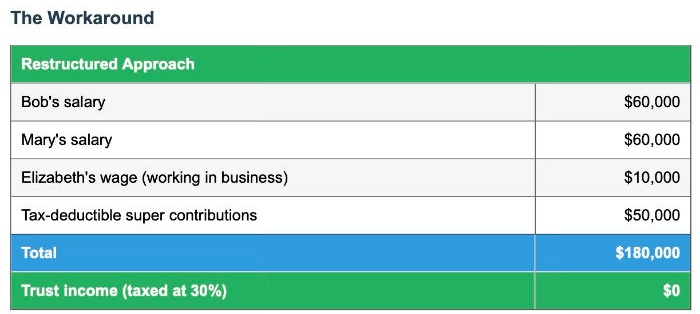

The way around this is to ensure the trust has no income itself, and the money is distributed to the beneficiaries in a different way.

This is just one simple example, but it does show the importance of anyone with a family trust working closely with their accountant to optimize their taxation position before these changes take effect.

The death tax

There’s been plenty of media speculation about a possible death tax. Much of it appears to relate to potential changes to testamentary trusts, but that remains a grey area and experts are still waiting for details. But there is already a form of death tax effectively locked in: Division 296, the proposed tax on super balances above $3 million.

Take Jack and Jill. They each have $2.5 million in super, so neither is affected because both are under the threshold. Then Jack dies and his super passes to Jill, pushing her balance to $5 million and leaving her $2 million above the threshold and potentially exposed to Division 296 tax.

A death tax by stealth.

Noel Whittaker is the author of Making Money Made Simple and numerous other books on personal finance. His advice is general in nature and readers should seek their own professional advice before making any financial decisions. Email: [email protected].