The proposed capital gains tax (CGT) reforms announced in the Federal Government’s recent budget represent more than a simple change in tax mechanics. They alter the value of one of the most important advantages available to long-term investors: the ability to convert nominal gains into concessionally taxed capital gains.

Today, investors benefit from a 50% discount on gains realised after a 12-month holding period. However, under the proposed framework, that discount would be replaced by inflation indexation, meaning only the inflation-adjusted portion of a gain would be exempt from tax.

At first glance, both systems appear to reward long-term investing. In practice, however, the economics are quite different. The current regime rewards patience with a fixed 50% discount regardless of market conditions, while the proposed system ties the benefit directly to inflation. As a result, the current regime would produce superior after-tax outcomes in almost all instances, other than in an environment where inflation is high over a sustained period.

The key question for investors is therefore not simply whether taxes increase, but which investment strategies are most exposed.

Turnover: the hidden driver of tax outcomes

Portfolio turnover- the degree to which asset managers buy/sell assets in any given year - can have a significant impact on investment performance and tax outcomes. The reason? CGT is only payable on realised gains whereas unrealised gains continue to compound tax-free, creating a valuable deferral benefit for investors.

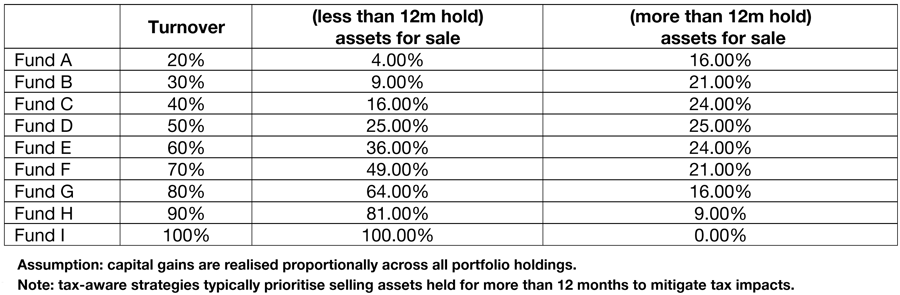

Let’s consider how two funds delivering identical pre-tax returns can produce very different after-tax outcomes, depending on how frequently gains are realised. The table below illustrates the proportion of gains assumed to be realised from positions held for less than, and more than, 12 months across different turnover levels.

Consider a fund generating a 10% annual return with 20% turnover, a 30% tax rate (proposed minimum CGT) and inflation of 3%.

Only one-fifth of the portfolio return is realised each year. Of those realised gains, a relatively small proportion originates from shorter-term holdings and is fully taxable. The remainder comes from assets held for longer than 12 months and therefore qualifies for concessional treatment.

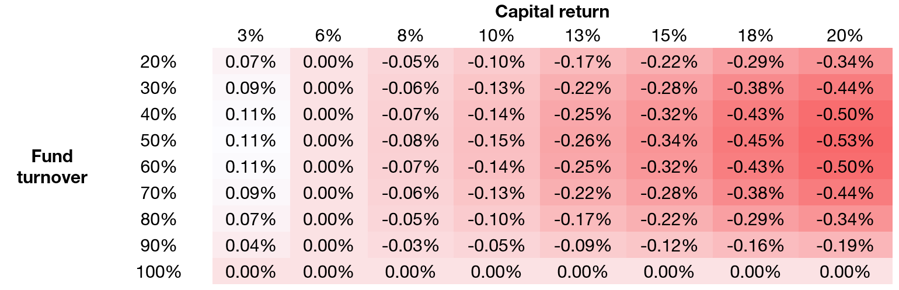

Under the current system, the tax payable on those longer-term gains is approximately 0.24% at the portfolio level. Under the proposed indexed approach, tax rises to around 0.34%. The result is a reduction in after-tax return of roughly 0.10% p.a.

While 0.10% may appear modest, its cumulative impact becomes meaningful over long investment horizons. More importantly, it highlights a broader principle: when investment returns significantly exceed inflation, a 50% CGT discount is substantially more valuable than inflation indexation.

The surprising impact on moderate-turnover funds

The impact of the reform is not linear. One might assume that high-turnover funds would be most affected because they realise more gains. In reality, the greatest impact falls on funds with moderate turnover.

Why? Low-turnover strategies defer most gains and therefore remain largely insulated from any changes to the taxation of realised gains.

High-turnover strategies are also relatively unaffected because a large proportion of their gains are already taxed at full rates. They receive little benefit from the current CGT discount and therefore have less to lose.

Moderate-turnover funds sit in the middle. They realise enough gains to create a meaningful tax liability, yet still rely heavily on long-term holdings that currently benefit from the 50% discount. These strategies enjoy the largest tax advantage under the existing regime and therefore stand to lose the most when that concession is replaced by inflation indexation.

In many cases, the after-tax impact peaks around turnover levels of 40-60%.

Market returns matter just as much

The impact of the reform also depends heavily on the return environment. When returns are close to inflation, there’s little difference between the two systems. In fact, indexation can occasionally be marginally more favourable, because inflation offsets much of the taxable gain.

However, as returns rise above inflation, the gap widens quickly. The current 50% discount becomes increasingly valuable, while the benefit provided by indexation remains fixed by the inflation rate. In other words, the reform matters most when investors are successful.

Strategies delivering strong capital growth are likely to experience the greatest deterioration in after-tax outcomes, particularly when combined with moderate turnover.

Implications for portfolio construction

Turnover remains a key driver of after-tax outcomes, determining the extent to which returns are realised and subject to tax. While the proposed reform doesn’t change this fundamental relationship, it reduces the tax advantage of long-term holdings by replacing the 50% CGT discount with a less generous indexation framework. The effect varies across strategies and is influenced by both turnover and investment returns, becoming more pronounced in stronger market environments. High-return, moderate-turnover strategies appear most exposed, while very high-turnover strategies are comparatively less affected.

From an investor's perspective, only gains accrued post 1 July 2027 are impacted, while existing unrealised gains retain access to the current discount. While our primary focus remains on maximising pre-tax risk-adjusted returns through active allocation and rigorous manager research, tax considerations will increasingly matter in preserving investor wealth.

Overall, tax efficiency is likely to become a more explicit input into manager selection and portfolio construction, alongside risk/return, style, diversification and liquidity.

Ethan Xing, CFA is a portfolio manager (Asset Allocation) at Zenith Investment Partners. This article is general information and does not consider the circumstances of any individual investor.