As anticipation grows for the upcoming federal budget, financial commentators will fixate on two words: debt and deficit. These will be the measures by which the government’s fiscal performance will be judged. But there is a growing disconnect between debt and spending, with the culprit being ‘off-budget’ accounting.

Where typical government expenditure flows through to the ‘underlying’ cash balance, cash flow into financial assets for policy purposes that are deemed off-budget ‘investments’, does not. Such expenditure does however add to gross debt, and is recorded in the ‘headline’ cash balance.

The problem is, and in muddled terminology, the headline figure around budget time is the ‘underlying’ cash balance, while the ‘headline’ cash balance is paid scant regard by the media.

But with the December 2025 Mid-Year Economic Fiscal Outlook (MYEFO) revealing ‘underlying’ cash balance deficits totalling $143 billion in the four years to 2028-29, the equivalent ‘headline’ deficits total $237 billion. That represents anticipated off-budget spending of $94 billion, which is by no means trivial and warrants clear understanding.

Included in the $94 billion going to ‘financial assets’:

- Additional equity injections (including in the NBN, Snowy Hydro, Clean Energy Finance Corporation)

- Loans (including to Snowy Hydro, write down of HECS loans)

And since the Albanese government came to office, fund capitalisations to the tune of some $50 billon have arrived off-budget, including Rewiring the Nation Corporation ($20 billion), the National Reconstruction Fund ($15 billion), and the $10 billion Housing Australia Future Fund.

As we shall see, these items alter the scale of the government’s balance sheet, shifting attention away from direct spending. But they represent real cash outflows.

To understand how off-budget accounting works, consider the Housing Australia Future Fund (HAFF).

It was set up like a mini sovereign wealth fund, with an initial $10 billion capital injection that was raised by the government issuing bonds, adding to gross debt. Under the Future Fund Board, the $10 billion is invested in financial markets, with up to $500 million per year of investment earnings earmarked for social housing projects and affordable housing programs.

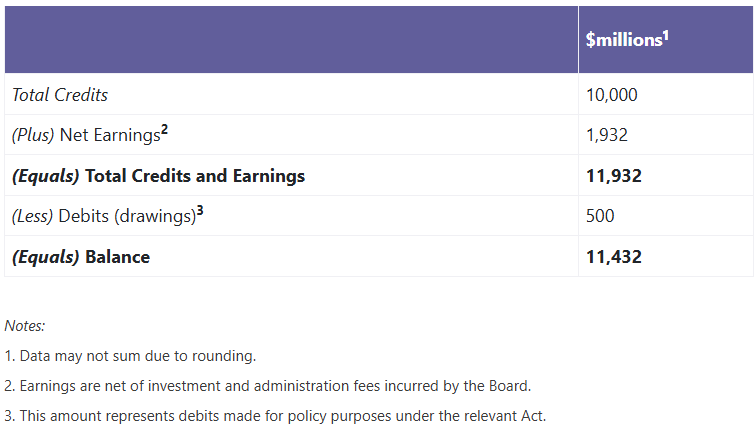

Housing Australia Future Fund - Financial performance since inception to 31 December 2025

Source: Australian Government Department of Finance

How this is all accounted for is key.

The $10 billion outlay was deemed an investment, not expenditure, and therefore was not counted in the ‘underlying’ cash deficit. It does, however, sit in the less scrutinised ‘headline’ cash deficit. The government’s balance sheet expanded, with the $10 billion fund a financial asset, and gross debt increasing by the same amount.

Once in place, distributions from the fund are taken up as revenue in the ‘underlying’ cash balance, offset by corresponding housing spending. With little net impact on the cash balance. And the government pays interest on the borrowings used to establish the fund, also recorded in the ‘underlying’ cash balance.

So what has happened here?

As well as altering the fiscal presentation, policy programs moving off-budget introduce investment risk. While the HAFF $10 billion doesn’t register in the ‘underlying’ cash balance, it is a leveraged position borrowing at a fixed cost with fiscal outcomes determined by market returns. The sustainability of this approach is dependent on a positive spread between return on investment and cost of debt. The process represents a shift from income statement to balance sheet, with the most closely watched budget metric not capturing this economic reality.

The HAFF was established in November 2023, and as of December 2025, its balance was $11,432 million. Breaking this down: $10,000 million capital injection + $1,932 million investment earnings - $500 million disbursement = $11,432 million. This represents investment performance well above the benchmark rate of return of CPI + 2-3%.

But there was also interest paid on the start-up capital, which since inception would be of the order of $900 million. A budget cost. This highlights the mismatch of the capital being excluded from the underlying balance, while the cost of funding it is not.

Compare the off-budget HAFF approach to a more conventional arrangement. The government would not set up an investment fund with borrowed money. Rather, it would simply fund the housing program directly each year by up to $500 million, recorded as expenditure in the budget. The costs would be visible with no differences recorded between the ‘underlying’ and ‘headline’ cash measures.

This is where things become blurred. Is the HAFF a policy program or an investment? If the fund was created to deliver a policy outcome first, and to earn a commercial rate of return second, then it is basically spending with risk attached. It amounts to spending via markets as opposed to spending via a budget.

And the larger the difference between the ‘underlying’ and ‘headline’ cash measures, the bigger the fiscal spending off-budget and the size of program invisibility, compounded if follow-up equity injections occur like with the NBN and Snowy Hydro. Focus ends up not so much on the scale of the initial decision, but more on the smaller cashflows it generates. The conversation shifts from one of $billions up front to $millions per year, because of the lesser scrutiny around cash deployed for ‘investment’. In the end though, taxpayers carry not only the program cost, but the investment risk as well.

So why transform a straightforward spending program into a leveraged investment position?

The establishment of a fund is less about having a punt, and more about bringing forward a commitment to spending. And even though there could be commitment without a fund structure, the government is basically capitalising an annual budget in the balance sheet. In that sense, it removes the annual argy-bargy for funding when the intention is locked in for future years.

Governments like this approach because it creates future funding that would be harder for future governments to unwind or to make program cuts. It is a signal that the program is not temporary. The trade-off is the loss of annual scrutiny and flexibility.

Overall, off-budget accounting doesn’t reduce the cost of policy. Rather, it changes its visibility, risk, and the timing of financing. And the extent to which it is now deployed warrants greater scrutiny and challenge. Particularly around budget time.

Tony Dillon is a freelance writer and former actuary. This article is general information and does not consider the circumstances of any investor.