“Over the years, I have made many mistakes. Our satisfactory results have been the product of about a dozen truly good decisions - that would be about one every five years.“

- Warren Buffett, Annual Letter to Berkshire Hathaway shareholders, 2022

“Focusing on aggregate shareholder outcomes, we find that the top-performing 2.4% of firms account for all of the $US75.7 trillion in net global stock market wealth creation from 1990 to December 2020. Outside the US, 1.41% of firms account for the $US30.7 trillion in net wealth creation.”

- Hendrik Bessembinder and colleagues, Financial Analysts Journal, revised March 2023

***

When Hendrik Bessembinder published his original study on the stockmarket performance of 26,000 US companies from 1926 to 2016, he expected a few hundred fellow academics to read it. It was somewhat blandly titled “Do Stocks Outperform Treasury Bills?”, and to him, it was about ‘skewness’ or the asymmetry of returns.

“When I was compiling this, I almost didn't write it up. I thought people must know this. Because it's not exactly rocket science, you know, honestly, to take the same database that other people have been looking at and actually compound the returns. Seems a lot of people were caught by surprise.”

But as word leaked out about his results, the world media and financial commentators took notice.

(The original research is available free on SSRN from 2017 here and updated from 2023 here).

The surprising results that caught world attention

There have been a multitude of studies of long-term returns, but it was Bessembinder’s results which shocked, and he outlined them in a recent presentation in Sydney. Out of 26,000 US listed companies:

- A few stocks have very large compound long-run returns.

- The large positive ‘market risk premium’ is attributable to relatively few stocks.

- The top 90 firms (1/3 of 1%) account for half of the shareholder wealth enhancement (relative to US Treasury Bills) since 1926.

- The top 4% of firms account for all of the net shareholder wealth creation since 1926.

Only about 1,000 stocks out of 26,000 accounted for all the US$35 trillion of wealth created (above the Treasury Bill rate). This is far from a coin toss as 96% of companies did not contribute to growing net shareholder wealth. Bessembinder said of his research:

“The basic difference here is that I took those monthly returns and compounded them for a given stock over time. When I compound them out over the full time that they're in the database, most of them deliver negative returns. A few stocks on the other hand give very large compound returns ... The stock market as a whole is doing very well for investors. Most stocks are not doing well for investors. The only way this adds up is that there's a relative few stocks doing very well.”

Even more skewed in the global results

In his Sydney presentation, Bessembinder also reported on his updated work, which now covers 64,000 global companies from 43 countries over 30 years. To show the US results were not a fluke, the global stock market returns were even more skewed.

Of the US$76 trillion shareholder wealth created by 63,785 firms from 1990 to 2020:

- The top 5 firms (0.008%) accounted for 10.3%

- The top 159 firms (0.25%) accounted for 50%

- The top 1,526 firms (2.39%) accounted for 100%

- The other 62,259 firms collectively matched US Treasury Bills.

In his research, 25,441 (39.9%) companies did generate (modest) positive wealth which just offset the wealth destruction of 36,818 (57.7%) companies.

It’s a difficult number to comprehend. Only 2.4% of global listed companies account for all the market performance above a short-term government security.

What factors caused the outperformance?

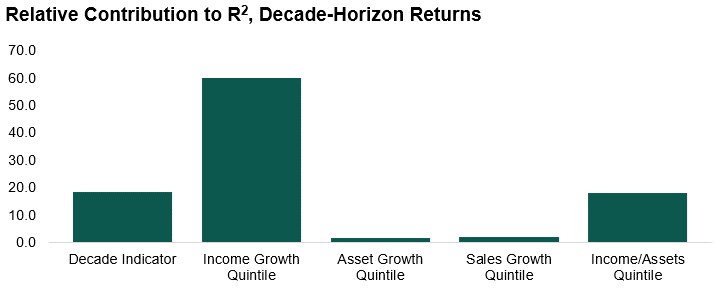

Bessembinder then started looking for the source of the outperformance, especially the growth in fundamental measures. Based on compound returns in US stocks from 1970 to 2020, he found five fundamental variables which he says explain about 29% of the variation in multi-decade stock returns.

The strongest indicator was income growth, while asset and sales growth were relatively unimportant. He also tested the ‘decade indicator’ to see if there was something about particular decades which produced strong results, and he compared the income to assets ratio.

What does this mean for investing?

Every company that lists on the stock exchange is sponsored by a broker, who pitches the name to its investors by producing expansive offer documents showing the apparent potential of the company and detailed financial and future plans. While the broker has some duty of care, the main aim is to sell the asset. These companies are bought by market professionals, as well as retail investors. And despite all this professional oversight navigating listing and regulatory rules, the overwhelming majority of companies destroy wealth versus simply investing in a government security. Most companies destroy investor wealth over time.

There are two opposing ways to interpret these results.

The first view is that if so few stocks create all the market’s gains, it must be extremely difficult to identify them early enough, which speaks to the merit of passive investing and owning everything. At least then, a small slice of the big winners is in play.

The second view is that there are extraordinary rewards for the active fund manager who invests in these moonshots, at almost any time in their early development. It does not need to be at pre-IPO, IPO or shortly after. That is only the start of a long and successful run. A big win compensates for losses elsewhere.

The fact that Bessembinder was brought to Australia to speak at a conference called ‘Active Advantage’ shows his work influences active managers who work to identify rapidly-growing, ground-breaking companies in the list above. In fact, Scottish fund manager Baillie Gifford financed the global study.

What does Bessembinder say?

Knowing his work can support arguments for both active and passive investing, Bessembinder walks the fence. While he says:

“I think I have provided some ammunition for the people who say it’s their business to chase moonshots. The skewness shows just how big the pay-offs can be if you’re good at this.”

… Bessembinder hedged his bets in his own interpretation, making these arguments in Sydney:

- In the long run, stockmarket investing has much in common with venture capital.

While all venture capitalists have a unique approach, in general, they place many bets in startup companies knowing that 80% will fail, 10% will breakeven and 10% will deliver success in a big way. Obviously, they do not deliberately select companies they expect to fail, but picking early-stage winners is difficult. The surprising aspect of Bessembinder’s work is that more-established listed companies are the same or worse.

- (Many) Investors should hold low-cost and broadly-diversified portfolios.

Bessembinder acknowledges that the majority of people do not have special skills to identify a few great companies, and he supports the majority holding cheap index funds. BUT

- (Some) Investors should select focused portfolios.

Some investors have enough of a comparative skill advantage (and this might be individuals or fund managers) to select stocks and build their own portfolios to outperform.

- We should reconsider approaches that implicitly assume that only the mean and variance of returns matter.

Portfolio optimisation theory explains investing as a tradeoff between risk (variance of returns) and mean (average returns) but he argues there are far more factors involved in explaining markets.

“I think we've really been missing something by focusing just on mean variance. If you actually look at how things turn out and longer horizons, mean variance analysis was motivated by stock returns that are normally distributed, more evenly distributed. That's just nowhere close to the truth.”

In the presentation, Bessembinder elaborated on his ‘active versus passive’ views:

“The textbooks lay out all the reasons why people should have broadly diversified low-cost portfolios, and my study backs that up. Just picking stocks at random, the odds are worse than 50-50. On the other hand, if you can pick winners in the future, some investors should be actively trading. The irony is that when people read my study, it's like a Rorschach test. What do you see here? But I do think there is a really important idea of comparative advantage that comes from economics. What are you good at? I firmly believe some asset managers have the right comparative advantage. And among those who place their funds with asset managers, some have a comparative advantage in identifying the right asset but that doesn't mean everybody should be.”

Are you or a favourite fund manager especially talented?

For most people who are not market professionals, the chance of selecting sustained winners among thousands of listed companies is remote. It’s not impossible, and many will argue that picking up the Commonwealth Bank or CSL or Wesfarmers or Macquarie Bank (or going back, the big winner, Westfield) was not that difficult. No amount of evidence will convince them otherwise, so to them ... go for it and have fun.

While index investing in the US now commands the majority of new flows, active funds management dominates in Australia. For investors who have confidence they can identify the fund managers who will outperform over time, then also ... go for it and have fun. Bessembinder does not want to spoil the party.

But for most retail investors, the man who spends his life studying the numbers says buy a low-cost and diversified portfolio. Manage risk tolerance through asset allocation and the mix of defensive and growth assets rather than worrying about individual stocks. Shares will rise over time but with painful periods along the way, and everyone reacts differently to underperformance, either by their own stocks or a selected fund manager.

Just recognise that while you’re having fun, the odds of finding the special outperformers are slim, but maybe some people do have a comparative advantage.

Graham Hand is Editor-At-Large at Firstlinks. This article is general information and does not consider the circumstances of any investor.

Hendrik Bessembinder was a presenter at the Active Advantage Forum co-hosted by Orbis, MFS International (both sponsors of Firstlinks) and Baillie Gifford, and Graham Hand attended as their guest.