The government has consistently sought to minimise the impacts of the CGT changes on small businesses.

The Small Business Minister Anne Aly has stated that about 90% of small businesses would experience "absolutely no impact"[1] from the CGT changes.

The Prime Minister asserted that “Now, 90% of small businesses in Australia are eligible for these concessions, and they’ll continue to remain eligible.”

In response to pushback on these changes, the government has announced a reprieve: an expansion of one of the key eligibility criteria for one of the concessional CGT programs for small businesses. Under the change, the maximum revenue threshold for the 50% Active Asset Reduction program will be lifted from $2 million to $10 million, enabling more businesses to access this program. The government has stated that following this change, all 2.7 million active small businesses and 98% of all active businesses will be eligible for this concession.

This sounds pretty good. But is the government being honest with us?

Let’s assess their claims.

The government’s first claim: 90% of small businesses would experience "absolutely no impact" from the CGT changes to business

The Small Business Minister’s claim is difficult to accept.

This follows from two considerations:

- Eligibility: the “90%” eligibility claim is questionable and misleading.

It is not at all clear that 90% of businesses actually will be eligible for one or more of the concessional CGT programs.

- Impact: the “no impact” claim is incorrect in three out of four of the concessional CGT scenarios.

It is straightforward to see that in many, if not most cases, businesses will still be significantly impacted by the CGT changes even if they are eligible for one of the four concessional CGT programs.

The “90%” eligibility claim is questionable and misleading

Where did the government derive the “90% of businesses” figure from?

Over 90% of businesses in Australia have a revenue of under $2 million. Therefore, if businesses were to be assessed solely against the maximum revenue threshold - whether or not it had a revenue of under $2 million - then 90% of businesses would be eligible. This statistic is where the government’s 90% claim derives from.

The problem with this approach, though, is that the $2 million maximum revenue threshold is not, in fact, the only eligibility criteria for the concessional CGT programs. To see how many businesses are in fact eligible for one or more of these concessional CGT programs, we would need to assess businesses against the complete set of eligibility criteria for the concessional CGT programs.

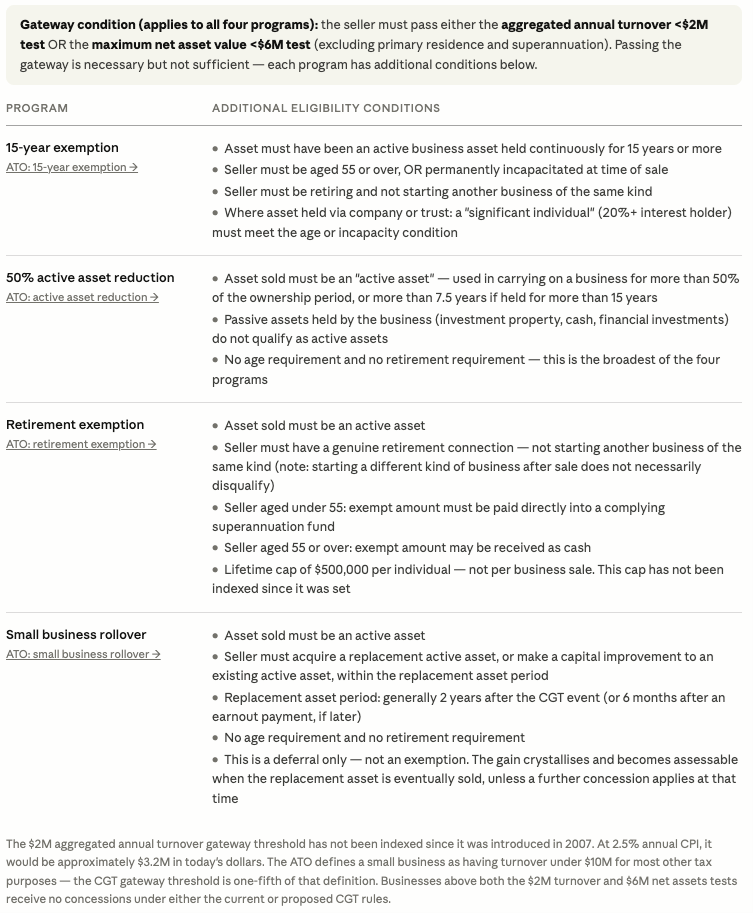

The following table summarises the eligibility criteria for each of the four concessional CGT programs.

As we can see from the table, the $2 million maximum revenue threshold is not the only eligibility criteria for the four concessional programs. The actual “gateway condition” – the eligibility criterion that must be met if they are to be eligible for any of the four CGT concessional programs – is either:

- The revenue for the business is less than $2 million or

- The net asset value for the business is less than $6 million

The “net asset value” is a technical term that reduces, for practical purposes, to the actual sale price for the business (assuming that the business is sold at fair market value).

A business with revenue of over $2 million could still be eligible for the CGT concessional programs – if its net asset value falls under the maximum net asset value threshold. For example, a business with revenue of $12 million a year that sells for $5.5 million would still likely meet the gateway condition, because its net asset value would be less than $6 million.

But even if a business passes the gateway condition, then that is not the end of the story. There are additional eligibility requirements, unique to each concessional program, that a business must meet in order to qualify for a concessional program.

The concessional program with the most restrictive eligibility requirements is the 15-year Exemption program. To qualify for this program, the eligibility requirements also include that:

- The business must have been running (be an “active business asset”) for 15 years or longer

- The owner of the business must be over the age of 55 (or incapacitated)

- The seller intends at the time of sale to retire (and not start another business).

It is simply not correct to claim that 90% of businesses would be eligible for this program. They would have to meet the gateway condition - and satisfy the other eligibility conditions such as the age of the owner and the age of the business.

The Retirement Exemption program similarly requires that the business owner is intending to retire.

The program with the broadest eligibility is the 50% Active Asset Reduction program. This simply requires that the asset be an “active asset” for at least half of the ownership period.

The Prime Minister said that “90% of small businesses in Australia are eligible for these concessions, and they’ll continue to remain eligible.” This one program, the 50% Active Asset Reduction program, comes closest to fulfilling the Prime Minister’s claim, due to its broader eligibility conditions.

But it’s still not correct for the government to claim that 90% of all businesses would be eligible for these concessions - because not all businesses are saleable. A business that cannot be sold cannot create a capital gain, and a business that doesn’t produce a capital gain will clearly never qualify for a capital gains tax exemption.

Let’s unpack this further.

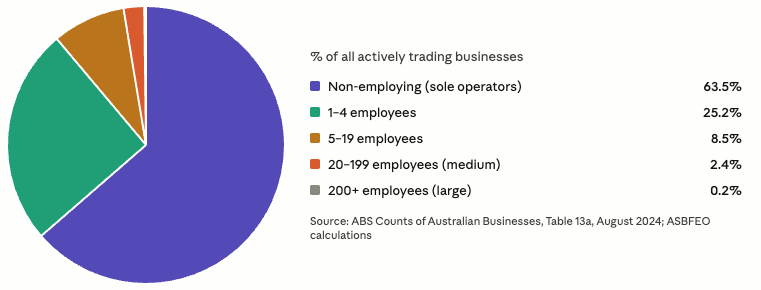

The number of businesses we are discussing comes from the ABS dataset on Counts of Australian Businesses. This data is based on counting the number of ABNs that are registered.

But the fact that a business has an ABN does not mean that the “business” has any employees. The business could be a sole contractor, like an uber driver or a solo carpenter or a solo law practice – people who work for themselves but could not “sell” their business to anyone else because they have not built up any substantial business value independent of their own work labour. Their business depends on them.

In fact, around 63.5% of those “businesses” have zero employees. This is illustrated in the following pie chart:

The number of saleable businesses that could qualify for CGT concessional programs is likely to be predominantly made up of the 36.5% of businesses that have employees -particularly the 33.7% of businesses that hire 1-4 or 5-19 employees.

If the government is referring to a percentage of businesses that are eligible for the concessional CGT programs, the denominator for that assessment must be saleable businesses. Businesses that cannot be sold are not relevant to that calculation.

The “no impact” claim appears to be false in three out of four of the possible scenarios

If a business remains eligible for one or more of the four CGT concessional programs, is it true that there will be no impact on them under the government’s new approach?

In three out of the four cases, the answer is “no.”

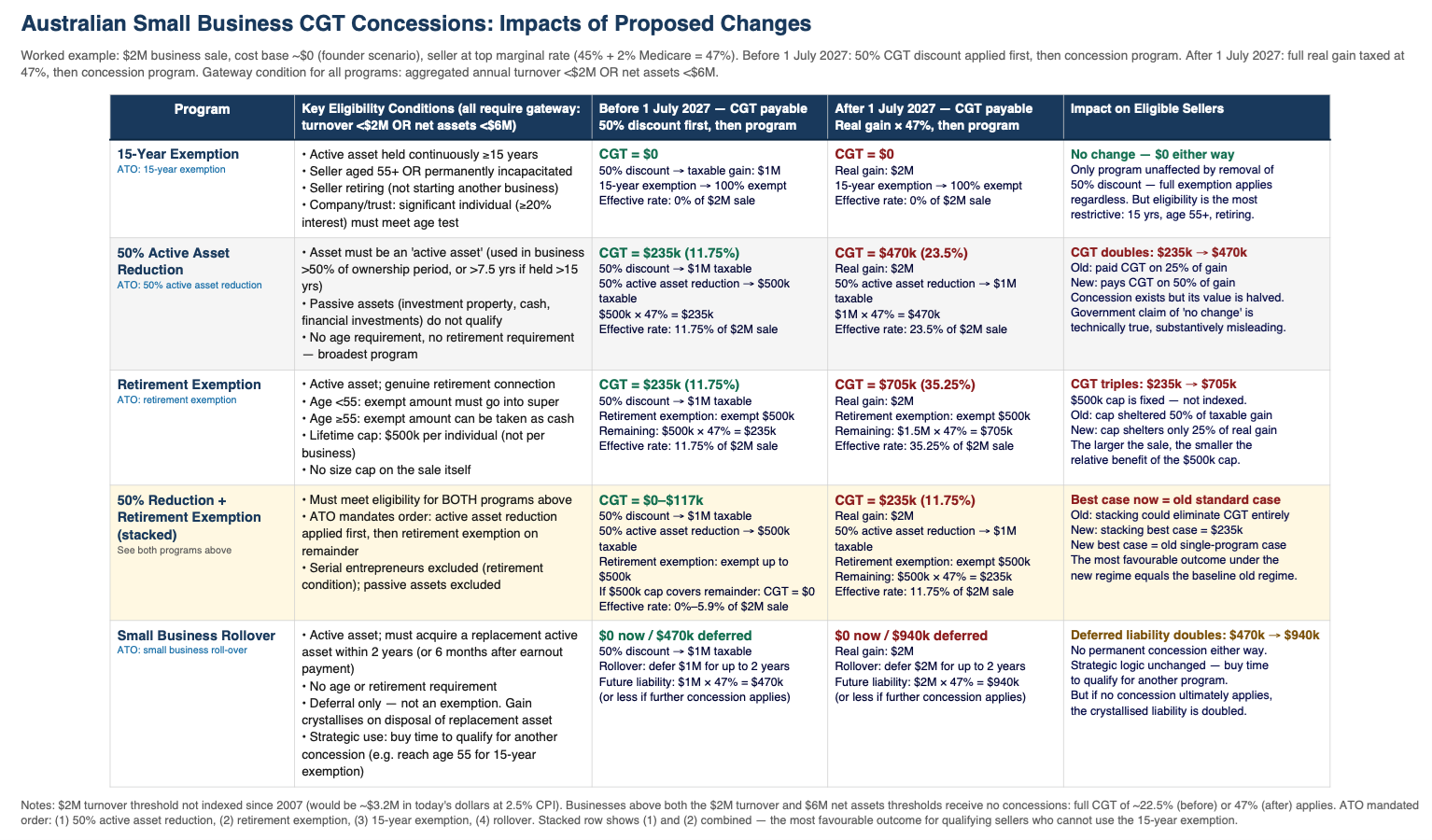

To illustrate, the following table shows the four concessional programs, their eligibility requirements, and the CGT payable under old and new systems for a founder selling their business for $2 million.

Click to enlarge

Under these four concessional programs, the only case where the small business owner is as well-off under the new CGT calculation method as they were under the old CGT calculation method is when the business is eligible for the 15-year Exemption program. This is because if they are eligible, then the CGT is reduced to zero. Under either the new or old CGT arrangements, they are equally well-off with this very generous CGT exemption.

But, as we noted, this is the concessional program with the steepest eligibility requirements.

For example, if a business owner is now 40 and has been operating their business for 10 years, they are not eligible for the 15-year exemption for two reasons: their age, and the age of the business. By the time they wait a further 15 years until they are over the age of 55 and satisfy the age eligibility criterion, their business may have grown to, say, an annual revenue of $8 million a year and a net asset value of $9 million. At that point they fail the gateway condition – both revenue and net asset value thresholds – even though they and the business are now old enough.

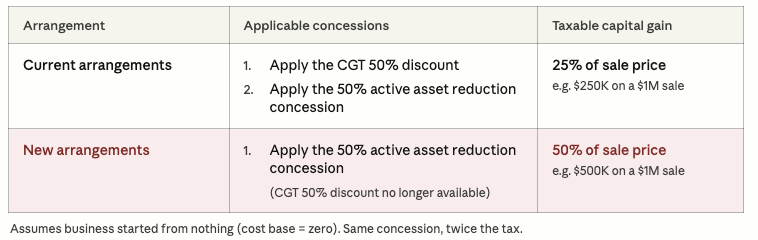

If the business owner qualifies for the 50% Active Asset Reduction program, there is one key fact to be aware of if we are to understand it properly: the 50% Active Asset Reduction program does not replace the 50% CGT discount, it works together with it.

Therefore, under the new CGT arrangements, a business owner will pay twice as much CGT under the 50% Active Asset Reduction program even if they are eligible for this concessional CGT program.

The reason why is summarised in the following table.

In the current system, if someone sells a business for $1 million, and they are eligible for the 50% Active Asset Reduction program, they would

- Apply the 50% CGT discount, to reduce their taxable capital gains to $500,000

- Apply the 50% Active Asset Reduction, to reduce their taxable capital gains to $250,000

The remaining 25% of their sale value - $250,000 - would then be taxed at their marginal tax rate.

Under the new CGT arrangement, step one would no longer apply.

Instead, they would calculate the real capital gain. Since the starting value for a business started from nothing is zero, they would index zero to adjust it for inflation, which would still be zero. The real capital gain (and the nominal capital gain) would be the sale price.

Then, if they qualify for the 50% Active Asset Reduction program, they can reduce the capital gain of $1 million by 50% to $500,000. They then pay tax on the $500,000 taxable capital gain at their marginal tax rate.

If they are eligible for the 50% Active Asset Reduction concession, then they still pay twice as much capital gains tax under the new CGT arrangements.

Businesses are clearly impacted by the changes. They pay twice as much tax.

For the other two programs, the Retirement Exemption program and the Small Business Rollover program, similar considerations apply. For the Small Business Rollover program, they can only roll over half as much. For the Retirement Exemption program the value of the concession varies depending on the amount of the sale, but for business sales of over $500,000 they will pay more tax.

The government’s current claim: 98% of all active businesses will be eligible for the 50% Active Asset Reduction concession

In relation to CGT for business owners, the key change on June 18th was raising the maximum revenue threshold from $2 million to $10 million for the 50% Active Asset Reduction program, so that more businesses would be eligible for this concession.

This is only changing the maximum revenue threshold, not the net asset value threshold, and it is only making this change in relation to one of the four concessional CGT programs – not to all of them.

It is a very specific, tightly focused change.

What are the impacts of that change?

Its impacts on eligibility are unclear

It’s not entirely clear that raising the maximum revenue threshold from $2 million to $10 million would make many more businesses eligible for the concession.

This uncertainty arises because the maximum revenue threshold is not the whole of the gateway condition – the updated gateway condition is now a revenue of less than $10 million or a net asset value (the sale price for the business) of less than $6 million.

To see why this is so, consider how a business is sold.

Around 80% of Australia’s economy is a service economy. Most businesses are service businesses, such as consulting, marketing, and software service businesses, or running a café or restaurant.

When the owner of a service business sells their business, they tend to sell it at a multiple of annual profits. For example, a business that has revenue of say $5 million a year with a profit of $1 million a year might sell the business for a multiple of 3X or 5X the profit, or in other words a $3 million or $5 million sale respectively.

In either case, in this example, the sale price would be under the $6 million net asset value threshold. Raising the revenue threshold from $2 million to $10 million would not have made that business any more eligible for the concession – it was already eligible under the maximum net asset value threshold.

The maximum net asset value is arguably the more important gateway threshold, since it is directly related to the price the business sells for.

If the government is interested in providing a genuine carve out to extend eligibility for CGT concessional programs, they clearly have superior options available. For example, they could double the threshold for the net asset value test from $6 million to $12 million, and index it to inflation - and then apply this change for all four of the concessional CGT programs, rather than just to one of them.

The changes still lead to a business owner paying twice as much tax

The changes to the maximum revenue threshold, lifting it from $2 million to $10 million, do not change the impacts. Businesses owners eligible for the 50% Active Asset Reduction program will still pay twice as much CGT as they would under the current arrangements.

Yes, the business owner will get a 50% reduction on their capital gain. But that’s instead of a 75% reduction.

It’s hard to sell that as a positive for a business owner, or to see it as an incentive for starting and growing successful, saleable businesses.

It’s not much of a “back down”

The government is only increasing the maximum revenue threshold, not the maximum net asset value threshold, so it is unclear to what extent it is actually extending eligibility. It is only making this change for one of the four concessional CGT programs (the 50% Active Asset Reduction program), and not for the other three CGT concessional programs. And it is not tackling the impacts of their CGT changes: for eligible businesses, business owners will still pay twice as much CGT as before the changes announced in the budget as they would have under the current system.

If the government wanted to design what looked like a substantial concession to address community concerns, without actually conceding much at all, it would have crafted a program very similar to this “carve out.” This is a “Clayton’s carve-out.”

This is reflected in the numbers. The government projects a cost of $475 million a year for these changes to eligibility conditions, out of the extra $7 billion a year expected to be raised from the broad changes to CGT and negative gearing.

Has the government been honest with us?

It is not clear that the government has been transparent with us. Key claims they have made, such as that 90% or 98% of businesses will still be eligible for the existing concessional programs, are questionable at best. They have been less than forthcoming about the actual impacts of these changes for small business owners. Their “carve out” is minimal, only applying to one of the four programs – and only to the less significant threshold.

The CGT changes for business sales send exactly the wrong signal to Australia's founders and entrepreneurs: that the government will now take a larger share of the value that they spent years creating. A government serious about economic growth would not do that without first giving a clear explanation of why the change is justified to help grow the overall economy. No credible explanation has yet been offered.

Dr Lauchlan Mackinnon is an independent researcher and consultant with interests in ideas, capitalism, vocation, and investing. He holds a Ph.D. in Economics and Philosophy from the University of Queensland.