The rapid decline in the number of financial planners in Australia over the past decade (from around 28,000 at the peak in early 2019 to just over 15,100 today) has been a huge factor in reducing the accessibility and affordability of financial advice. On top of this, the impact of increased regulation and red tape has made it more expensive for advisers to run their business, which also affects the cost of advice.

And of course, this is happening at a time when more Australians than ever would benefit from financial advice. The intergenerational wealth transfer, the rising cost of living, taxation reform and economic uncertainty, are all contributing to an environment where Australians need quality, professional financial advice in order to achieve financial wellbeing.

One simple step to make advice more affordable for more Australians has been to make more types of financial advice tax-deductible. Most ongoing financial advice is already deductible, but an important extension was finalised by the ATO in late 2024, confirming that some upfront advice can also be tax deductible.

In TD 2024/7, the ATO has confirmed that upfront financial advice fees are deductible to the extent they relate to tax advice.

The result is that more Australians should be able to deduct a larger portion of both their initial (as well as ongoing) financial advice fees.

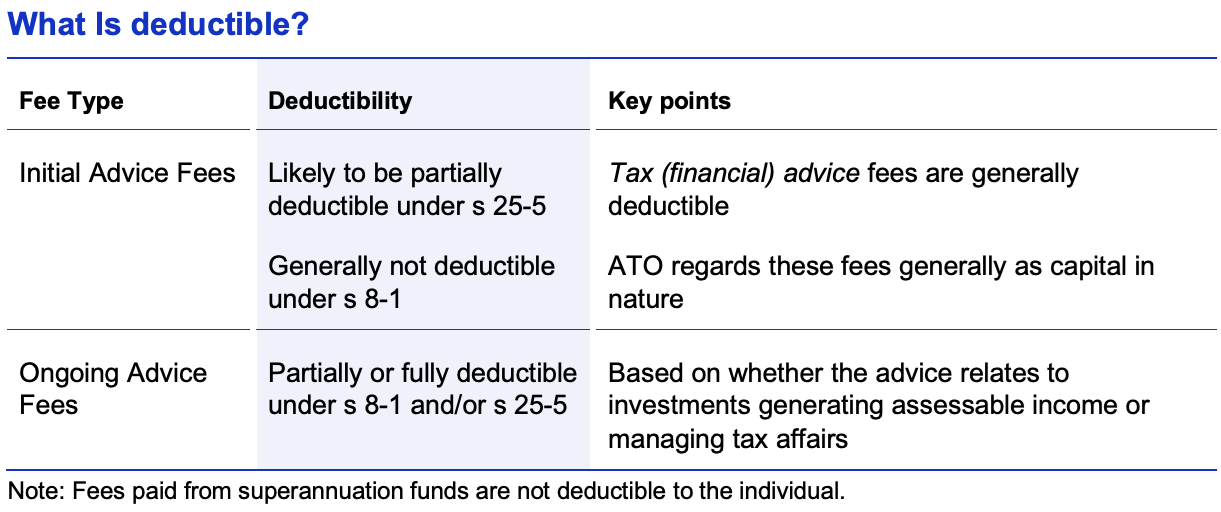

What is deductible

The definition of tax (financial) advice can include all or part of the fee for superannuation advice about contributions such as salary sacrificing, advice around superannuation pension strategies, advice on whether or not certain insurance policies should be held inside or outside of super, gearing strategies, some estate planning advice and investment structuring for taxation purposes.

Source: FAAA

How the adviser determines what portion of the advice given relates to taxation advice is complex and must be evidence based. An example can help illustrate how this might work.

Let's look at the case of Leo, a pre-retiree in his 50s looking to retire in the near future and seeking advice from financial adviser Amy. The total initial advice fee paid by Leo (i.e. not his super fund) is $5,500.

Amy and Leo have an initial consultation of one and a half hours, during which they discuss a range of factors, including a general discussion about tax affairs.

After the meeting, Amy investigates and analyses Leo's existing investments and circumstances for half an hour which includes a CGT report and an examination of his contribution caps.

Overall, Amy breaks down each portion of time she spends on Leo's affairs and what part of that time is spent on tax (financial) advice. This includes 1.5 hours spent on strategy modelling, 2 hours spent on strategy development, 5.5 hours spent on writing the statement of advice and another hour-long meeting with the client to present the Statement of Advice.

In total, Amy assesses that $2,831 of the initial fee of $5,500 is tax deductible (51%).

If Leo is on a salary of $155,000 and a marginal tax rate of 37 cents in the dollar for income earned over $135,000, that tax deductibility represents a saving of $1,047 on his upfront advice fee, reducing the effective total fee to $4,453.

Affordability gains

In this example, the deductibility of certain portions of the financial advice fee is an effective 20% reduction in cost.

Our annual Value of Advice consumer research consistently shows that advised clients are much more confident about their financial affairs, with 96% in our most recent survey for 2025 saying that it has provided them with more value than it costs, and 93% reporting that their financial adviser has made them tangibly financially better off.

By reducing the overall effective cost of advice, the tax deductibility of some parts of the advice fee further improves affordability and allows more Australians to access financial advice.

So if you are a financial advice client, make sure you talk to your accountant and financial adviser about tax deductibility of any advice fees, when finalising your tax return for FY26!

Sarah Abood is the Chief Executive Officer at the Financial Advice Association Australia (FAAA).