A mix of health concerns, market volatility and employment disruption felt over the past two years and recent cost-of-living stresses have increased concerns about their retirement. This slippage is evident in key comparisons with our 2020 research:

- Employees today expect to retire half a year later than they did in 2020.

- They expect to retire with $100,000 less in retirement savings – their total expected retirement saving has fallen from $500,000 to $400,000.

- The number who expect a comfortable retirement has fallen nearly 10%.

The cost crunch

Over one third (35%) of workers have changed their retirement goals due to the impact of the pandemic and the policy responses to it (lockdowns, JobKeeper etc). But it’s striking that the more recent economic trends of higher costs and rising inflation are now dominating worries about retirement, especially those who may not have had the opportunity to build their savings over a long period.

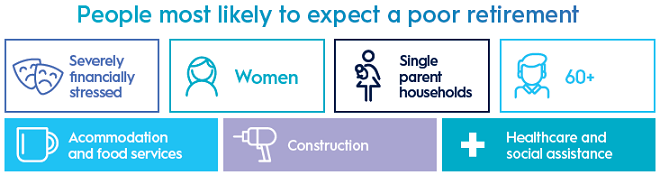

About 45% of women are particularly concerned about how higher costs will affect their retirement lifestyle, a significant increase on 2020. Similarly, it is women, single parents and pre-retirees who are more concerned about the damage inflation could do to their life after work.

Nearly 50% of 50–59-year-olds cite this concern, reflecting the perceived damage inflation can do to those who are close to retirement but who feel they haven’t saved enough to cope with rising costs. On an industry basis, it is workers in areas like Accommodation and Food Services and Health Care and Social Assistance that are most worried about retirement. This is no surprise as these fields are where women are over-represented and part-time work is common.

Fear of Running Out (FORO)

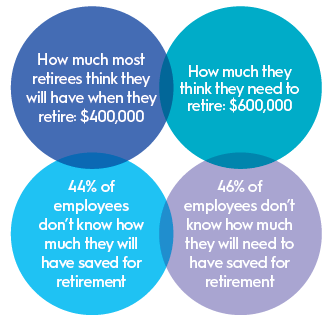

There’s a clear gap between how much people expect to retire with ($400,000) and what they think they need ($600,000). That $200,000 perceived gap is also a potent source of financial stress.

Whilst FORO is real and understandable, authoritative sources like Treasury’s Retirement Income Review (RIR) suggest that many retirees comfortably outlive their savings.

So this stress may be overdone and unnecessary. There are implications for employers and the financial services sector here.

Retirement needs are highly personal. So while industry benchmarks are helpful, we shouldn’t be placing too much focus on a single retirement number. Employers, advisers and the financial services industry can promote positive actions – yet reduce financial stress – if they help educate employees to better understand their individual retirement financing needs and how to meet them.

The good news is that the financial services sector is already turning to the task of reducing FORO.

Engaging in the future

Most Australians are not prepared to compromise the lifestyle they’ve dreamed of in retirement. Many have reduced their current spending, while more than 60% say they would work for longer to avoid a lifestyle downgrade once they finish work. Only a third (34%) would be happy to re-adjust their lifestyle expectations.

This flexibility means employees give themselves more time to plan for retirement and craft new working and saving arrangements that help them reach their long-held retirement dreams, even if it’s a few years later.

The past two years have increased people’s fears that retirement won’t live up to their expectations and that their non-work lives will be crimped by financial concerns.

However, the fact that Australians are engaging more actively with their super planning and are prepared to be flexible about reaching their goals is a highly positive development. To take advantage of these trends, the financial services industry, employers, financial advisers and policymakers need to:

- Invest in retirement income education that looks beyond generic ‘needed to retire numbers’ to give people a more realistic and less stressful view of their retirement prospects.

- Educate people about the broader range of tools that can help them fund their retirement, such as the age pension, government benefits such as discount cards, low-cost healthcare through Medicare, property ownership and part-time work.

- Encourage retirees to look beyond the return on their assets as the only source of retirement income. For many retirees it makes sense to draw down on their retirement capital to support their lifestyle, as long as it’s done in a disciplined fashion.

- Similarly, help people to ‘right-size’ their retirement goals, to take into account their income, health, family circumstances, work patterns and lifestyle expectations in ways that encourage positive action rather than worry and anxiety.

- Highlight how effective good financial planning can be in helping individuals ride out the effect of market volatility or short-term economic dislocations.

Five ways to ease the pressure on yourself

Here are five practical approaches to managing financial stress, but the main message is not to overanalyse the feelings of financial stress. Identify ways to control those fears, assuage those stresses and move on.

1. Find your bearings, clarify your situation, build your budget

Without a clear sense of where you are, you can’t take any steps to change your position. Start by clarifying and writing down exactly where you are financially. That means knowing the balances in your banks, super funds and credit card providers to get a clear picture of your personal balance sheet.

Take a look at both your spending and income. Many bank accounts today have budget or tracking apps that provide a clear view of your spending patterns. The first step here is to put aside some cash for emergencies (3-6 months’ income is often recommended).

With all this information at your fingertips, a real sense of your financial position helps to stop worrying and start managing.

2. Put yourself first and set your financial goals

Taking control of your money is not just managing the components of a good financial life (budgets, a savings plan, regular super contributions etc). It’s having something to aim for. So while good financial management will reduce financial stress, it should also be focused on your goals and your dreams – whether that’s a travel-filled retirement, helping your children or simply not having to worry about money every day.

Popular financial goals

Ages 18-29 – Purchasing a house

Ages 30 to 39 – Providing security for children

Ages 40 to 44 – Paying off mortgage

Pre-retirees – Saving for retirement

3. Get help from the experts

There’s plenty of research showing that people who draw on expert advice from financial planners, accountants, super funds and more are less financially stressed and make better decisions.

All the providers we mentioned above, plus government sources like the ATO website and Moneysmart.org, have free educational material that can help you budget more carefully, invest more prudently, protect your family via insurance and save for retirement. They contain practical tools – checklists, calculators, tips and online learning, designed by experts - to give you greater control over your money.

Some super funds and investment firms offer access to comprehensive financial advice, but there are more limited advice options available that will help you address specific financial issues that are causing you stress. Take advantage of those options.

1 in 2 employees say their likely to seek professional financial advice in the next 12 months.

4. Make work, work

Workers who are financially stressed find it harder to focus on work, so it makes sense for your employer to care about your financial position. The more secure you are, the better for you, the better for them.

Talk to HR, your line manager and your super fund. All of them will have avenues you can explore together to build financial security. They could range from financial and psychological helplines, access to cheaper insurances, discounts on goods and services and financial education. Or it could be sophisticated solutions like salary sacrifice options and access to comprehensive financial and insurance advice. These are work-related benefits that can boost your financial wellness and make you better at your job.

5. Prepare for retirement

As with any journey towards better financial wellness, the path to a more comfortable retirement starts with knowing where you start.

Whether by yourself, with an accountant, financial adviser or help from your super fund, you need to get a clear picture of your pre-retirement financial position: the money you have in super, savings and investments, any debt, your insurance needs and likely spending patterns in retirement.

It’s also important you understand the support you can access from government benefits, not just the age pension but the pension card and associated discounts.

You also need to understand the intersection of the super and retirement income systems as you transition to retirement. That means the tax and social security implications of withdrawing super, making contributions and earning income from work or other investments.

Ben Hillier is General Manager Retirement Solutions, AMP Capital Investors Limited.

Extracted from AMP's 2022 Financial Wellness research with permission. Data from more than 2,000 respondents was collected between mid and late June 2022 and post-weighted based on ABS statistics: gender, age, location, working status, and industry. This article is general information only and as such, does not consider your personal goals, financial situation or needs. AMP recently announced its new retirement income product which we will examine in a subsequent edition.