While Australia does not have an official inheritance tax, that doesn’t mean there won’t be tax bills and administrative delays depending upon how assets are passed on. In some cases, poor estate planning can cost beneficiaries hundreds of thousands of dollars.

The biggest misconception with estate planning is that it is purely about documenting your wishes. Proper estate planning documents wishes while providing options. I leaned on insights from estate planning lawyer Abbey John to understand how wills should be structured.

The cost of avoiding a will

The cost of avoiding a will can be significant. One of the clearest examples involves the family home. Under current tax rules, executors generally have two years from the date of death to sell a principal place of residence and retain a capital gains tax exemption.

John adds that delays are commonly caused by poorly drafted wills or the lack of a will. If you miss the two-year window entirely, there’s little to no chance to save the capital gains exemption.

Without a valid will, families may spend months determining who can act as administrator of the estate, potentially delaying the sale of assets and increasing legal and tax costs. When principal places of residence are held long-term the tax consequences may be significant.

John notes there is an appeal process for an exemption but this involves legal and administration fees that can otherwise be avoided. A successful appeal isn’t guaranteed and requires a strong, valid reason.

I’ve written a deep dive on what to do if you inherit a home here.

Testamentary trusts

Many simple wills merely divide assets without considering how beneficiaries will receive them, including the tax they will pay on sale or how to handle income generated by the asset. One way to divide assets and minimise the tax burden of the estate is a testamentary trust.

Testamentary discretionary trusts are powerful estate planning tools. These trusts are created through a will and only become active after death. Rather than beneficiaries receiving assets directly in their personal name, the inheritance is held within a trust structure.

John describes them as ‘the most tax-advantageous and protective way to receive an inheritance.’

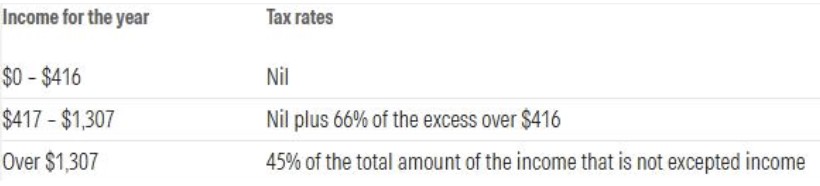

Importantly, testamentary trusts allow distributions to minors to be taxed at adult tax rates rather than punitive minor tax rates. Under standard family trust rules, minors can typically only receive a small amount tax-free each year. Testamentary trusts allow minors to receive the adult tax-free threshold amount.

Figure: Tax rates for residents who are under 18 for 2024–25 without a testamentary trust Source: ATO

With a testimonial trust families may be able to distribute income to children or grandchildren in a tax-effective way to help fund expenses such as education costs.

John charges around $1,100 for a simple will, while a will with a testamentary trust costs roughly $2,000. The trust itself sits dormant until death and does not create ongoing costs while the will-maker is alive. As a rough guide, she says estates of around $250,000 per beneficiary may justify the structure.

Testamentary trusts are not for everyone. They may not make sense for beneficiaries who permanently live overseas and are not Australian tax residents. They do not receive the benefits of structuring for tax minimisation. If the inheritance is relatively small, the ongoing accounting and tax return costs may outweigh potential benefits.

Structuring to get the most out of your super

Superannuation is often one of the most tax-sensitive assets in an estate because it does not automatically form part of your will. Instead, super is governed by the rules of the super fund and your binding death benefit nomination.

Binding death benefit nominations must be made to a valid dependent. If they are not a tax dependent, such as an adult child, they can face tax when inheriting super directly.

In some situations, directing super benefits to the estate instead of directly to adult children may reduce the overall tax burden. Nominating your Legal Personal Representative (LPR) on your binding death nomination form means that adult children will pay tax, minus the 2% Medicare Levy. On large estates, avoiding the Medicare levy is meaningful.

John adds that this strategy only works if the estate plan and binding death benefit nomination are properly aligned.

The biggest mistake with wills

DIY wills can make already emotional situations more complex. DIY or generic online wills are meant as a catch all for the general population and do not take your specific circumstances into account. Broad or general wording leaves the document up to interpretation. Estate planning language must be precise because executors rely entirely on the wording of the document when administrating an estate.

Any ambiguity can increase the risk of disputes and potentially expose executors to personal liabilities.

Three things to review

I finished my conversation with John by asking what are three things that each of us can do to improve the tax effectiveness of their estate plan. She believes the first place to start is a review. The second is assessing whether growing wealth means a simple will is no longer sufficient. The last is ensuring your binding death benefit nomination aligns with your estate plan.

Above all, don’t avoid estate planning because it feels uncomfortable. Dealing with it now ensures that you have the best chances of your wishes being honoured and saves any potential conflict or confusion at an already emotional time.

Shani Jayamanne is Director, Investment Specialist, at Morningstar Australia.