The 2026–27 Federal Budget has unsettled estate planning because it places two structural tax reforms beside a familiar succession-planning vehicle: the discretionary testamentary trust. From 1 July 2027, the first proposed measure would replace the 50 per cent CGT discount for individuals, trusts and partnerships with cost base indexation and a 30 per cent minimum tax on net capital gains. From 1 July 2028, the second would impose a 30 per cent minimum tax on discretionary trust taxable income, with non-refundable credits for non-corporate beneficiaries and specified exclusions.

Those measures are proposed reforms, not enacted law. But Budget announcements can still affect present planning. Many executed wills contain discretionary testamentary trust clauses. If the will-maker is alive, the trust may not yet exist or hold property. On the Budget wording, those wills may sit outside any grandfathering for “discretionary testamentary trusts existing at announcement”. Estate plans settled years ago may therefore require review, because the tax assumptions attached to a future trust may no longer hold.

Testamentary trusts: what they are and why they are used

A testamentary trust takes effect through a will or codicil and is funded because of death. It is not the deceased estate itself. The executor collects assets, pays debts and distributes or sets aside the residue; a testamentary trust may then continue as the longer-term holding vehicle.

The fixed/discretionary distinction is central because testamentary trusts often serve purposes beyond tax. In a fixed testamentary trust, beneficiaries have defined interests in income, capital or both. That structure may suit a will-maker who wants certainty of economic entitlement. A discretionary testamentary trust, by contrast, identifies a class of potential beneficiaries and gives the trustee power to decide who receives income or capital, when, and in what proportions. That discretion is often the mechanism through which the trust performs its protective, succession and governance functions.

It allows the trust to respond as children mature, needs change, or beneficiaries face insolvency, relationship breakdown, disability, addiction, exploitation risk or financial inexperience. It can delay outright control for a young adult, preserve a family farm or closely held business, manage competing claims between active and non-active family members, separate control from benefit, and impose governance around investment or business assets. In blended families, it may also support provision for a surviving spouse while preserving capital for children of an earlier relationship.

Those benefits are not absolute: family law, creditor access and trustee-control issues remain. But many testamentary trusts are not merely income-splitting devices. A tax regime that penalises discretion may therefore affect asset protection, business succession, family governance and intergenerational control, not only tax outcomes.

The tax settings that made them attractive

The current income tax settings are located in Division 6 of the Income Tax Assessment Act 1936 (Cth). Section 96 states that a trustee is not liable to tax except as the Act provides. Where an adult resident beneficiary is presently entitled to trust income, section 97 generally assesses that beneficiary on the corresponding share of net income. Trustee assessment can arise for legal disability, non-residence or absence of present entitlement.

For estate planning, the minor-beneficiary rules are especially important. Division 6AA generally discourages income splitting with minors by applying special rates to eligible unearned income. Section 102AG carves out specified “excepted trust income”, including qualifying income of a trust estate that resulted from a will or codicil. The income is not tax-free; rather, the minor is taxed at ordinary rates. Since the 2019 tightening of Division 6AA, the minor-beneficiary concession for testamentary trusts turns on tracing: income is concessionally taxed only to the extent it is produced by estate property, or by traceable accumulations and replacement assets, not merely because the trust arose under a will. That matters because trustees now need clear records of sale proceeds, reinvestments and mixed funds, and income from injected or untraceable assets can lose the concession and fall back into the harsher tax regime for minors.

CGT supplies another attraction. Death is generally not itself a CGT taxing point. Division 128 of the Income Tax Assessment Act 1997 (Cth) disregards a capital gain or loss from a CGT event happening because a taxpayer dies, and treats the legal personal representative or beneficiary as acquiring the asset on death. Later disposals can still produce taxable gains. Under current law, however, individuals and ordinary trusts can generally access the 50 per cent CGT discount where the asset has been held for at least 12 months, with Subdivision 115-C providing the trust capital-gain attribution machinery.

What the Budget proposes

The CGT proposal is broader than housing. Budget Paper No 2 states that, from 1 July 2027, the 50 per cent CGT discount would be replaced by cost base indexation for assets held for more than 12 months, with a 30 per cent minimum tax on net capital gains. It would apply to all CGT assets, including pre-1985 assets, held by individuals, trusts and partnerships. Transitional rules would preserve pre-commencement gains: the 50 per cent discount would continue for gains accrued before 1 July 2027, while indexation and the minimum tax would apply thereafter. Taxpayers could use a valuation or specified apportionment formula supported by ATO tools.

The discretionary trust proposal is separate. From 1 July 2028, trustees of discretionary trusts would pay a 30 per cent minimum tax on taxable income. Beneficiaries would still return trust income, but non-corporate beneficiaries would receive non-refundable credits. Fixed and widely held trusts, fixed testamentary trusts, complying superannuation funds, special disability trusts, deceased estates and charitable trusts are stated to be outside the measure. Excluded income would include primary production income, certain vulnerable-minor income, amounts subject to non-resident withholding tax and income from assets of discretionary testamentary trusts existing at announcement. Collection, franking-credit and rollover details remain to be designed.

A before and after example: distributions to children and low-rate beneficiaries

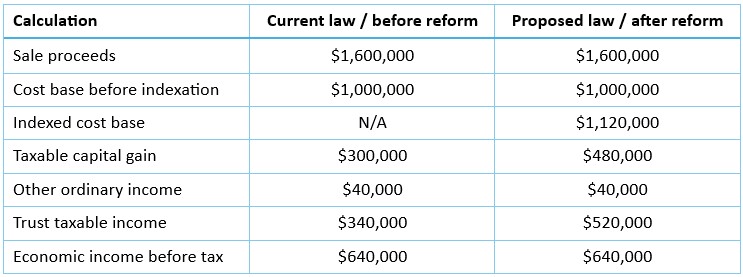

Assume a parent dies after 1 July 2028 and the will creates a discretionary testamentary trust for two minor grandchildren and two adult children. All four beneficiaries have no other taxable income. The trust receives $1 million of estate-sourced assets, later sells those assets for $1.6 million, and also derives $40,000 of ordinary income in the same year. CPI indexation over the holding period is assumed to be 12 per cent. The trustee distributes equally. The example ignores Medicare levy, offsets, franking credits, losses, streaming rules and future legislative refinements. It assumes the minors’ shares are excepted trust income and uses the announced 14 per cent resident rate from 1 July 2027.

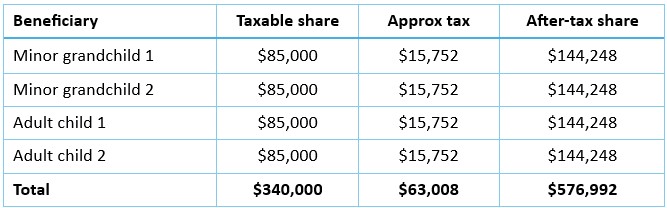

Under current law, the 50 per cent CGT discount reduces the taxable capital gain to $300,000. With $40,000 of ordinary income, trust taxable income is $340,000. If distributed equally, each beneficiary receives an economic share of $160,000 and a taxable income share of $85,000. Ignoring offsets and Medicare levy, each pays about $15,752; total family tax is about $63,008, leaving about $576,992 after tax.

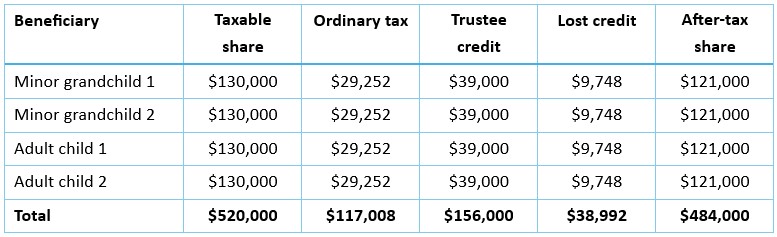

Under the proposed regime, the indexed cost base is $1.12 million, producing a real capital gain of $480,000 and a 30 per cent CGT floor of $144,000. The trust’s taxable income is $520,000, so the discretionary trust floor is $156,000. If allocated equally, each beneficiary has taxable income of $130,000. Their ordinary tax before credits would be about $29,252 each, or $117,008 in total. If trustee credits are equal and non-refundable, each receives a $39,000 credit and loses the excess $9,748. The family group bears $156,000 of tax and the after-tax outcome falls to $484,000.

The two floors should not be added together. Pending final drafting, the capital gain must satisfy a capital-gains floor, while the discretionary trust as a whole may also need to satisfy a broader trust-income floor. Here, the broader $156,000 trust floor absorbs the $144,000 capital-gains floor. The practical effect is still substantial: tax increases by about $92,992 because low-rate beneficiary outcomes are overridden by the non-refundable trustee-level credit design.

Estate planning implications: existing wills, non-tax objectives and fixed trusts

The grandfathering question is acute for people who have signed wills containing discretionary testamentary trust clauses but have not died. The Budget papers protect income from assets of discretionary testamentary trusts existing at announcement. A living person’s will is not the same thing as an existing trust holding assets. If final legislation follows that wording, a testamentary trust arising only after a future death may be a new trust for these purposes. The will may remain valid, but its tax assumptions may have changed.

Nor is the practical response simply to ‘convert to fixed’. As noted earlier, fixed interests may avoid the proposed minimum tax but can undermine the very protective, succession and governance functions for which discretion was chosen. Even for tax purposes, ‘fixed’ is not self-defining: existing concepts often turn on fixed entitlements to income and capital, and variation, appointment or amendment powers can complicate classification.

The reform may therefore force a choice between tax efficiency and fiduciary flexibility. Some families may accept a higher tax cost to retain discretion; others may consider fixed trusts, special disability trusts, direct gifts, superannuation nominations, companies or hybrid drafting. Legislative clarity is needed on whether grandfathering attaches to wills, trusts, assets, income streams, substituted property or realised gains, and how any vulnerable-beneficiary or minor-related exclusion will operate.

Is it a death tax?

‘Death tax’ is not a technical Commonwealth income tax category. In Australian debate it usually refers to an estate duty, inheritance tax or death duty: a tax imposed because wealth passes on death, either on the estate or on recipients. On that definition, the Budget proposals are not a classic death tax. They do not impose an upfront tax on the estate because a person has died. Division 128 remains the enacted CGT rule. The announced trust measure also excludes deceased estates.

That does not make the label politically irrelevant. A future discretionary testamentary trust exists only because someone has died. If income and gains from inherited property are taxed more heavily in that trust, families may experience the measure as part of the fiscal cost of intergenerational transfer. The more precise conclusion is narrower than the public debate sometimes suggests: this is not a tax on death as such, but it may be a higher tax on post-death income and gains from inherited wealth held through future discretionary testamentary trusts.

Conclusion: reform, rhetoric and the design questions ahead

Testamentary trusts have been used to protect vulnerable beneficiaries, preserve family assets, manage blended families, defer control and support business succession planning, as well as to obtain tax advantages. A regime that treats discretionary power as the problem may therefore compromise important non-tax functions, including continuity of family businesses, control of closely held assets and intergenerational governance, unless exclusions and credits are carefully designed.

The hard questions are legislative. Will grandfathering protect wills already signed but not yet activated, or only assets held by trusts on Budget night? How will substituted assets, reinvested proceeds and borrowed funds be traced? How will fixed, discretionary and hybrid testamentary trusts be classified? Will non-refundable credits overtax child and low-rate beneficiaries in cases far removed from high-income avoidance? How will the two floors interact? Until draft legislation answers those questions, careful analysis requires a clear distinction between enacted law, announced policy and political characterisation. The real test of the reform will be whether it can curb tax-driven income splitting without collateral damage to the legitimate protective and succession-planning purposes for which testamentary trusts are often used.

Citation:

Villios, Sylvia, (2026), Budget Forum 2026: Testamentary Trusts after the 2026-27 Budget: Estate Planning, Tax Reform and the “Death Tax” Debate, Austaxpolicy: Tax and Transfer Policy Blog, 29 May 2026, Available from: https://www.austaxpolicy.com/testamentary-trusts-after-the-2026-27-budget-estate-planning-tax-reform-and-the-death-tax-debate/

Dr. Sylvia Villios is an Associate Professor at the Adelaide Law School, University of Adelaide. Dr. Villios researches and teaches in taxation law, particularly focusing on questions about the operation of the Australian tax system, taxation policy, corporate taxation and the role, powers and accountability of the Commissioner of Taxation.