The legislation to implement the capital gains tax changes announced in the May 2026 Federal Budget sailed through the House of Representatives but will obviously face a tougher crowd in the Senate. If it’s passed, it won’t impact super funds at all. But since it impacts most of the alternatives to super, will it change the considerations for people facing Division 296 tax?

In a nutshell – the changes make it less attractive to withdraw money from super. That doesn’t mean no-one should do it, but the changes weaken the case for taking action. (Helpful of the Government to do this immediately before 1 July 2026 when the new tax is due to start.)

At the moment, the comparison between super vs non super has been quite simple for Division 296 tax. Because the amount of a capital gain has been calculated in the same way for all types of taxpayer (sale price less original cost), the only differences have been:

- the extent to which the gain is discounted before it’s taxed, and

- the relevant tax rate.

To date, I’ve found this table quite a useful way of explaining things to clients:

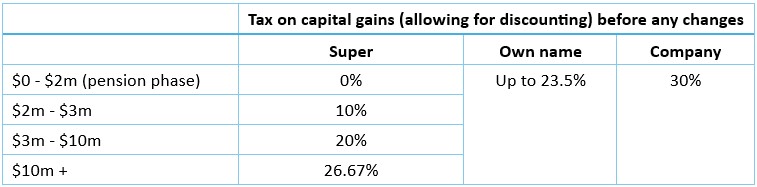

Table 1: Current rules

The super rates all allow for the fact that capital gains are eligible for a one-third discount. They also reflect the fact that different rates of tax apply for different ‘slices’ of an individual’s super when we take Division 296 tax into account. The 26.67% figure in the table above, for example, is two-thirds of 40% (the total tax applied to earnings relating to the balance above $10 million – being 15% fund tax plus an extra 25% Division 296 tax).

The tax rate shown for an individual assumes that the people we’re talking about (people with Division 296 tax problems), usually already have income in their own name. While that income alone might not be able to push them into the top marginal tax rate every single year, a large capital gain certainly would. Hence I’ve assumed capital gains, after discounting, would be taxed at 47% (and 23.5% shown in the table above is 47% x 50%).

In future, the tax rate (let’s assume it’s 47%) will be applied to a capital gain calculated in a totally different way (sale price less an inflation adjusted cost base). That means we can’t just compare tax rates.

So how can we compare outcomes?

I suggest we come up with a specific metric for the comparison. I’d calculate this amount:

This is a completely artificial number – it’s not a tax rate, it’s just a comparison tool. I’ve called it the comparison rate.

So how do we put this to use?

First, we need to consider the variables at play to make sure we compare genuinely different scenarios. Given the changes for individuals and trusts will mean the capital gain subject to tax is now worked out based on an inflation adjusted cost base, the level of inflation vs growth in the asset is obviously a key one.

If inflation is high and asset growth is low, for example, the new method will actually demand very low amounts of tax.

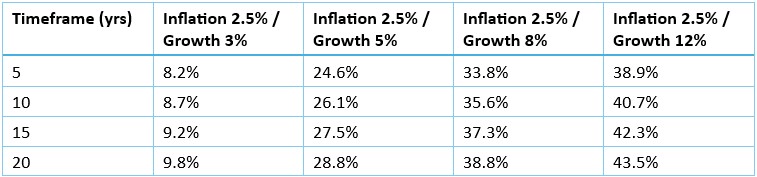

To use an extreme example – if inflation is 2.5% pa and the asset only grows by 3% pa, a $100,000 asset will have grown to around $134,400 in 10 years. The indexed cost base will have grown to $128,000. The new approach will see only $6,400 ($134,400 - $128,000) subject to tax (a tax bill of $3,000 at the highest marginal rate of 47%). This is equivalent to a tax bill of 8.7% of the whole capital gain (ie, $3,000 is 8.7% of $34,400). This is my ‘comparison rate’ above – ie the rate we can compare to the super fund rates above.

In contrast, the same asset held in a super fund would have a $34,400 capital gain ($22,900 after discounting) and a tax bill of $9,200 if we assumed the highest possible tax rate of 40%. That results in a comparison rate of 26.67% - as per Table 1 above. In other words, the comparison rates for the various slices of super are still exactly as shown in Table 1. (This isn’t actually how super fund taxes or Division 296 tax work. In real life, every $1 of capital gain is divided between the various slices but hold that thought for a moment.)

In contrast, if the asset grew at 8%, the tax bill if it’s sold after being held personally would be more like $41,300 (which equates to a tax rate of around 35.6% on the capital gain of $115,900). Remember this isn’t a real tax rate (this is still assumed to be 47% on the capital gain relative to an indexed cost base), it’s just a way of expressing the tax paid in a way that makes it directly comparable to the rates in the table above.

The table below shows a range of ‘comparison rates’ – ie, the effective tax burden for a given mix of inflation and growth, expressed as a percentage of the overall growth. Note the equivalent rates for super don’t change – they’re still the same as Table 1.

Table 2: Comparison rates under different scenarios for assets held personally, top marginal tax rate of 47% applies

What does this tell us?

- Low growth: personal ownership is more attractive. While the tax rate is still 47% in my calculations, the amount of capital gain it’s applied to is so small that the tax rate “feels like” the figures in the first column (the comparison rates). Remember, if the CGT rules weren’t changing, every figure in this table would be 23.5% (47% tax on 50% of the capital gain).

- Moderate / high growth: super becomes more attractive. It doesn’t take much growth (as little as 5% relative to inflation of 2.5%) for the tax rate to feel much higher. Many of the comparison rates in the table above are higher than the top rate for super (26.67%).

What about the new minimum tax rate of 30% on capital gains?

This isn’t relevant for my analysis here – I’ve assumed a tax rate of 47% in all scenarios (thanks to the individual’s other income). While it’s a highly relevant change for other people, I’m guessing those with very large amounts in super who might make big withdrawals to avoid Division 296 tax aren’t paying tax at less than 30% on any of their income – let alone capital gains.

One more very important feature of CGT in super

When personal assets are sold and subject to capital gains tax, it’s easy to focus on marginal rates because we can assume ‘other income’ will push the recipient into a higher rate of tax. (This is why the above focussed entirely on 47%)

It’s not quite the same for super funds.

Because the tax rates depend on wealth not income, even when a member has more than $10 million in super, every dollar of income and discounted capital gains will be split into various parts – with some taxed at 0-15%, some at 30% and some at 40%.

Technically, then, the super fund tax rates applicable to a particular amount of capital gain will be lower than the ones shown in the table above. But in order to consider whether to leave money in super vs withdraw it, I usually feel the “marginal rate” approach is a more helpful proxy for the real impact of the choice to leave money in super or withdraw it.

My logic is something like this:

- Imagine someone with $15 million in super – who’s wondering whether to withdraw $5 million (the part triggering the worst possible tax rate of 40% on some of their super earnings),

- If they leave it in super, one-third of all capital gains will be taxed at 40% (after discounting)

- If they take it out, none of their super fund’s capital gains will be subject to 40%,

- In other words, leaving that $5 million in super lifts the tax paid on even capital gains that relates to the first $10 million,

- That means a more valid proxy for the impact of leaving that $5 million in super is to assume capital gains are taxed at 40% in working out the comparison rate. It will tend to overstate the tax cost of staying in super but it’s still reasonable.

Of course, there is a lot an individual can do to better manage their tax liabilities in super but even using my basic arithmetic, the decisions facing those with large super balances just got harder!

Meg Heffron is the Managing Director of Heffron SMSF Solutions, a sponsor of Firstlinks. This is general information only and it does not constitute any recommendation or advice. It does not consider any personal circumstances and is based on an understanding of relevant rules and legislation at the time of writing.

For more articles and papers from Heffron, please click here.