SpaceX’s long anticipated IPO went smoothly. The shares opened above the offering price before finishing its debut knock 19% higher. Heavy subscription by institutions and retail investors meant allocations were slim, leading to strong demand once shares began trading.

SpaceX (SPCX.NAS) is now the 6th-largest US listed company, exceeding Tesla in terms of market capitalisation. The initial public offering price valued SpaceX at US$135 per share. Morningstar’s fair value sits at US$63, less than half the offer price. SpaceX investors are being asked to cough up today for a set of future possibilities that may or may not ever materialise.

So why does this impact the everyday Aussie? When a behemoth of a company like SpaceX lists, it becomes part of the global index ecosystem. This involves a complex web of index inclusion rules that flow through to superannuation funds and passive ETFs. For Australians, that process is where the IPO starts to impact your future, whether you like the company or not.

Firstly, understanding the valuation allows investors to get a better grasp on why the index implications really matter.

Why we think SpaceX is overvalued

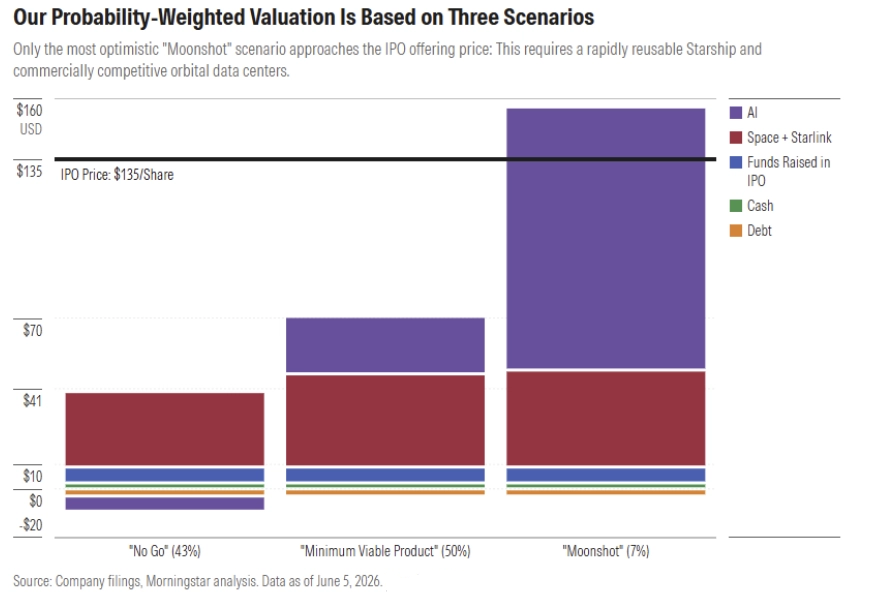

Morningstar analyst Nicolas Owens highlights a significant gap between the IPO price and the intrinsic value for SpaceX. SpaceX’s future depends on the successful execution of technologies that are not yet proven at scale, particularly around rapidly reusable rockets and the commercialisation of launching data centres into space. To address this, our analyst created three scenarios for SpaceX and weighted them on probability.

Nicolas noted that even at US$63 per share, a significant amount of leeway was given in two of the three scenarios. In these two scenarios, Nicolas assumes the company can achieve a rapidly reusable Starship rocket enabling multiple launches per week and successfully commercializes data centres in space. Neither problem has been solved and both remain years away from fruition.

In the most optimistic ‘moonshot’ scenario, the company would be worth $1.97 trillion or $154 a share which is 3% below the closing price on Friday. However, Nicolas assigns this scenario, in which both Starship is reusable and scaled orbital data centres are highly successful, a 7% chance of happening.

The core space and connectivity businesses (think Starlink) adds around US$40 per share and is the key driver in two of the three scenarios. The three scenarios for the AI segment add $16.50 to our overall valuation estimate. The AI segment drives upside in the best case however contributes no value in the worst.

Based on the three scenarios, the most likely scenario according to this model is that orbital data centres are viable and benefit from SpaceX’s decreasing cost to launch from Starship. While the technology is not yet proven, SpaceX is best positioned in the industry to capitalise on the endeavour. This scenario models space data centres generating US$47 billion in revenue by 2035.

Why index inclusion matters

The path from IPO to widespread ownership is governed by index providers. Typically, a newly listed company doesn’t go straight into the S&P 500 or the Nasdaq 100. It needs to establish a trading history, demonstrate sufficient liquidity and meet minimum free float requirements.

For flagship benchmarks like the S&P 500, profitability is also a key hurdle. These rules exist to ensure indexes can avoid illiquid or highly speculative companies. This also helps index funds replicate index performance with minimal tracking errors.

Index inclusion triggers forced buying, as index funds must replicate benchmark weights. The result is a synchronized wave of buying that has little to do with valuation and everything to do with rules. Interestingly, despite the size of SpaceX, its float-adjusted market cap is only US$90 billion. This means SpaceX will not immediately be one of the largest holdings in broad index funds. Its small initial float limits the immediate size in many index funds. For example, the SpaceX weighting is expected to initially collect less than 0.20% of Vanguard Total Stock Market ETF VTI once added.

As locked-up shares from insiders become available to sell, the float-adjusted market capitalisation will increase. This will also increase the weighting in index funds and ETFs which will trigger ongoing buying as funds rebalance. Most Australian superannuation portfolios have substantial exposure to global equities, either through passive vehicles or mandates that closely track major indices.

The index timeline

SpaceX is expected to be added to several indices over the next month, while inclusion in the S&P 500 will likely take at least 12 months due to additional profitability requirements. Once included, exposure flows quickly into superannuation portfolios through routine rebalancing.

In practical terms, many Australian investors will own SpaceX indirectly within one to two years of its IPO, regardless of whether they actively follow the stock. The weighting is expected to increase over time as insiders sell shares and expand the free float. As a result, the short-term impact is minimal but weightings in portfolios are likely to rise steadily over time.

The big picture for Aussie investors

For Australian investors, the key takeaway is straightforward: you don’t need to own SpaceX intentionally for it to influence your portfolio. As the company moves through index inclusion, it will be absorbed into superannuation funds via passive allocations and benchmark linked mandates.

Crucially, that exposure reflects index mechanics rather than valuation discipline. In a market where probabilities are being priced aggressively, it’s important to understand both the index mechanics and the valuation fundamentals. This will help investors shape their own assessment of SpaceX and the market implications from the recent IPO.

Tyger Fitzpatrick is an Associate Investment Specialist at Morningstar Australia, writing for retail investors and advisers on equity markets. He also authors Morningstar’s Ask the Analyst column.