There are several studies that show that retail clients who get advice from brokers do not end up with better portfolios or improved performance. Here is a classic study from Canada that shows that while good advisers can create enormous value for clients, the average adviser does not. What made me perk up, though, was when I came across a study of clients in the rarefied world of German and Swiss private banking that shows a result to the contrary.

Maria Maas and her colleagues managed to convince a German private bank with offices in Germany, Switzerland, and Luxembourg to hand over 969 client portfolios. Of these, about 800 portfolios were self-managed by the clients, while about 160 were managed with the help of an adviser from the bank. Note that the differences between the advised and non-advised clients in this case are tiny. 92% of the clients are German, all of them have substantial financial assets (otherwise they wouldn’t be clients of the bank), and they all have very similar levels of income, age, risk profile, and financial literacy. The only real difference was the use of an adviser or the lack thereof.

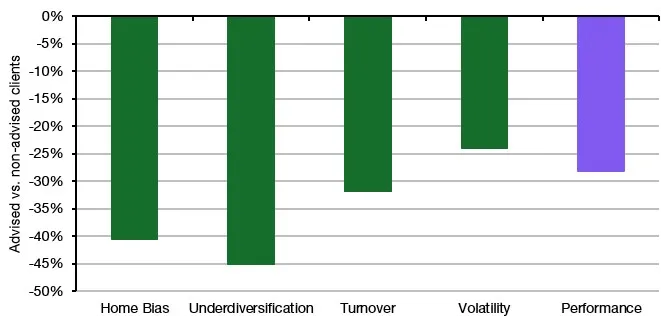

Below is a chart that summarises the key differences in terms of portfolio risks and behavioural biases between advised and non-advised clients. A negative number means that clients using an adviser have better (read: less risky) portfolios.

Difference between advised and non-advised clients’ portfolios

Source: Maas et al. (2025)

As you can see, the chart shows that clients who use an adviser have, on average, less of a home bias and more diversified portfolios. This directly contradicts the results of the Canadian study I linked to above. Clients who use an adviser also have portfolios with lower volatility and generally have lower turnover in their portfolios – something that has long been established as a key driver of underperformance.

But also note that despite these more diversified portfolios and the reduced turnover, the average return of the advised clients’ portfolios is lower than the return of the non-advised clients.

The authors of the study claim that advisers in this private bank are giving good advice because they reduce risks and behavioural biases in client portfolios. But one chart in the paper caught my attention. And I think that gives a hint at the true story.

Forgive my cynicism. As someone who has worked in Swiss private banking for almost 20 years, I don’t think private bank advisers are any better than retail advisers in Canada or anywhere else, for that matter. And the overwhelming evidence in previous studies points to advisers not adding any benefit to clients, on average (again, a good adviser can make a big difference, but you first have to find a good adviser).

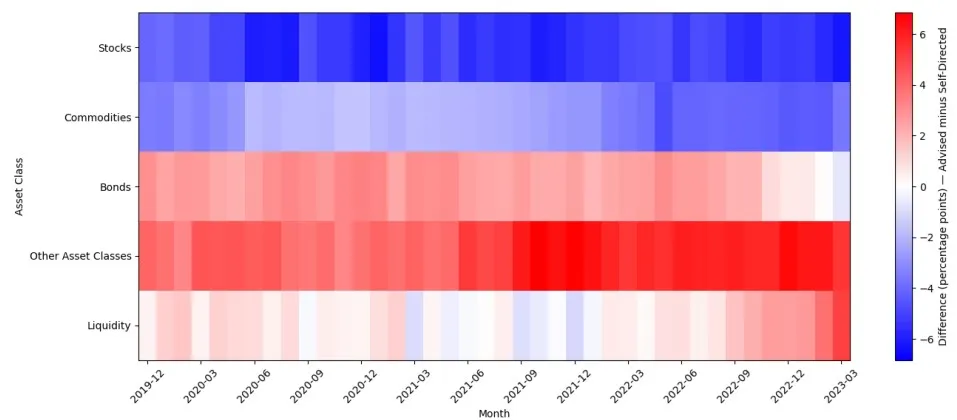

Below is that chart from the paper. It shows the average difference in portfolio allocation between advised and non-advised clients over time. Blue shades indicate that non-advised clients have a higher allocation, red shades indicate advised clients have a higher allocation.

Average difference in allocation

Source: Maas et al. (2025)

The chart shows that non-advised clients have more equities and fewer alternatives and bonds in their portfolio. Indeed, every private bank adviser will tell you that the incentive structure for them is such that they are trying to sell funds and preferably funds with high fees to the client.

Compared to non-advised clients who predominantly think about single stocks, this means that diversification is almost certainly higher in advised portfolios, while home bias and portfolio turnover are lower. That alone reduces volatility considerably.

But over the last twenty years, the trend has also been towards recommending alternative asset funds (hedge funds, private equity, infrastructure, etc) to clients because they promise additional diversification to the client and higher fees to the bank advising the client. Unfortunately, these alternative asset classes often end up with higher fees but lower returns than a simple stock/bond portfolio.

The result is that clients who use an adviser end up with more diversified and lower risk portfolios, but also with lower returns and almost always higher fees. I can’t prove that this is what is going on in this study, but I think my explanation is a bit more likely than assuming that private bank advisers are somehow better than their peers who work at brokerage firms or advise retail clients.

Joachim Klement is an investment strategist based in London. This article contains the opinion of the author. As such, it should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of the author’s employer. Republished with permission from Klement on Investing.