The Strait of Hormuz has been described as the world’s most critical energy artery, but in February 2026, that artery was effectively severed. As conflict between the US and Iran escalated, the closure of this passage didn’t simply spike the price of oil — it broke the global supply chain for refined products in ways that have no modern parallel, not even the 2022 Ukraine crisis.

2022 vs 2026

The 2022 Ukraine energy crisis was severe, but its oil impact was one of trade redirection, not physical destruction. While the International Energy Agency (IEA) initially forecast that 3 thousand barrels per day (mbpd) would be removed from global markets, the actual production reduction was smaller - Russian oil was diverted to new buyers in Asia and Turkey, often at a significant discount to bypass Western sanctions. Refineries outside Russia ran flat out to capture soaring margins. The system strained but did not break.

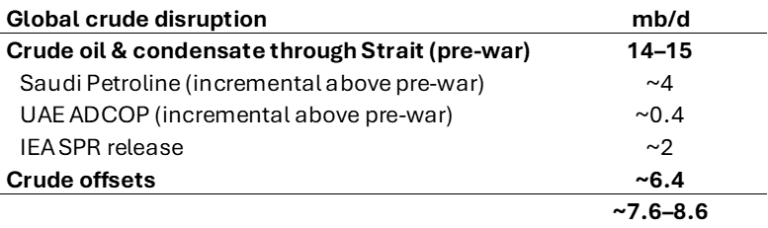

The 2026 Iran energy crisis is categorically different. The Strait blockade has physically trapped an estimated 14 to 15 mbpd of crude - roughly five times the peak disruption of the Ukraine crisis. Unlike 2022, however, the market entered this conflict with high global crude inventories, providing an initial buffer. Several emergency mechanisms have since cushioned the impact further. The IEA coordinated a record 400 million barrel strategic reserve release - more than double the 2022 response - delivering approximately 2 mbpd to the market. Saudi Arabia ramped its Petroline pipeline from 3 mbpd to its 7 mbpd ceiling, generating approximately 4 mbpd of incremental exports, while the UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP) lifted an estimated 0.4 mbpd above pre-war throughput. Together these factors have prevented the crude price spiralling out of control, even as roughly half the total Hormuz shortfall remains unmet.

Sources: IEA OMR March 2026; S&P Global; EIA; Rystad Energy.

The refined product problem

The crude market has partial buffers. The refined product market has none. The Strait carries about 5 to 6 mbpd of refined products – petrol, diesel, and jet fuel – representing roughly 19% of all global seaborne trade in finished fuels. Unlike crude, there is no pipeline or alternative route through which these products can bypass the chokepoint.

The disruption does not stop there. Of the 14–15 mbpd of Gulf crude normally transiting the Strait, approximately 80% flows to Asian refineries. That feedstock loss is now spreading rapidly across the region in the form of refinery run cuts. In China, Sinopec has cut throughput by more than 10% while smaller teapot refiners have lost access to nearly 1.4 mbpd of Iranian crude imports. In Singapore, ExxonMobil’s Jurong Island operations have been cut to 50% or lower and Singapore Refining Co has reduced runs to 60%. Accounting for the full extent of cuts across Japan, South Korea, Taiwan, and smaller regional refiners, Wood Mackenzie estimates the total Asian run cut at 4 to 5 mbpd. Combined with the direct loss of Gulf refined product exports, the total shortfall reaches 9 to 11 mbpd — far exceeding anything the crude offsets can address.

Sources: IEA OMR March 2026; Wood Mackenzie. Approximate.

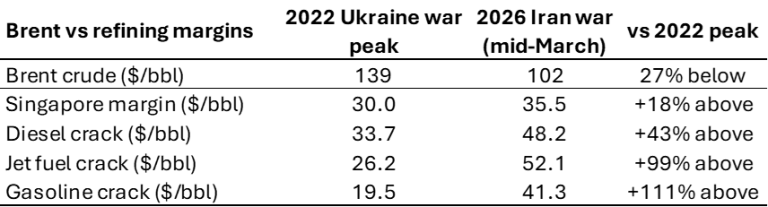

The result is a refined product market under a degree of stress that makes the 2022 Ukraine crisis look mild by comparison. The crude price is below its 2022 peak while every refined product price is well above it.

Sources: Reuters/EIA; LSEG; Wood Mackenzie. 2026 figures as of mid-March 2026.

The jet fuel crack spread at $52.10 per barrel — nearly double its 2022 peak — is forcing airlines to respond. Qantas has raised international fares by approximately 5% and warned that some routes may become uneconomical if prices remain elevated. Air New Zealand has cancelled approximately 5% of its schedule through early May.

The aviation impact is just one dimension of Australia’s broader economic exposure. The country imports roughly 90% of its liquid fuel as refined product from Asian refining hubs — South Korea accounts for 32% of imports, with Singapore (23%) and Malaysia (23%) making up most of the remainder. While direct Gulf imports are negligible, approximately 59% of the collective crude intake for Australia’s top suppliers transits the Strait. Australia does not import Gulf fuel directly, but the Asian refineries providing its supply are critically dependent on that Middle Eastern feedstock.

Australia’s two remaining domestic refineries — Ampol’s Lytton in Brisbane and Viva Energy’s Geelong facility — provide a partial buffer, sourcing crude primarily from Southeast Asia and Africa, but they meet less than 20% of national consumption. With Asian refiners cutting runs and China and Thailand suspending fuel export contracts, competition for available refined product is intensifying rapidly. Australia’s 29 days of petrol reserves and 25 days of diesel provide a buffer — but one that is rapidly depleting as international supply lines tighten.

Conclusion

The global refined product supply chain is only as resilient as its narrowest physical chokepoint. Where 2022 was a price shock the market absorbed through trade redirection, 2026 is a physical blockade compounded by infrastructure destruction and a regional ‘feedstock famine’.

The crude oil market has been partially protected by the policy tools available to governments and the IEA — reserve releases, pipeline diversions, emergency output increases. These mechanisms, while imperfect, have provided a meaningful buffer for global crude benchmarks. For refined products, no such safety net exists. The finished fuel that used to flow through the Strait cannot be rerouted or replaced from alternative sources. Until the Strait reopens, the world remains in a structural fuel deficit and no policy tool currently deployed can change that.

Jason Teh is a Portfolio Manager at Clime Investment Management Limited, a sponsor of Firstlinks. The information contained in this article is of a general nature only. The author has not taken into account the goals, objectives, or personal circumstances of any person (and is current as at the date of publishing).

For more articles and papers from Clime, click here.