For all the talk of energy transitions, oil and gas markets remain at the centre of the global economy.

When oil and gas are cheap, inflation is low and growth is strong. When they rise sharply, the opposite usually follows.

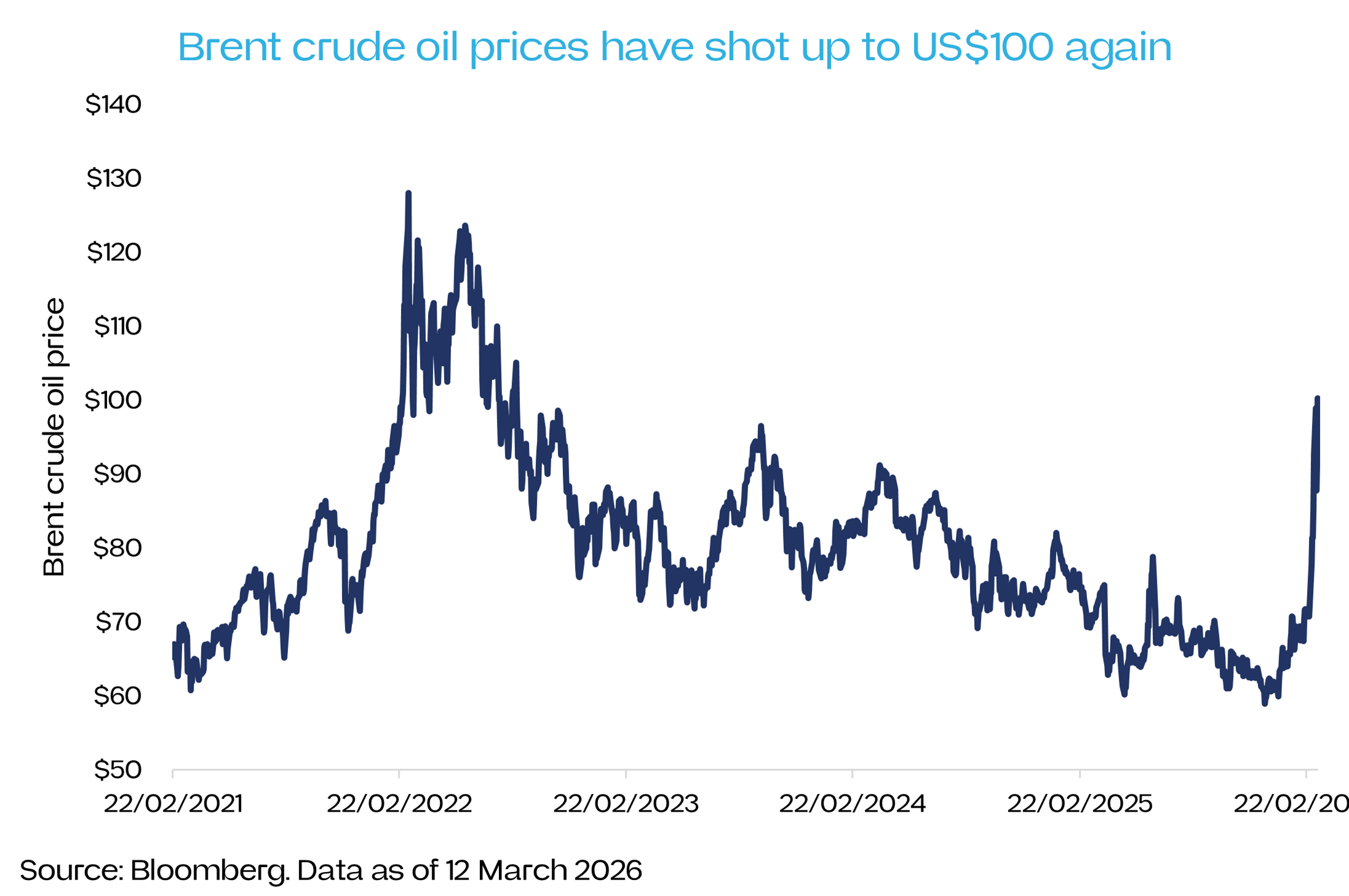

That matters for Australia because oil and gas are becoming more expensive as the US escalates its war with Iran.

Reflecting this, banks are raising their inflation forecasts and trimming their growth outlook.

That is about to matter in a big way for Australian households – especially mortgage holders, as high inflation forces central banks to keep interest rates higher for longer.

Why oil matters so much for inflation

Some conservative political commentators claim high oil prices are being used as a scapegoat for local inflation.

But oil and gas prices truly do have an outsized impact on inflation.

Petrol alone accounts for roughly 3% of CPI. Electricity and gas add several percentage points more. In total, energy-related components typically make up around 6–8% of the inflation index directly (exact numbers differ quarter to quarter).

That may sound modest, but what people often miss are the indirect impacts. Energy prices show up elsewhere through second-order effects.

Plastic is one example. Plastic comes from crude oil, and it appears everywhere in the modern economy: children’s toys, refrigerators, medical equipment such as syringes. When oil prices rise, these costs rise too.

Food is another example. Agriculture depends on fertiliser, which is produced using natural gas through the Haber process. Higher gas prices therefore raise fertiliser costs and ultimately food prices.

Transport and freight is another channel. Everything in the supermarket has travelled there by truck, ship or plane, meaning fuel prices ultimately feed into shelf prices.

Economists estimate that a sustained US$10 increase in oil prices can add roughly 0.2–0.3% to inflation in developed economies. If oil rises from US$80 per barrel to US$100 and stays there, the impact on inflation could approach 1% over time.

For a country already struggling to bring inflation back to target, that is significant.

The strategic importance of the Strait of Hormuz

The reason oil and gas markets – and inflation expectations – have reacted so strongly to the war with Iran is geography.

About 20% of global oil and gas supplies pass through the Strait of Hormuz, making it (along with the Strait of Malacca near Singapore) the most important chokepoint in global commerce.

Tehran knows this and has made targeting the Strait with mines, drones and missiles central to its campaign.

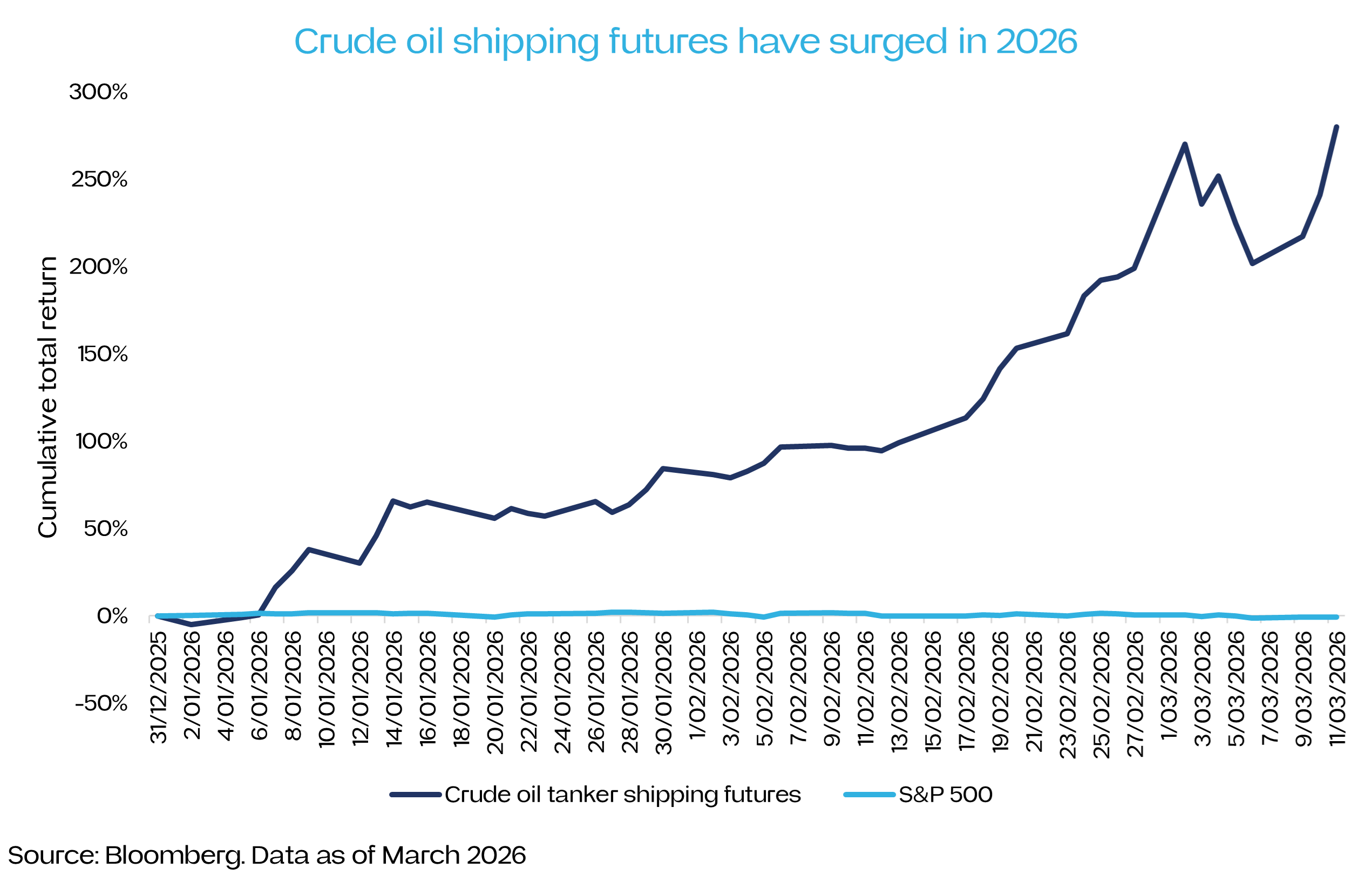

Major shipping companies such as Maersk have stopped sending vessels through the Strait altogether. Crude oil tanker shipping futures have surged more than 250% in 2026 as of 12 March, making them the best-performing asset class of 2026 so far.

Meanwhile, oil futures are now in a structure known as backwardation, which can create negative medium-term consequences.

Backwardation simply means the price of oil today is higher than the price for delivery months or years in the future.

This creates a strong incentive for traders to sell oil immediately rather than store it. And it is happening at the same time governments are drawing down strategic reserves.

The result could be a market with fewer reserves available as both governments and private traders sell down inventories.

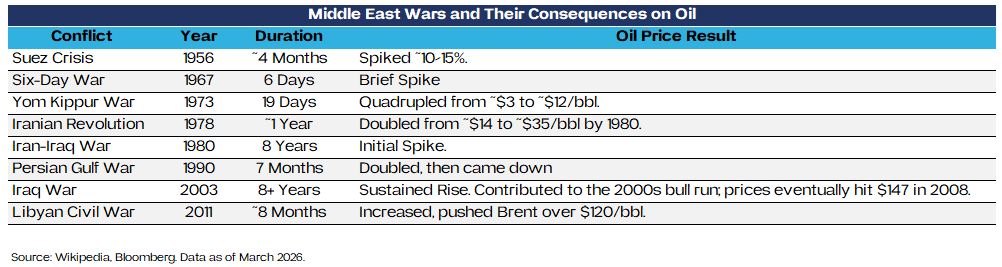

How long will the war last?

Complicating matters further is that no one knows how long the war will last or what the medium-term need for reserves may look like.

Political leaders rarely announce they are embarking on a long war.

When the First World War began in 1914, many leaders said it would be over by Christmas. It ultimately lasted four years. When George W Bush began the war in Afghanistan in 2001, few imagined it would last two decades.

Statements from figures close to Donald Trump – such as Israeli prime minister Benjamin Netanyahu and US defence secretary Pete Hegseth – suggest the current conflict could persist for some time.

Markets therefore face uncertainty not just about the timeline of the war, but also about how it might end. Diplomatic breakthroughs can arrive suddenly or gradually, peacefully or violently.

For central banks, that uncertainty itself becomes a problem.

The squeeze on Australian households

For Australian households, inflation was already elevated at the start of the war.

Immigration policy has been a major driver. Despite widespread public concern, migration numbers have remained far higher than domestic housing supply can sustain. As a result, rental vacancy rates have fallen, and rents have risen sharply across major cities.

Rent is a large component of CPI – larger than energy itself. Rising rents therefore push both inflation and the RBA’s cash rate higher.

Higher oil prices and strong immigration together mean the two main inflation drivers – energy and shelter – could be rising simultaneously in 2026. That creates a headwind for living standards across the mortgage belt.

How should investors think about this?

Within this bleak picture, investors may wonder if there is anything they can do.

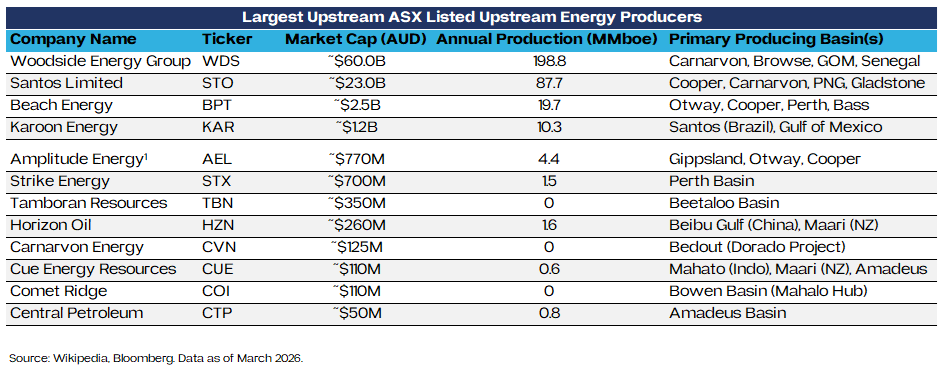

One approach might be ASX upstream oil and gas producers. They make more money when oil and gas prices rise.

Choices are limited though. In Australia, like other parts of the world, oil and gas production is dominated by a small handful of companies.

Woodside and Santos are the largest by far. After them, only Beach and Karoon Energy have market capitalisations above $1 billion. After that, it is a pool of more small speculative developers like Horizon Oil and Carnarvon Energy.

Both Woodside and Santos sell oil and gas under long-term contracts linked to global energy prices.

This means rising oil prices tend to push their revenues and share prices higher.

That means the companies’ shares can act as something of a hedge against rising energy prices for Australian investors. Their dividends typically rise when oil and gas prices are higher too.

Even households that do not own energy stocks may see some relief from ASX producers.

East coast gas prices largely follow international markets. But the Australian government retains the power to force producers to sell domestically at discounted prices, as it did in 2022 following Russia’s invasion of Ukraine.

Oil is different. Australia produces little crude oil and is almost totally dependent on imports.

The only major lever available to the government – via the RBA – is the exchange rate. Because oil is traded globally in US dollars, a stronger Australian dollar reduces the local currency cost of buying oil.

Conclusion

There is a risk the US-Iran war becomes a large income transfer from energy consumers to energy producers, and from borrowers to lenders.

An extended conflict could place further pressure on Australian household finances.

For investors, ASX oil and gas companies may offer a partial natural hedge. But for the broader economy, it would be far better if the war ended quickly and peacefully.

David Tuckwell is the Chief Investment Officer at ETF Shares, a sponsor of Firstlinks. He is also a journalist and researcher specialising in finance and international politics.

Disclaimer: This article is issued by ETF Shares Management Limited (“ETF Shares”) (ABN 77 680 639 963, AFSL: 562766) and ETF Shares is solely responsible for its issue. Under no circumstances is this article to be used or considered as an offer to sell, or a solicitation of an offer to buy, any securities, investments or other financial instruments. Offers of interests in any retail product will only be made in, or accompanied by, a Product Disclosure Statement (PDS) and target market determination (TMD) available at www.etfshares.com.au.