The last time global real estate investment trusts (GREITs) lagged global equities by as much as they do now, Australia was over-excited about One.Tel and living rooms crackled to the sound of dial-up internet.

The dotcom bubble had left REITs for dead. Then the bubble burst and REITs did what neglected asset classes tend to do when normality returns; they bounced back.

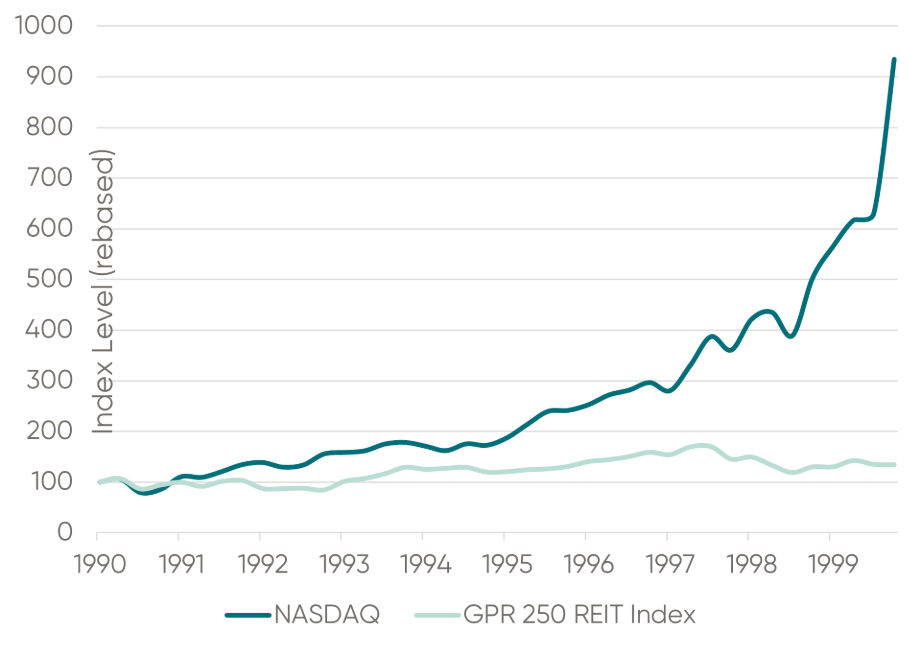

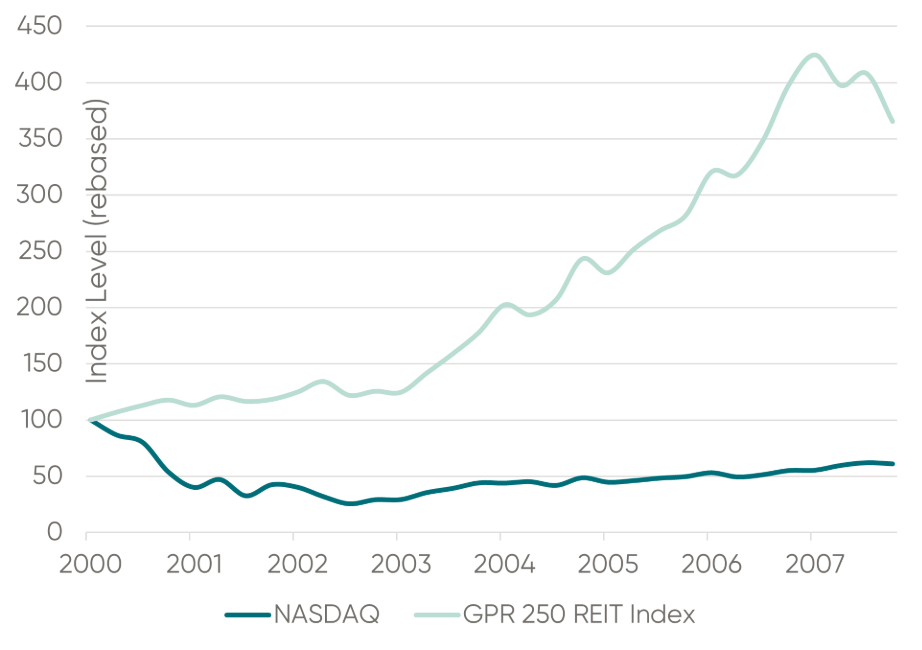

Figure 1 shows the US NASDAQ index between 1990 and 1999 outperforming global REITs, while figure 2 shows their resurrection.

Figure 1: NASDDAQ vs. Global REITs leading into the Dot-com Bubble

Figure 2: NASDDAQ vs. Global REITs after the Dot-com Bubble

Source: JP Morgan Research, DXAM. Past performance is not a reliable indicator of future performance

Today’s circumstances aren’t identical, but the echoes are audible. Global REITs have now underperformed global equities for four consecutive years, the longest period in over two decades.

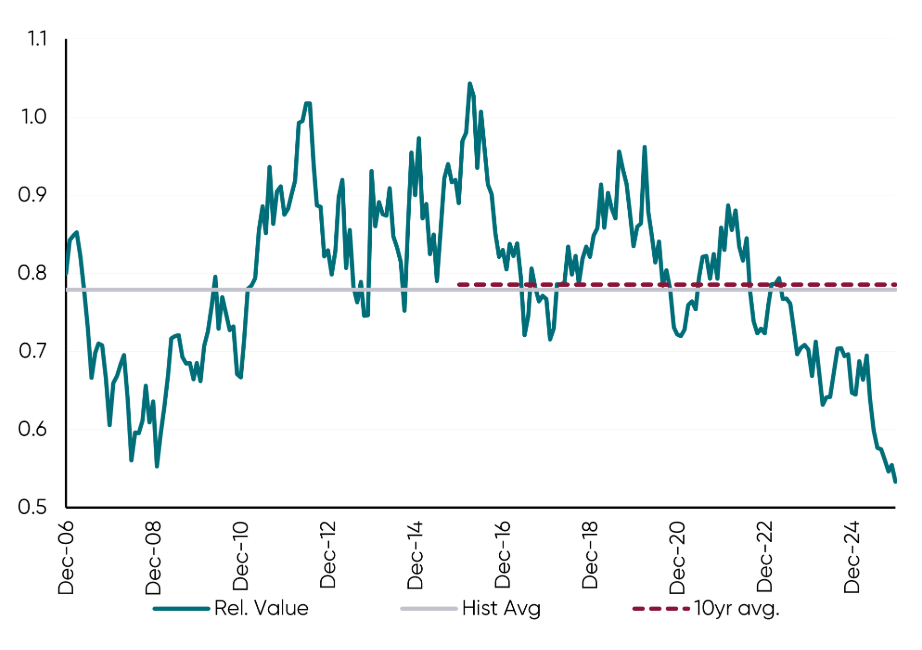

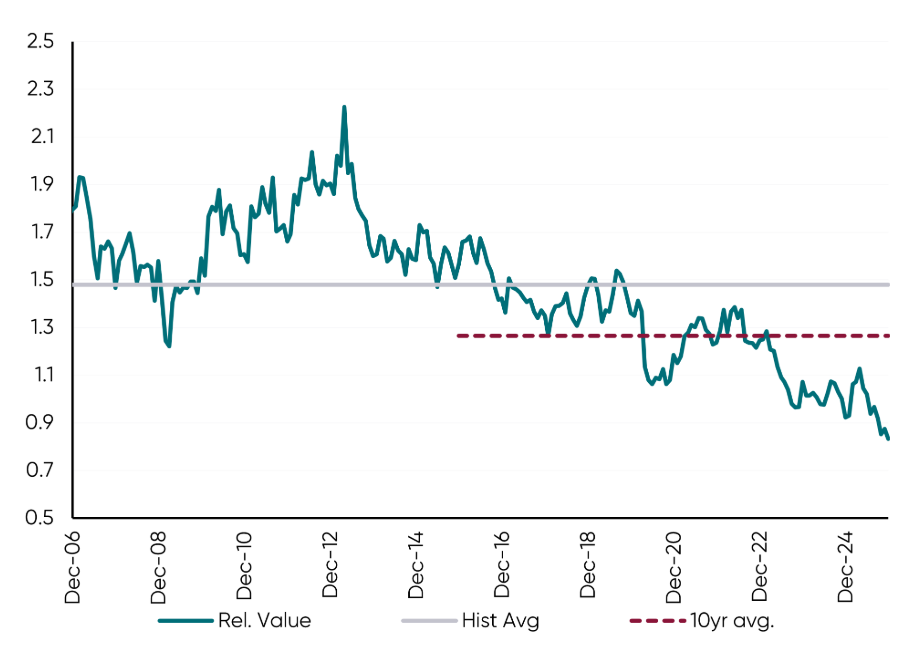

Unlike in the Dotcom era and the pandemic, recent pessimism has accumulated slowly. The effect, however, has been the same. Relative to equities, on key valuation measures GREITs are trading significantly below historical averages.

The purported impacts of artificial intelligence (AI) at one end of global markets has created some speculative excess. At the other, in commercial property, there are ongoing macroeconomic concerns, compounded by the shift to work-from-home, white collar employment and cost of living pressures.

The result is that GREITs have been all but forgotten. Relative valuations have plumbed levels not reached in decades.

Figure 3: Price / book value – Global Listed Real Estate vs Equities

Figure 4: Price / cash flow – Global Listed Real Estate vs Equities

Source: DXAM, UBS. Past performance is not a reliable indicator of future performance.

For an active investment strategy, where investment decisions are based on data more so than narrative, this is a time of opportunity.

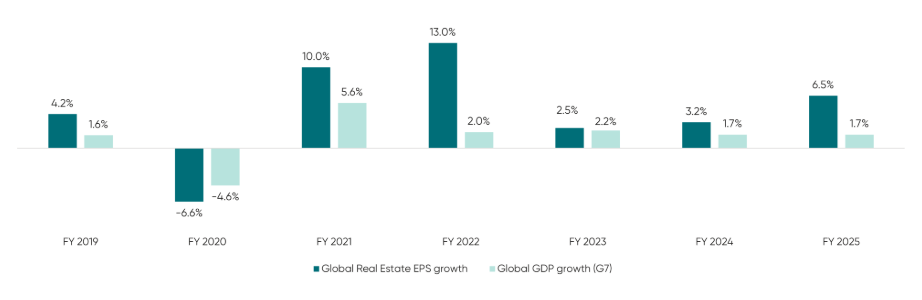

The evidence is compelling. GREIT earnings rebounded strongly after the pandemic and have actually exceeded economic growth after conditions normalised. While the returns in the chart below suggest some volatility, they do not substantiate the discounts implied by public market pricing. Indeed, earnings growth shows increasing momentum, in our view.

Figure 5: Historical global real estate sector earnings growth vs. GDP growth*

Source: IBES, Datastream, UBS, DXAM.

*This graph has not been prepared by DXAM and the information in it is predictive in nature. Global EPS & GDP growth (YoY) is average of US, UK, EU, AU, JP, HK, and Singapore.

There are other reasons for investors to be enthusiastic

First, commercial property is primarily an investment in an income stream. Leases are contractual and long-term, rents typically rise with or ahead of inflation and revenue is reliable. GREITs are classically defensive assets, with growth potential.

Due to booming equity markets, many investors are now underweight real estate. This is an opportune time for investors to rebalance their portfolios, lock in some gains and increase their exposure to GREITs, in our view.

Second, these defensive characteristics are available at compelling prices. We believe GREITs might be well positioned to outperform equities, offering dividend yield, earnings growth and valuation upside. On a risk-adjusted basis, low-teens returns may be a realistic expectation, although not all GREITs are created equal.

Third, the strength of the investment case is unlikely to be undone by expanding supply. Construction and financing costs are now higher and projects have been delayed or shelved. Implications of this dynamic is likely to be ongoing market rental tension, benefiting incumbent REIT landlords.

According to JLL forecasts, across office, industrial, retail and other sectors, completions in 2026 will be lower than in the 2021–25 peak. Supply is tightening, not expanding. That’s good for GREIT earnings growth.

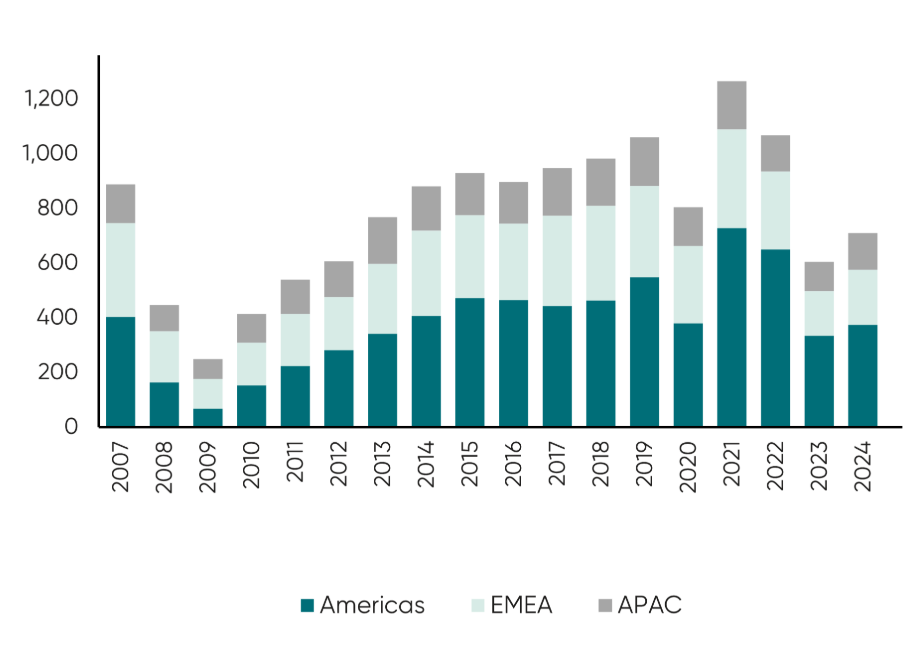

Fourth, private market transactions support valuations and prospective earnings growth. Private buyers, deploying real capital, tend to be more pragmatic than investors in listed markets. The recent increase in mergers and acquisition activity bolsters the investment case.

Figure 6: Direct commercial real estate transaction volumes ($bn)

Source: UBS/JLL

Fifth, inflation and interest rates are moving into more favourable territory. Historically, GREIT returns have been strongest when inflation is in a 2–3% band. Current running yields for global REIT portfolios are in the mid-single digits.

Let’s say that dividend yields contribute 3–5% and earnings grow at mid-single digits, too. Even if GREIT share prices stay exactly where they are, this would imply returns in the high single digits.

However, it’s quite possible the valuation discount closes over the next few years – we can’t say when exactly, but that’s usually what happens. Add these factors together and low-teens total returns are plausible, especially on a risk-adjusted basis.

For investors seeking a more defensive posture without sacrificing the potential for total returns, this is an ideal time. That’s why we believe global listed property looks less like a relic and more like a mispriced opportunity hiding in plain sight.

How best to access the opportunity?

It would be opportune, at this point, to raise a vested interest. As an active GREIT funds manager, we would naturally make the case for active management. Nevertheless, the facts speak for themselves, this is an active manager’s market.

1. Dispersion creates opportunity

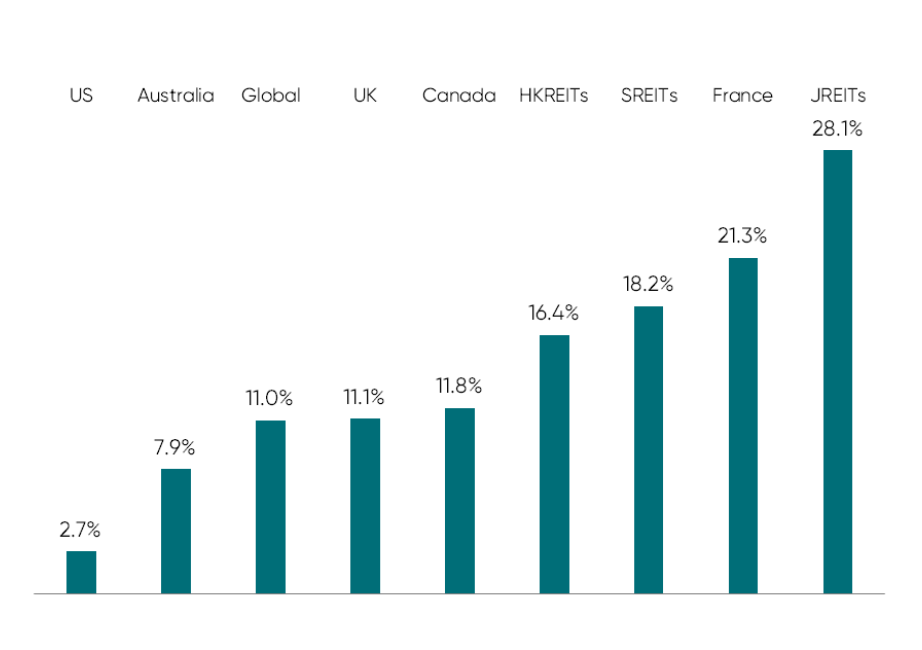

In 2025, performance dispersion, the spread of investment returns from their average across global REITs was unusually wide.

Country returns ranged from low single digits to more than 25%. Sub-sector outcomes spanned from negative mid-single digits (residential) to almost 30% (healthcare).

Figure 7: Country performance CY2025

Source: DXAM, UBS

This is not typical of a market moving in lockstep on macro factors. Instead, it reveals significant differences in Global REIT portfolios and their respective balance sheet strength and management quality. Index returns hide a good part of this story. The average is rarely the most attractive part of the market.

These are not circumstances in which index funds do well because selection is critical to performance. Active managers are forward-looking; index funds are built on a view of the past. In performance terms, that contrast is usually most evident when the cycle turns. We believe we have reached such a point.

2. The limits of Index investing

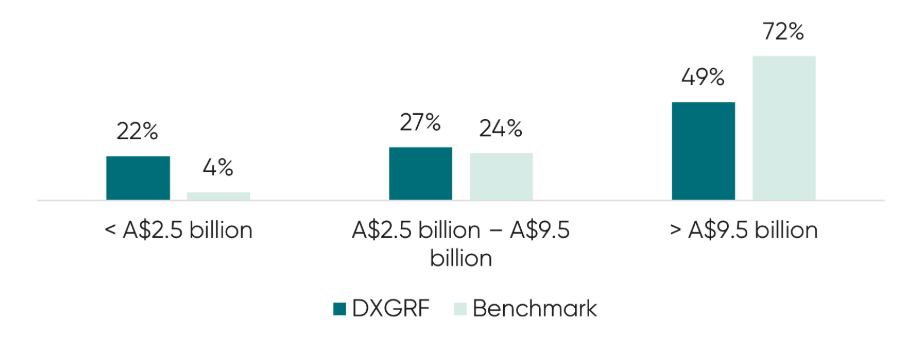

It is a mathematical inevitability that global REIT indices are biased towards large-capitalisation stocks. The chart below makes this case. About 72% per cent of the benchmark’s weighted average is in companies with market capitalisations of over A$9.5 billion.

Figure 8: Weighted average market cap (AUD)

Source: FactSet, DXAM

These are the most researched and widely owned securities in the sector. They also tend to be held across multiple passive vehicles and large institutional mandates. While this concentration can dampen mispricing, it can work the other way, too. Balance sheet weaknesses or structural challenges can be embedded in index exposures at precisely the wrong point in the cycle.

As the chart shows, the Dexus Global REIT Fund has significantly higher exposure to small and mid-capitalisation stocks that are under-represented in indices and under-covered by research houses. This is where valuation anomalies are more likely to arise. Indeed, this is where we are finding the best opportunities.

3. Capital preservation focus boosts total returns

Our Fund’s objective explicitly emphasises lower volatility, steady income and capital preservation alongside total returns. Capital growth is an important but secondary consideration.

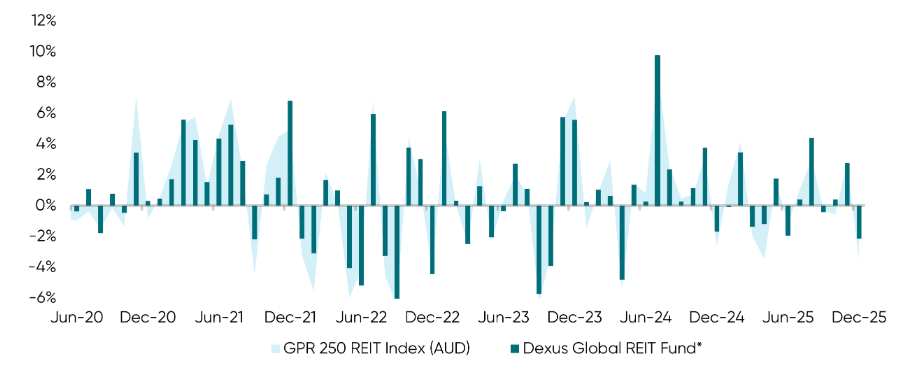

The latter, however, works in concert with the former. In 74% of down markets since inception, the Fund has outperformed the benchmark. This isn’t relevant just to income-focused and risk-averse investors. Avoiding permanent capital impairment during weaker periods compounds over time and boosts performance.

Figure 9: Periodic Fund vs GPR 250 REIT Net Index*

Source: DXAM as at 31 December 2025

*Past performance is not a reliable indicator of future performance. Returns after all fees and expenses. Assumes distributions are reinvested. Investors’ tax rates are not taken into account when calculating returns. Returns and values may rise and fall from the one period to another. Fund’s inception date used to determine the return: 1 April 2020. Dexus Global REIT Fund performance Index/Benchmark is the FPR 250 REIT Index (AU).

Our current positioning, for example, reflects a willingness to be underweight in areas where expectations appear elevated and overweight in segments where supply constraints and demographic trends are working in our favour. This allows us to target low teens total returns over the coming years whilst maintaining our mandated concentration on capital preservation.

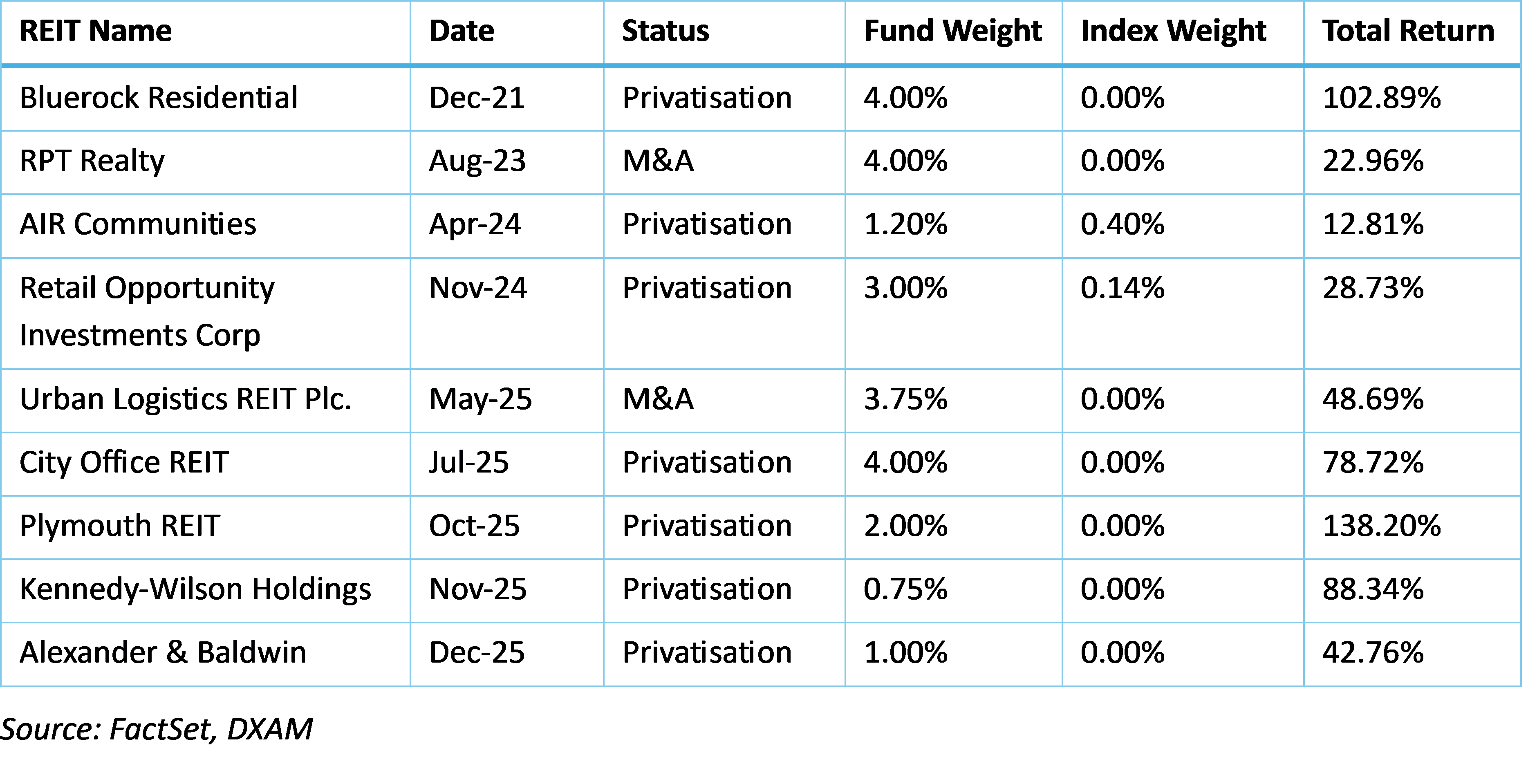

4. Direct markets are validating value

Direct commercial real estate transaction volumes are improving along with private capital fundraising and debt issuance, as we noted earlier. But, as the table below shows, there has also been a steady stream of value affirming, take-private transactions and corporate activity in listed property.

These aren’t theoretical valuation exercises. Private buyers, with long-term capital and detailed asset knowledge, are willing to pay more than the value public markets have ascribed to these assets.

Index funds capture such outcomes only in proportion to their index weights. Active managers can capture them more fully and are positioned to do so.

5. Historic discount offers a great opportunity

Global REITs have underperformed global equities for four consecutive calendar years, a record stretch over more than three decades of data. Relative to equities, the sector now trades significantly below historical averages.

In this environment, passive index funds ensure investors own the market’s aggregate exposure, warts and all. Active management helps concentrate investor capital on companies with defensible cash flows, prudent leverage and exposure to sectors with constrained supply. It also allows the purchase of those GREITs offering the biggest valuation discounts.

The return profile

The best opportunities in global listed property often don’t exist or aren’t material among index ETFs. Dispersion across countries, sectors and individual securities is high. Direct market transactions are validating private values above listed prices while balance sheet strength and asset quality differ markedly.

For investors seeking increased property exposure, with an emphasis on income and capital preservation, this is not a time to own the average. It is a time to be selective.

David Kruth is Portfolio Manager of the Dexus Global REIT Fund. Dexus is a sponsor of Firstlinks.