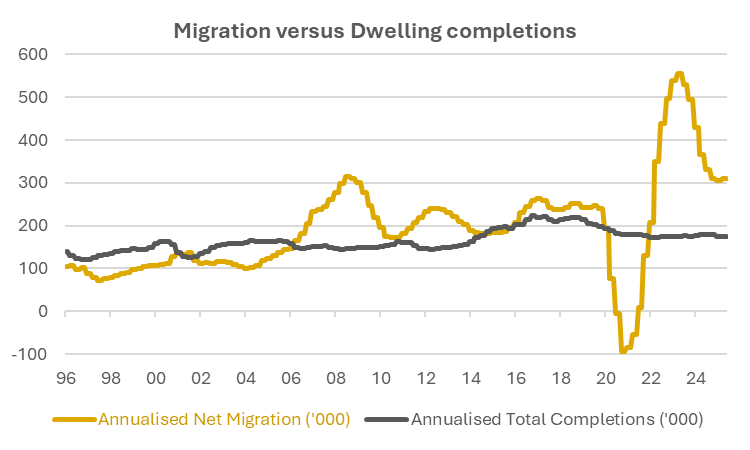

Rent is the defining issue of Australia's cost of living crisis. It has risen nearly 40% since 2020 and is consuming a record share of household income. The root cause of the rental crisis is the gap between the number of people who need housing and the number of dwellings being built to house them. The chart below shows an uncomfortable truth: annualised net overseas migration against total dwelling completions from 1996 to the present.

Source: FactSet, Vertium

Despite net migration coming off its record breaking 2022-23 peak, it is still running at an elevated level around 311,000 per year. Total dwelling completions are running at approximately 175,000, slightly below pre-COVID levels. The gap between demand and supply represents the structural shortfall that is driving rental inflation. Net migration and dwelling completions capture the core drivers of rental supply and demand. Adjusting for other factors such as household formation rates, the proportion of completions available for rent, or changes in existing rental stock would refine the analysis but not change the broad conclusion.

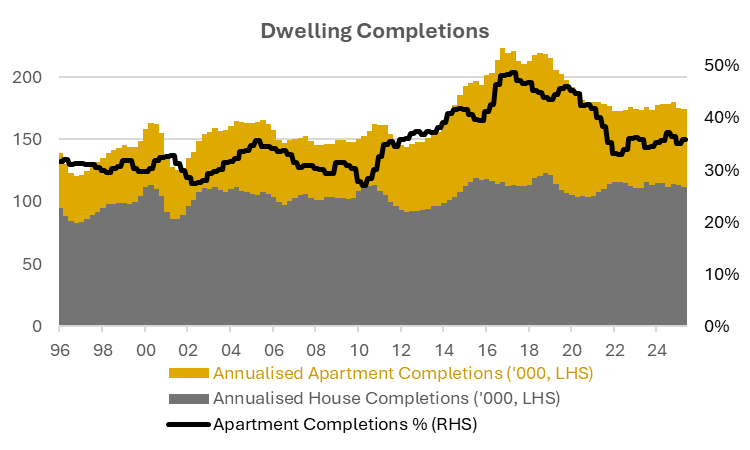

Over three decades, total dwelling completions have moved within a relatively narrow band, averaging about 165,000 per year. This stability is driven by house completions, which have been anchored at around 105,000 throughout. Apartment completions are more volatile — surging from around 30% of total completions prior to 2010 to nearly 50% at the 2017 peak before settling back to around 35%. But because they represent the smaller share of total completions, their volatility is dampened at the aggregate level.

Source: FactSet, Vertium

The simple economics of rent

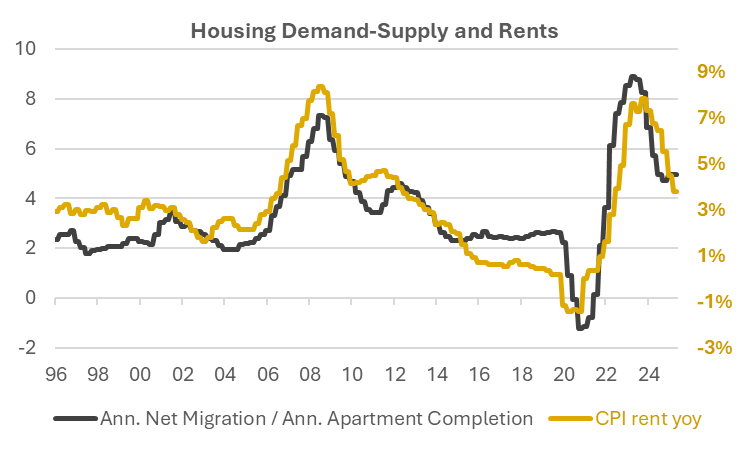

While apartments represent the smaller share of completions, they matter because they deliver supply at a volume detached housing cannot match. A single high-rise approval can yield hundreds of dwellings on a hectare of land where detached housing yields around fifteen. When the apartment pipeline runs at capacity, rental supply grows fast enough to absorb population growth and rents ease. When it stalls, nothing else compensates for the volume lost. Apartments are the release valve — and investor presale demand is the mechanism that opens it. The chart below plots the ratio of net overseas migration to apartment completions against CPI rent growth from 1997 to the present. The relationship between the two is unmistakable.

Source: FactSet, Vertium

Two rent booms

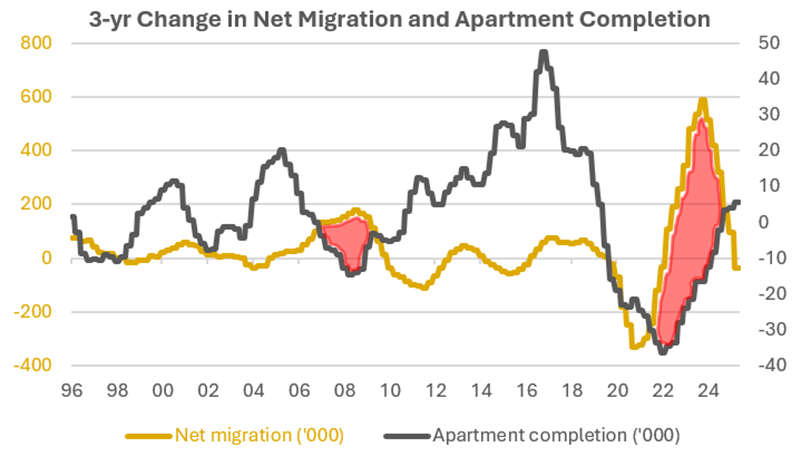

Australia has experienced two distinct episodes of severe rental inflation, one before the 2008 Global Financial Crisis (GFC) and one after the 2020 COVID pandemic. The underlying drivers were virtually identical: strong net overseas migration landing in a market where dwelling completions could not keep pace. The following chart shows the 3-year change in annual net migration and apartment completions to highlight the gap between demand and supply.

Source: FactSet, Vertium

In the pre-GFC episode, Australia's resources boom led to net overseas migration accelerating sharply, lifting net migration from 2006, while multi-dwelling completions experienced a decline. The migration-to-completions ratio rose sharply, and CPI rents surged. Rents eventually stabilised as migration fell in the aftermath of the resources bust. Lower rates used to stimulate the economy during the GFC also encouraged housing supply, which gradually rebalanced the housing market and further eased rent growth.

The post-COVID episode followed the same script, only more severely. Net overseas migration surged, eclipsing the migration dip during the lockdowns. This demand landed in a rental market where the supply pipeline had been hollowing out for years, compounded by post-COVID supply chain problems that extended construction timelines.

Despite comparable peak CPI rent growth of around 8% for both episodes, the post-COVID episode has felt far worse for renters. In the mid-2000s, the resources boom delivered strong economic growth and wages broadly kept pace with rising rents. After COVID, the picture reversed. Lacklustre economic growth and weak productivity left wages struggling, while inflation pushed workers into higher tax brackets. Bracket creep is eroding after-tax purchasing power. Full-time workers are now paying an average of 20% of their income in tax, the highest in over two decades. The result is that renters facing a 40% surge in rents since 2020 have done so with after-tax incomes that have barely moved in real terms. Australian households are now dedicating a record 33% of household income to rent, nearly double the 18% recorded in 2007-08. The rental crisis is not just a housing problem — it is the cost-of-living crisis.

Rent relief period

It was not always this way. Between these two rent booms sits an episode of genuine rental relief. Falling interest rates from 2012 fuelled strong capital gains expectations for housing, which in turn produced a boom in investor lending. The major banks — Commonwealth Bank, National Australia Bank, Westpac and ANZ Group — were the engine of this boom, growing their investor mortgage books aggressively as demand surged. By early 2017, interest-only loans represented 64% of all new investor lending. This capital funded a record apartment construction pipeline. Critically, this supply boom occurred despite the restrictive planning rules commentators today cite as the primary impediment to new supply. When investor lending economics were favourable, the market found a way.

The surge in apartment supply produced a prolonged period of subdued rent growth from 2016 to 2020. Completions surged while net migration was subdued and the ratio fell. CPI rent growth approached zero. For renters, it was genuine relief delivered entirely by private investor capital responding to market incentives.

While renters benefited from the excess supply, APRA grew concerned about the housing boom. Worried about systemic risk from concentrated interest-only lending, APRA imposed a cap in March 2017 limiting interest-only loans to no more than 30% of new residential mortgages. The major banks were forced to reprice interest-only loans higher and restrict approvals, directly curtailing the investor lending that had been driving apartment supply. Investor loan growth collapsed. The apartment presale market, which depends on investor buyers to unlock construction finance, dried up. The supply pipeline that had been delivering rental relief collapsed almost overnight. Fortunately, net migration remained stable and rents held steady.

The missing policy

The lesson from 30 years of data is clear: reducing rent inflation requires pulling two levers.

Lever one: reduce population growth

Immigration is one of Australia's great economic strengths. It brings skills, diversity and long-run productivity benefits. But like any good policy taken to an extreme, the costs eventually outweigh the benefits. Annual net migration running at 311,000 into a market completing 175,000 annual dwellings is not an immigration policy — it is a housing and cost of living crisis. Moderating migration to levels the housing stock can absorb reduces rental demand pressure directly and immediately. The international evidence is unambiguous. New Zealand, Canada and the United States all cut immigration materially in 2024-25, and in each case rental inflation decelerated sharply within months. Migration is the demand lever governments can pull immediately.

Lever two: incentivise investor lending for new builds

Investor credit conditions drove the 2013-2017 apartment supply boom. Unless the government plans to subsidise every dwelling itself, it needs to unleash the private sector. The new build negative gearing exemption creates the right incentive. For listed residential developers like Mirvac and Stockland, the exemption is a potential demand tailwind, but making it work requires credit conditions that allow investors to act on it. Today, those credit conditions are more restrictive than at any point during the 2013-2017 boom.

APRA should consider reducing the 3% serviceability buffer that was set for emergency interest rates in 2021. Now that the cash rate has normalised, the serviceability buffer is suppressing the investor borrowing capacity that drives apartment supply. More importantly, the single most effective policy lever to recreate the apartment supply boom is lower interest rates. But the RBA cannot cut rates in an environment where government spending is stoking demand. Every dollar of government spending that adds to inflation delays the rate cuts that would unlock investor lending for new builds and ease the rental crisis.

Yet the government's supply response largely bypasses the private sector. The National Housing Accord, announced in October 2022, targets 1.2 million new homes over five years, or 240,000 completions per year. The problem is that the absolute peak of the greatest investor lending boom in Australian history delivered only 223,000 completions in the year to March 2017. The reason the target will likely be missed is simple: the Accord offers very little incentive to the private market that drives apartment supply. Its spending is overwhelmingly directed at social and affordable housing. The Accord contains no mechanism that replicates the credit conditions which produced the only episode of genuine rental relief.

Conclusion

The supply-demand framework is not complicated. Rents rise when migration outpaces housing supply and fall when supply catches up. History has demonstrated this in Australia and the international evidence confirms it is not unique to this country.

What is complicated is the political will to pull the levers that work. Moderating migration, recreating the credit conditions that built the last apartment boom, and resisting fiscal spending that keeps inflation elevated and delays rate cuts that would unlock private sector construction — these are the levers that move rents. Until those levers are pulled, the negative gearing reform will have little impact and Australia's cost of living crisis will remain unresolved for the third of Australians who rent.

Jason Teh is the founder and Chief Investment Officer of Vertium Asset Management; and a Portfolio Manager at Clime Investment Management Limited, a sponsor of Firstlinks. This article is general in nature and does not constitute or convey personal financial advice. It has been prepared without consideration of anyone’s financial situation, needs, or financial objectives. Before acting on the areas discussed and contained herein, you should consider whether it is appropriate for you and whether you need to seek professional advice.

For more articles and papers from Clime, click here.