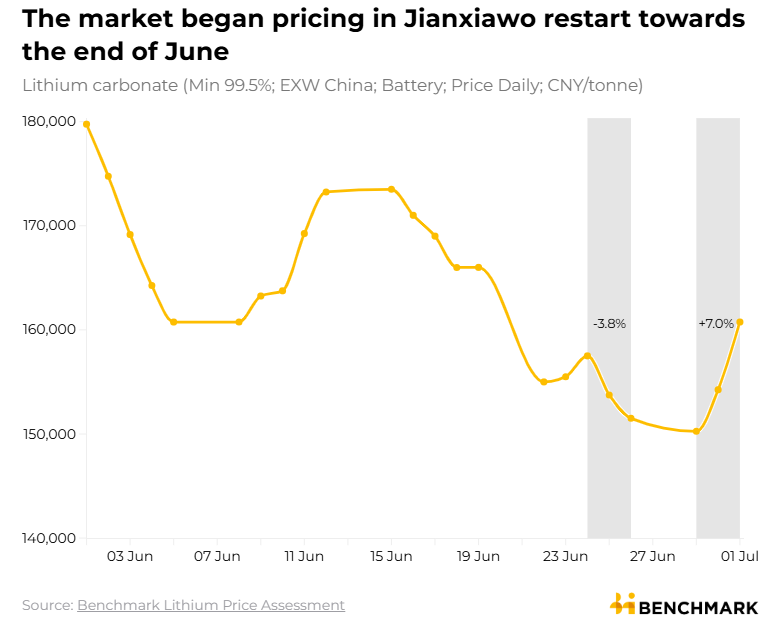

Lithium carbonate fell roughly 20% in June – in another bout of volatility that has come to define the battery metal.

Its decline has dragged down ASX lithium producers such as Pilbara Minerals and IGO and acted as a headwind to the ASX, which has become increasingly reliant on the resources sector for earnings growth.

The latest slump was driven by three things: mine restarts in China and Australia; demand concerns for electric cars following the re-opening of Hormuz; and renewed discussion about sodium-ion batteries.

It also highlights the central contradiction of lithium: while it is the most volatile major commodity by far, its demand growth is also the most certain.

Lithium’s drop: CATL and the power of rumours

The main driver of lithium's recent slide has been the restart of Contemporary Amperex Technology Co. Limited's (CATL) giant Jianxiawo mine.

Jianxiawo is one of the world's largest lithium mines and can produce around 6% of global supply. It was shut down in August 2025 on environmental concerns.

The closure sent lithium prices soaring. Lithium carbonate more than doubled in the months that followed, not simply because supply disappeared, but because it was CATL specifically that disappeared.

CATL is both the world's largest battery manufacturer and one of its largest lithium producers. Unlike pure-play miners, it sits on both sides of the trade. Lower lithium prices hurt its mining operations, but they benefit its much larger battery business.

That makes CATL different from most producers, which typically prefer a "value over volume" approach: producing enough material to earn attractive returns, but not so much that the market becomes oversupplied.

In many respects, the past year has been a case of "CATL giveth, CATL taketh away".

Sell the rumour, buy the fact

CATL's ructions have proved a profitable vein for traders and a reminder of how difficult commodity markets are to time.

In mid-June, Chinese authorities conducted what appeared to be a routine site assessment at Jianxiawo. The visit contained no material information, yet it sparked accurate rumours that production would resume. Lithium futures promptly fell nearly 10%.

Then, when the restart was formally announced on 29 June, lithium futures rallied 8.4%.

It was a classic commodity market reaction. The rumour mattered more than the announcement itself.

But it would be unfair to blame lithium's latest weakness entirely on China.

Australian producers have also been dialling up supply. The restart of mines such as Bald Hill has reinforced expectations that additional tonnes are coming. Buyers do not need to chase material when they know more supply is on the way.

Demand worries have compounded the sell-off

Demand concerns have also weighed on sentiment.

Oil prices fell around 40% between March and late June as the US-Iran ceasefire unwound the geopolitical risk premium. Lower oil prices reduce the economic incentive to switch to electric vehicles.

At the same time, investors have become more cautious on battery energy storage, one of lithium's fastest-growing sources of demand. China has begun reducing tax rebates on battery exports, raising concerns that some of the recent surge in energy storage demand may have been pulled forward.

That helps explain why lithium forwards have sold off alongside spot prices.

The sodium-ion story is probably overdone

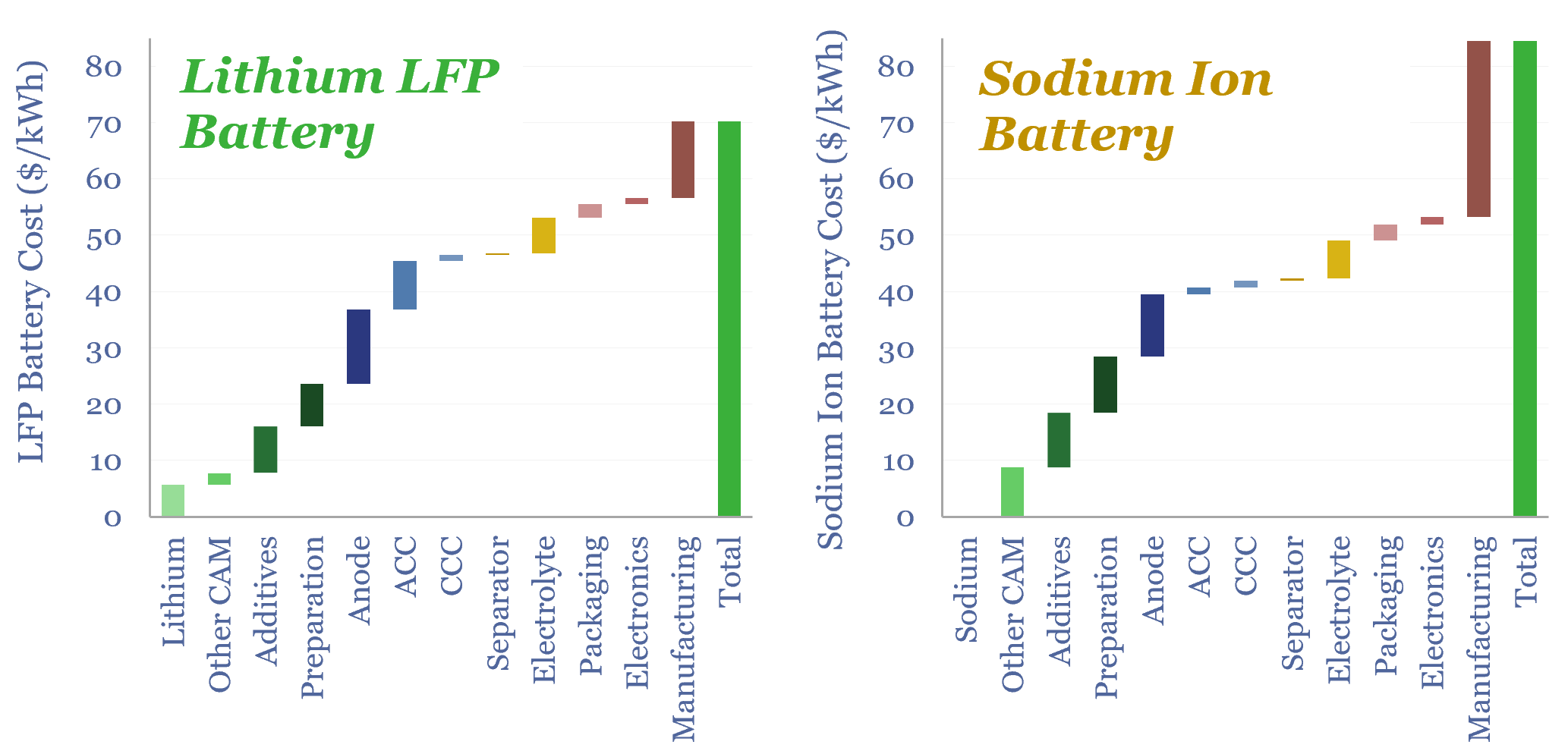

The final piece of the puzzle has been renewed talk of sodium-ion batteries replacing lithium-ion batteries.

Source: Thunder Said Energy, June 11, 2026

Sodium batteries have been discussed as an alternative to lithium for decades, with such discussion rising and falling with the lithium price. Sodium is abundant, more environmentally friendly, and CATL recently announced that it expects to deploy sodium-ion batteries in more than 10,000 vehicles this year.

Some investors have interpreted that as evidence that lithium demand is about to be disrupted.

But that conclusion is premature at best.

Sodium-ion batteries remain less energy dense than lithium-ion batteries and therefore tend to be heavier and bulkier for the same amount of stored electricity. While engineering improvements may narrow the gap, the underlying chemistry means sodium is unlikely to displace lithium in most electric vehicles.

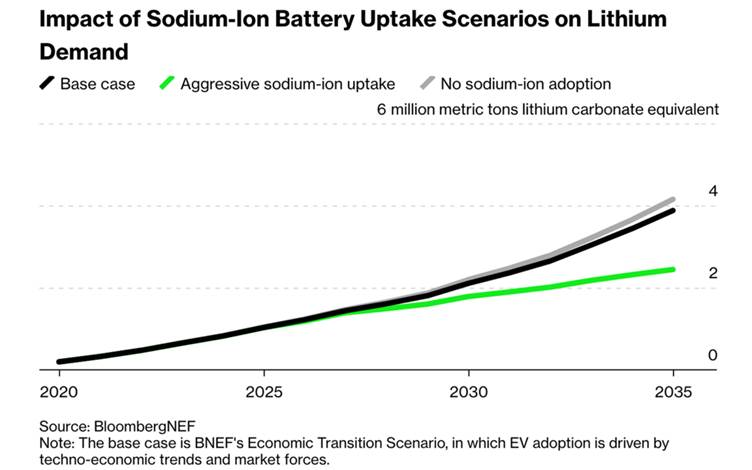

Instead, sodium batteries are more likely to find niches where weight and size matter less, such as AI data centres. Forecasts from reputable and impartial sources – such as the IEA and BloombergNEF – anticipate sodium subtracting only marginally from long-term lithium demand.

What it means for ASX investors

Tying this all together, lithium remains an extraordinarily volatile commodity.

That volatility does not simply reflect bad news. It also reflects the good news that producers continue to restart mines and bring on additional supply because they expect demand to keep growing.

Historically, Australian producers sold much of their lithium on long-term contracts, giving them some insulation when prices fell. Today, many sell material at prices much more closely linked to spot spodumene.

As a result, their share prices – particularly Pilbara Minerals – increasingly offer geared exposure to movements in the spodumene price. This creates an often-uncomfortable ride for shareholders.

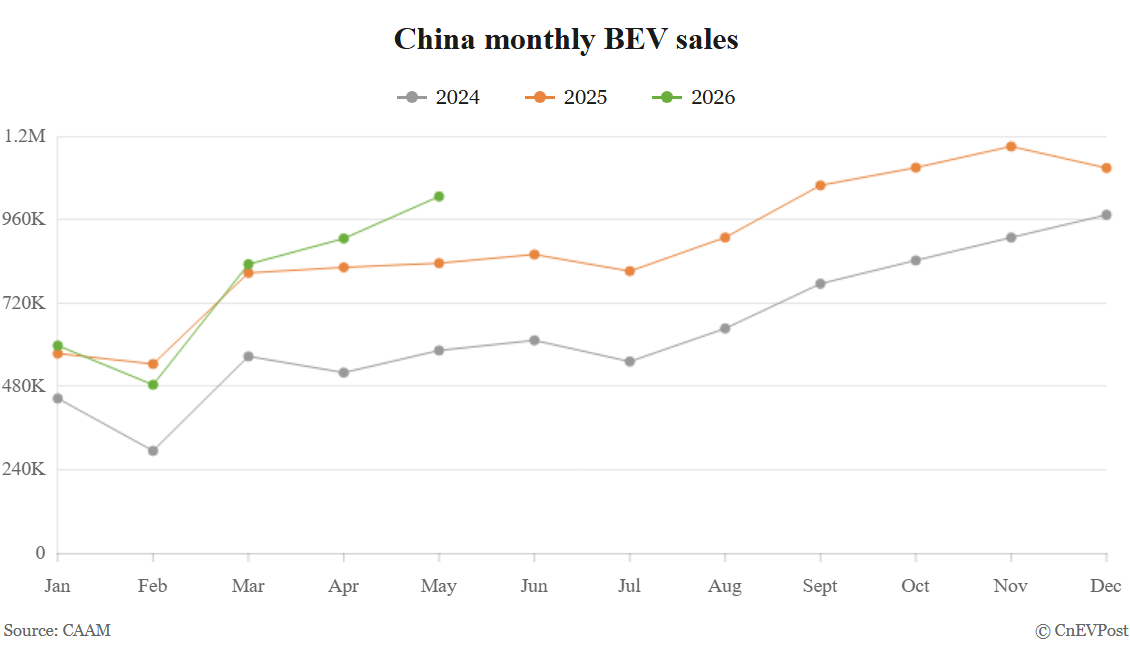

China monthly BEV sales, May 2026. Source: CNEVPOST, 10 June 2026

The irony is that while lithium is the most volatile commodity, its long-term demand growth looks the most certain.

Global electric vehicle sales are expected to exceed 23 million units this year. In concrete terms, that means every single person in Australia – including children – buying an electric car every year. That’s up from around 17 million in 2024. Battery energy storage installations are also forecast to grow by more than 30% in 2026. Then there are other categories too, such as drones, humanoid robotics and shipping. Most industry forecasts still see global lithium demand roughly doubling by the end of the decade.

The near term may remain challenging as supply returns. But many long-term forecasts continue to point to deficits emerging later this decade unless higher prices incentivise a new wave of investment.

That tension, between unrivalled demand growth and boom-bust supply growth, is the defining feature of lithium investing.

In this setting, we believe a global and diversified approach is preferable to trying to pick winners on the ASX.

The ASX hosts more lithium companies than any other global exchange, which means Australians have plenty to choose from. They’re also often familiar with the companies, which creates a sense of comfort in buying their shares.

The problem, though, is that ASX lithium producers are overwhelmingly exposed to hard-rock spodumene, which is most cost-advantaged for lithium hydroxide and premium electric cars. Global lithium miners provide access to a much broader opportunity set, including lower-cost South American brines, integrated chemical producers in China and emerging technologies such as direct lithium extraction, which could eventually unlock vast resources in Argentina, the United States and elsewhere.

Diversification cannot eliminate lithium's volatility. But it can reduce the risk of being overly exposed to a single geography, production method or end market.

ETF Shares provides the ETFS Global Lithium Miners ETF (ASX: VOLT) which began trading on the ASX in April 2026. For more information click here.

David Tuckwell is the Chief Investment Officer at ETF Shares, a sponsor of Firstlinks. He is also a journalist and researcher specialising in finance and international politics. The information provided in this article is general in nature. Before acting on any information in this article, you should consider the appropriateness of the information having regards to your objectives, financial situation or needs and consider seeking independent financial, legal, tax and other relevant advice. Past performance is no guarantee of future performance.

Disclaimer: This article is issued by ETF Shares Management Limited (“ETF Shares”) (ABN 77 680 639 963, AFSL: 562766) and ETF Shares is solely responsible for its issue. Under no circumstances is this article to be used or considered as an offer to sell, or a solicitation of an offer to buy, any securities, investments or other financial instruments. Offers of interests in any retail product will only be made in, or accompanied by, a Product Disclosure Statement (PDS) and target market determination (TMD) available at www.etfshares.com.au.