Today’s lithium rally has the look and feel of the tech stock rally in the early-2010s.

In those years, Amazon, Google and Netflix had proven business models and were household names. Their stocks were rising but no-one fully trusted it given the experience of the dotcom crash 10 years earlier.

Lithium today is rallying as major investment banks forecast sustained deficits. Demand for lithium is forecast by some industry figures to double between now 2030. Adding to potential demand are up-and-coming technologies like humanoid robotics and solid-state batteries, which are lithium intensive. Despite the strong demand picture, no new lithium projects have been launched since 2024, curtailments are everywhere and feasibility studies have greatly stagnated.

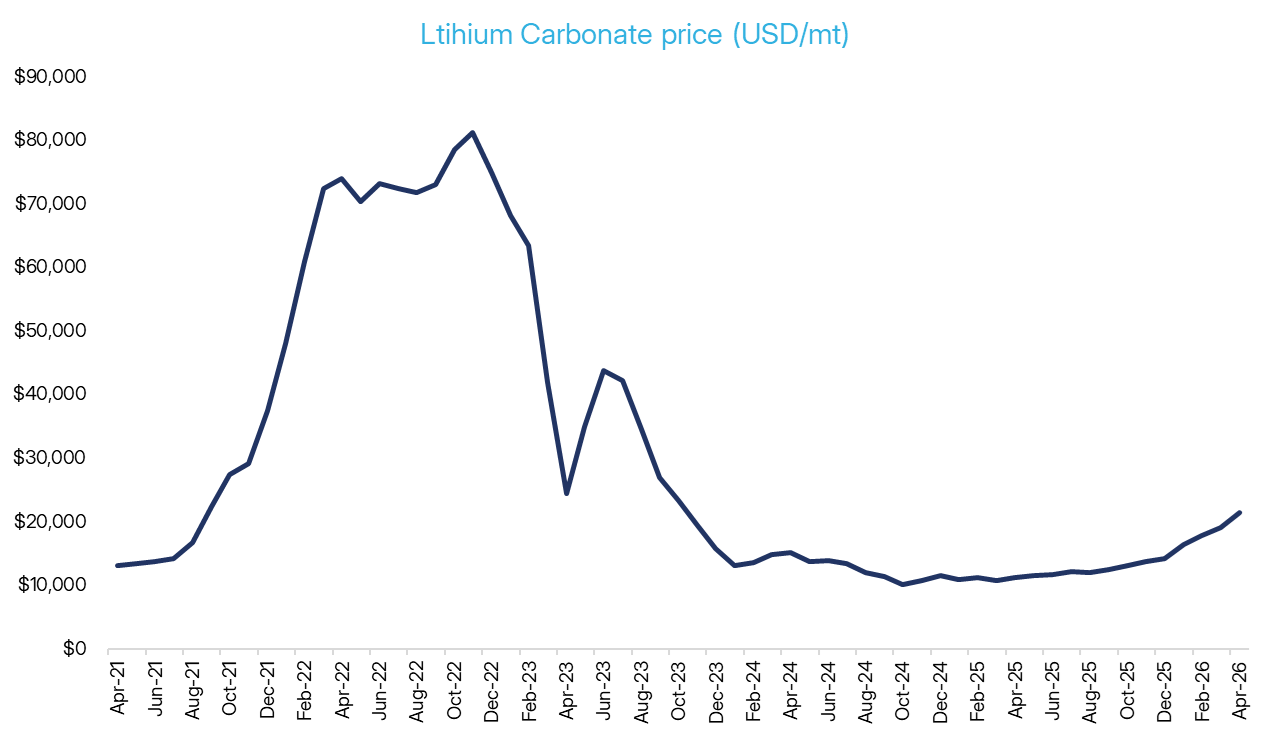

We believe that lithium remains out of favour due to the experience of 2022, when carbonate prices crashed 80%. Given this, it’s worth unpacking why this time is genuinely different.

Lithium demand is forecast to double within three years

The guts of lithium demand come from electric cars, which are continuing their steady surge. Because Australians focus primarily on Australian and US car sales, they often miss the global picture.

Electric vehicles accounted for roughly one in four new cars sold worldwide in 2025. In China, they outsell combustion-engine cars. In Europe, sales grew 33% last year, faster than in China. And European vehicles tend to have larger batteries, requiring more lithium.

Industrial batteries for energy storage – increasingly linked to AI-driven power demand – have emerged as a major new demand category and are growing faster than EV batteries.

Data centres require enormous amounts of reliable power. That helped drive energy-storage battery demand up 51% in 2025, outpacing the 26% growth in EV batteries. JPMorgan projects energy storage will represent 30% of global lithium demand in 2026, rising to 36% by 2030. This category of demand barely existed during the 2022 bubble and is a major differentiator in today’s rally.

Albemarle, the world’s largest lithium producer, confirmed the scale of this shift in its February 2026 results. Global lithium demand reached 1.6 million tonnes of lithium carbonate equivalent in 2025, a 30% year-on-year increase. For 2026, Albemarle projects demand of between 1.8 and 2.2 million tonnes, and by 2030 it forecasts demand of 3.7 million tonnes annually – a doubling, in other words. SQM, the second-largest producer, has published broadly similar forecasts, with demand roughly doubling between 2025 and 2030 on its numbers as well.

Supply isn’t ramping the way it did in 2022

Supply is not ramping up the way it did in 2022.

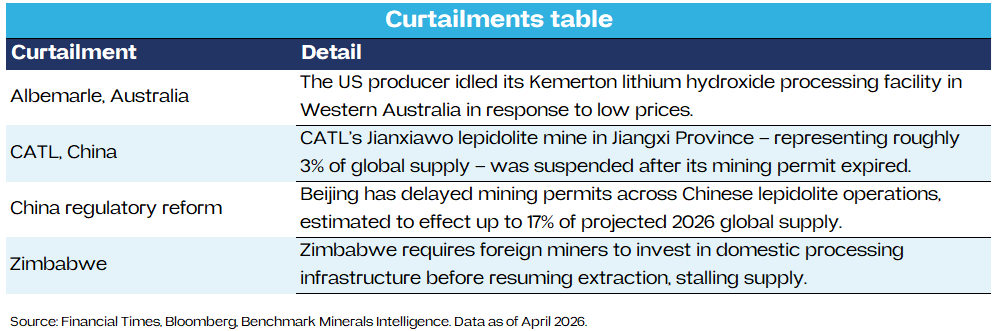

After the bubble burst, lithium prices remained below incentive levels for almost two years. Feasibility studies for new lithium projects fell from more than 30% annually to fewer than ten in 2025. No major new projects have commenced since 2024. Compounding the problem has been a wave of production curtailments, reflected in the table below.

Miners that survived the downturn are in no hurry to flood the market. They have adopted a ‘value over volume’ philosophy similar to what has occurred in uranium recently with Kazatomprom. Even if prices rise above incentive levels, supply responses are likely to remain slow.

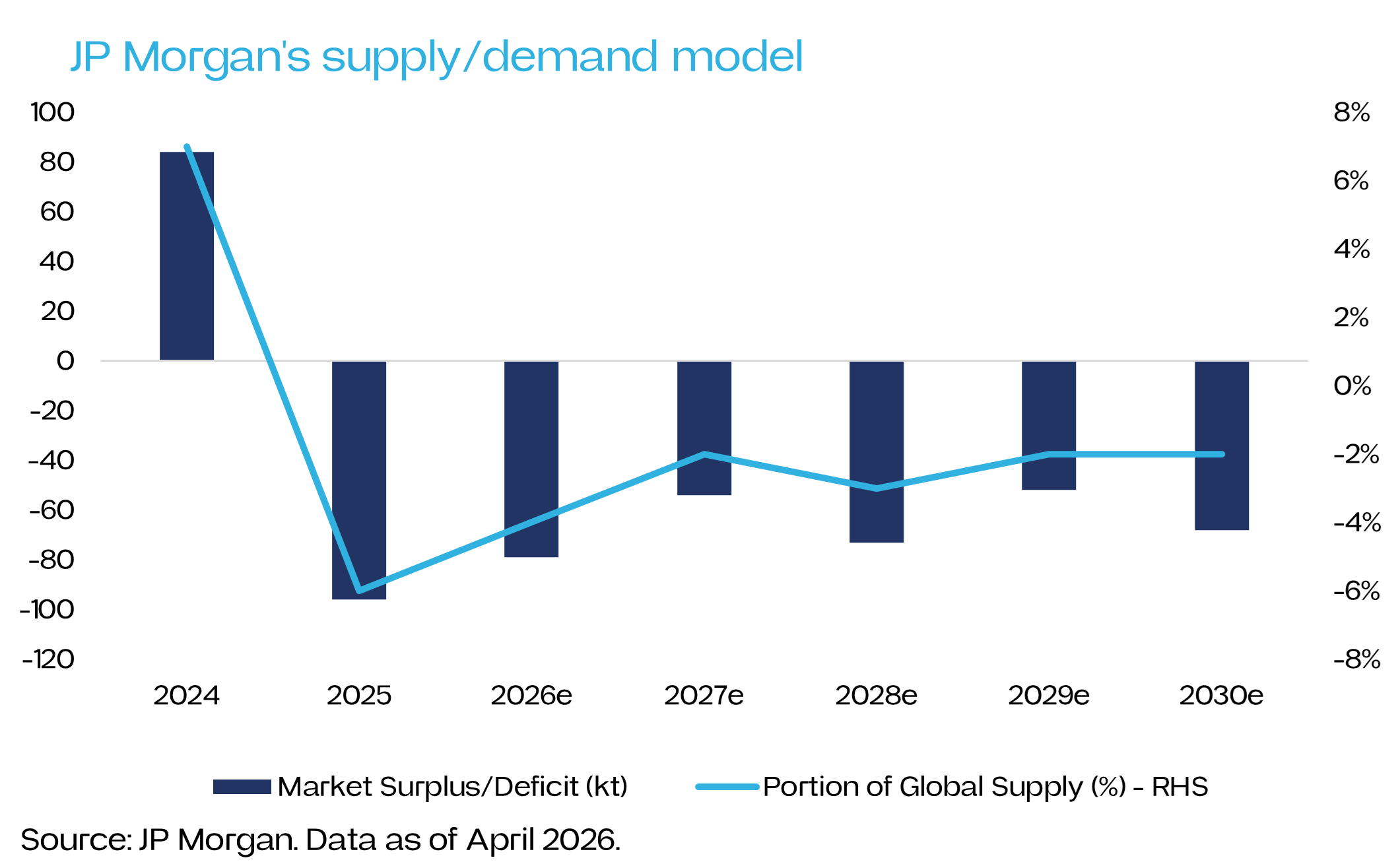

JP Morgan now forecasts a lithium market deficit persisting through 2030, even under conservative assumptions. Morgan Stanley projects a deficit of 80,000 tonnes of lithium carbonate equivalent in 2026 alone. UBS, while more conservative, still estimates a 22,000-tonne shortfall. Forecasts differ in magnitude, not direction. The broad consensus among major banks is that the era of chronic oversupply is over.

Lithium has optionality on future tech

Future tech like humanoid robotics, solid-state batteries, wearable computing and electrified aviation could also greatly benefit lithium. While these are widely understood by engineers and technologists to be ‘on their way’, most broker models still do not incorporate these demand sources.

Humanoid robotics may ultimately prove the most significant. Morgan Stanley has estimated that each humanoid robot could require around two kilograms of lithium. If its projection of more than one billion robots by 2050 proves even partially correct, incremental lithium demand by 2040 alone could push the market into a deficit approaching 80% of current supply. Morgan Stanley analysts have described lithium as an “Achilles’ heel” of the humanoid robotics buildout.

Solid-state batteries are the second major wildcard. They are more lithium-intensive because they use lithium anodes instead of graphite ones. Commercial production is beginning to scale as technological breakthroughs accumulate. The consensus within the automotive industry increasingly appears to be that it is a question of when, not if, solid-state batteries become mainstream.

Lithium: how to invest?

For investors interested in lithium, the natural question becomes how to gain exposure. The most obvious approach is to buy ASX-listed lithium miners such as Pilbara, Liontown or IGO.

The challenge is that Australian lithium miners are narrow businesses and only mine spodumene (hard rock). This is a problem because spodumene is at risk of long-term disruption from cheaper and more environmentally friendly direct lithium extraction. This is where lithium is taken directly from brine without an evaporating pond. Aussie spodumene miners do not do refining either, unlike their Chinese counterparts Ganfeng and Tianqi. This too is a problem because refining can be higher margin.

A more balanced approach, in our view, is to diversify globally across lithium producers rather than trying to pick individual ASX lithium stocks. This allows investors to be more agnostic about the lithium extraction techniques, tap into higher margin refining, and avoid the risks that can come with betting on a single company.

Conclusion

Many investors burned by the dotcom crash in 2000 avoided technology stocks for years afterwards and missed one of the greatest equity rallies.

Something similar could be true for lithium. The energy transition is continuing. AI is accelerating global power infrastructure investment. Robotics is emerging as a genuine industrial category. And lithium continues connecting all these themes.

Whether the current opportunity persists will depend on how quickly supply responds and whether demand forecasts are realised.

ETF Shares provides the ETFS Global Lithium Miners ETF (ASX: VOLT) which began trading on the ASX in April 2026. For more information click here.

David Tuckwell is the Chief Investment Officer at ETF Shares, a sponsor of Firstlinks. He is also a journalist and researcher specialising in finance and international politics. The information provided in this article is general in nature. Before acting on any information in this article, you should consider the appropriateness of the of the information having regards to your objectives, financial situation or needs and consider seeking independent financial, legal, tax and other relevant advice. Past performance is no guarantee of future performance.

Disclaimer: This article is issued by ETF Shares Management Limited (“ETF Shares”) (ABN 77 680 639 963, AFSL: 562766) and ETF Shares is solely responsible for its issue. Under no circumstances is this article to be used or considered as an offer to sell, or a solicitation of an offer to buy, any securities, investments or other financial instruments. Offers of interests in any retail product will only be made in, or accompanied by, a Product Disclosure Statement (PDS) and target market determination (TMD) available at www.etfshares.com.au.