“Design a portfolio you are not likely to trade… akin to premarital counselling advice; try to build a portfolio that you can live with for a long, long time.” Robert Arnott, Research Affiliates

The financial industry has long projected an image of delivering superior returns through complex strategies. And this certainly might be the case for a small portion of institutions on a short-term basis. But there is a struggle to consistently deliver alpha. Notably, professional money managers operate in a very different environment to retail investors.

Despite this, I find the portrayal of superiority has worked quite well and forms part of why some retail investors are drawn to sophisticated investment options.

How we got here

Sophistication has long been a status symbol.

It has developed well beyond the social markers of luxury goods and prestigious education to now deeply embed itself in the investment industry.

Retail bias for complexity stems from the assumption that intricate structures are inherently superior to simpler ones. We can fall into this trap by layering portfolios with additional products, strategies or structures, convinced that it will lead to better outcomes. This pertains not only to overly layered portfolios, but also an uptick in interest for complex products, once reserved for the likes of institutions.

The intellectual foundation of the 60/40 portfolio can be traced back to Modern Portfolio Theory (MPT), developed by Harry Markowitz in the 1950s. Thus, the birth of ‘the efficient frontier’ - the concept of optimising returns for a given level of risk through diversification.

For decades, the 60/40 model was a gold standard for a balanced allocation, however in recent decades, the landscape has shifted. Inspired by the success of David Swensen and the Yale Endowment Fund, the industry has shifted to embrace a more complex construction approach, while questioning the adequacy of the traditional 60/40 mix. Many retail investors have followed suit.

The democratisation of access to alternative investments have seen allocations shift toward hedge funds, private equity, infrastructure and private credit to increase returns and reduce correlation with public markets. Consequently, the average investor’s toolkit is much broader now and contains a wider array of asset classes.

But this hasn’t been without trade-offs, and it raises a few important questions that inevitably complicate things for retail investors. Chief among them is our ability to assess liquidity risk and valuation transparency in markets. Perhaps more importantly, does added complexity actually translate to better outcomes?

The confounding bias for investment complexity

Simplicity can be hard to appreciate and even harder to achieve in an industry focused on the proliferation of new products.

Research Affiliates released an article almost a decade ago on this issue. The authors asserted that investors have a profound bias toward complexity. They attribute this to two drivers: the incentive for asset managers to justify higher fees by leaning into complex strategies, and investor perceptions of intricate market dynamics demanding investment complexity. The paper raises a crucial point that this behaviour encourages performance chasing that manifests in a whipsaw pattern of buying and selling at the wrong times.

The industry earns higher fees through selling sophistication. But not all of these promises materialise in the long term. The most recent Morningstar analysis from the US found that active fund strategies struggled mightily from July 2024 through June 2025, with just 33% of strategies surviving and beating their asset-weighted average passive counterparts. This marks a 14% drop from a year earlier but also reflects a wider pattern of long term active underperformance amongst the higher fee funds.

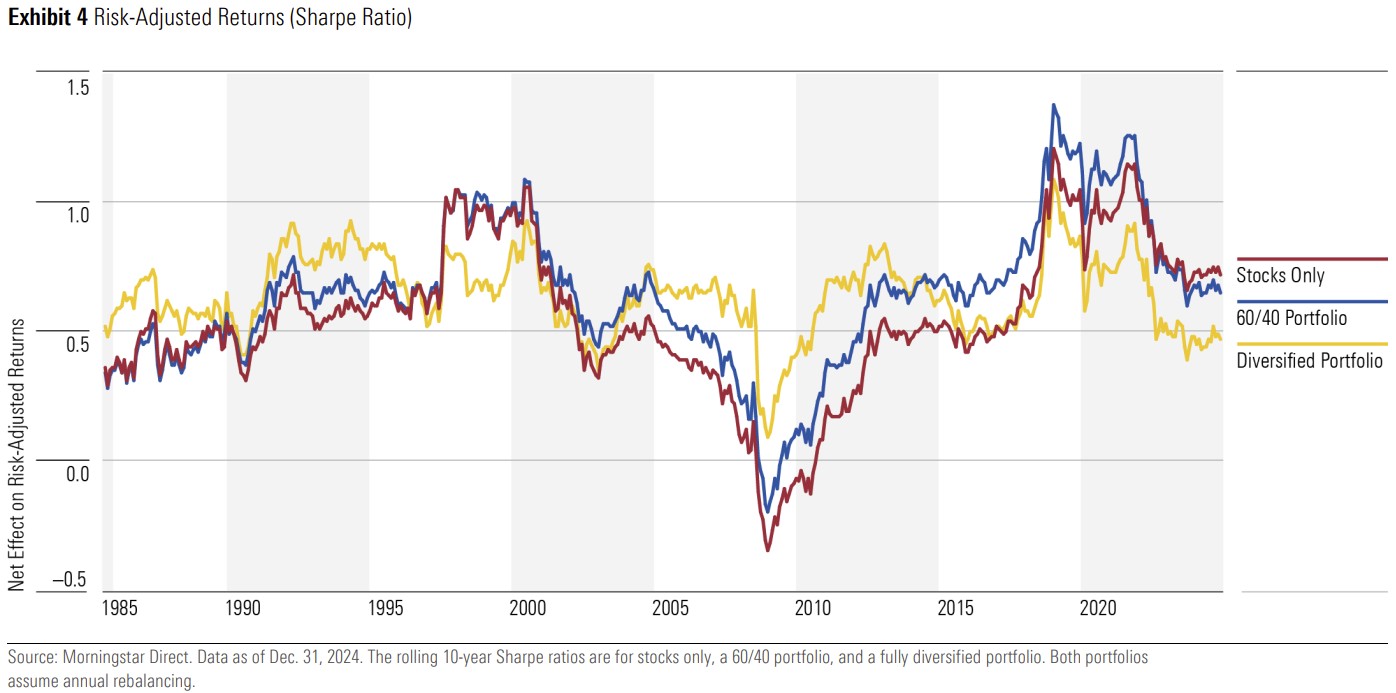

Another US-based study was conducted to test the value of diversification. This compared a portfolio comprised of 11 different asset classes, a plain-vanilla 60/40 portfolio and an all-stock portfolio over the long-term. The below graph demonstrates the findings of this exercise.

The diversified portfolio improved risk-adjusted returns (as measured by the Sharpe ratio) versus an all-stock portfolio during most rolling 10-year periods between January 1976 and August 2017. However, its relative performance has diminished in more recent years.

In contrast, the classic 60/40 has shown remarkable consistency. Since 1976, it has outperformed a stock-only approach about 83% of the time and since early 2005, it has come out ahead of the diversified portfolio in every rolling 10-year period.

We can all draw our own conclusions from this data, but it does make the case that simplicity has often been just as effective (if not more) than attempting to invest in every asset class under the sun.

Ultimately investing is a game of trade-offs. There will always be a portfolio that outperforms yours retrospectively. But that doesn’t mean it forms the gold standard approach for the future or for your specific goals. Staying grounded to your objectives and strategy is essential to avoid the temptation of overcomplicating your portfolio in pursuit of elusive outperformance.

A case in point

The allure of alternative asset classes has drawn investors into intricate products that some may struggle to fully grasp the mechanics of. This lack of understanding can have serious consequences.

A good example (albeit, before my time) is the 2008 collapse of Basis Capital, an Australian hedge fund whose strategy hinged on investing in complex instruments known as collateralised debt obligations (CDOs). At the time, these products were well rated, but critics have argued that the risks were largely misunderstood by the wider community.

When the market turned in the wake of the global subprime mortgage crisis, margins calls were made and Basis Capital was forced to sell off in a plummeting market. The fund was unable to recover and that consequently resulted in combined losses of $350 million.

One could argue the issue here wasn’t just the product itself, rather the broader ecosystem that failed to scrutinise products for their complexity and lacked an understanding of whether they were suitable for retail investors. Category ratings and performance metrics only go so far. Not every well-rated product belongs in a retail portfolio.

Managing complex financial products and overly layered holdings requires more time, effort and resources. This can create inefficiencies and result in a directionless portfolio with lower overall returns. On top of this, there are significant cost implications. Investing in complex products or even choosing to hold a large number of them result in higher fees and expenses. These naturally eat into your ability to compound returns over time.

Some sage advice

To conclude, I’d like to point you towards one of my favourite snips from Buffett’s 2016 Letter to Shareholders.

“Over the years, I’ve often been asked for investment advice, and in the process of answering I’ve learned a good deal about human behaviour. My regular recommendation has been a low-cost S&P 500 index fund. To their credit, my friends who possess only modest means have usually followed my suggestion.

I believe, however, that none of the mega-rich individuals, institutions or pension funds has followed that same advice when I’ve given it to them. Instead, these investors politely thank me for my thoughts and depart to listen to the siren song of a high-fee manager.

That professional, however, faces a problem. Can you imagine an investment manager telling clients, year after year, to keep adding to an index fund replicating the S&P 500? That would be career suicide. Large fees flow to these managers, however, if they recommend small managerial shifts every year or so. That advice is often delivered in esoteric gibberish that explains why fashionable investment “styles” or current economic trends make the shift appropriate.

The wealthy are accustomed to feeling that it is their lot in life to get the best food, schooling, entertainment, housing, plastic surgery, sports ticket, you name it. Their money, they feel, should buy them something superior compared to what the masses receive.

In many aspects of life, indeed, wealth does command top-grade products or services. For that reason, the financial “elites” – wealthy individuals, pension funds, college endowments and the like – have great trouble meekly signing up for a financial product or service that is available as well to people investing only a few thousand dollars. This reluctance of the rich normally prevails even though the product at issue is –on an expectancy basis – clearly the best choice. My calculation, admittedly very rough, is that the search by the elite for superior investment advice has caused it, in aggregate, to waste more than $100 billion over the past decade.

Human behaviour won’t change. Wealthy individuals, pension funds, endowments and the like will continue to feel they deserve something “extra” in investment advice. Those advisors who cleverly play to this expectation will get very rich. This year the magic potion may be hedge funds, next year something else. The likely result from this parade of promises is predicted in an adage: “When a person with money meets a person with experience, the one with experience ends up with the money and the one with money leaves with experience.”

A new era of product democratisation is truly upon us. Challenges have shifted from a lack of access to a lack of complete understanding. It’s important to acknowledge that the temptation to emulate institutional strategies should be grounded by a clear view of our role as retail investors and what we are trying to achieve in our lives.

Simonelle Mody is an Investment Specialist at Morningstar Australia. She writes for retail investors and financial advisers on topics spanning portfolio construction, market trends, ETFs and investor behaviour.