Oil at ~US$90-$100/bbl (barrel) represents a ~60% hike in prices from pre-conflict levels, with risks of higher prices omnipresent. Since the commencement of conflict, the ensuing closure of the Strait of Hormuz, damage to energy infrastructure in the region and resurgence in global geopolitical uncertainty are conditions to truly test the mettle of any asset class, including infrastructure.

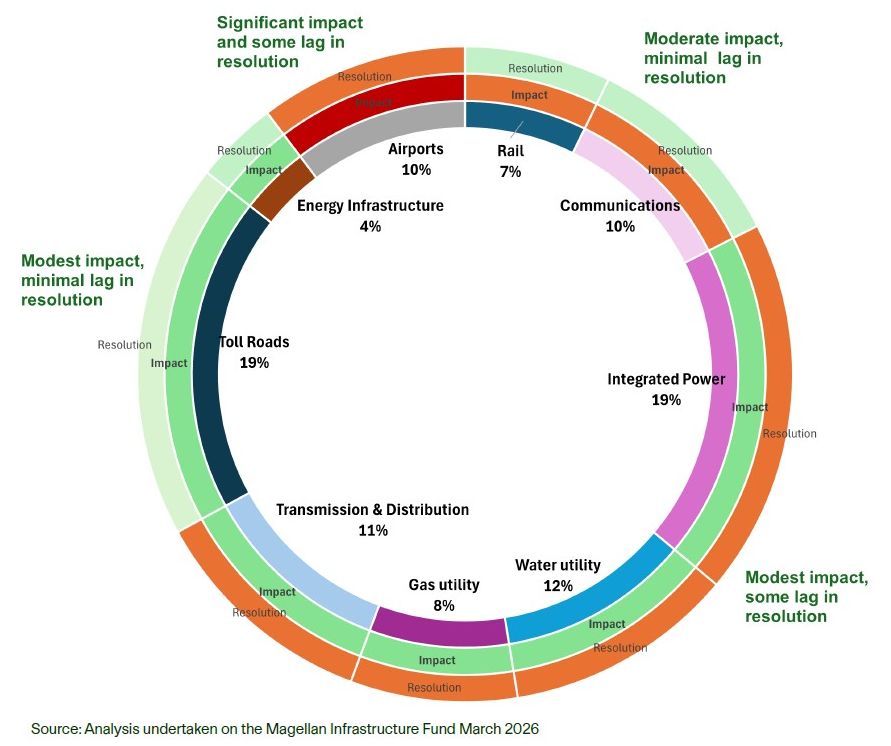

And yet, our scenario analysis (at the end of this article) suggests that while there will undoubtedly be a short-term impact, likely concentrated in airports and toll roads (along with rails and communications), resolution for infrastructure assets should take place over a matter of months. The overall outcome is one of resilience, with infrastructure relatively well-positioned to absorb a supply-driven energy market shock.

Impact

The direct impacts of the energy market shock are felt unevenly across infrastructure sub-sectors.

Some sub-sectors are most exposed to an energy price shock: Airports are top of this list given flight cancellations, higher ticket prices, passengers avoiding Middle Eastern airports (and air travel more broadly) as well as increasing risks of jet fuel shortages. Some airport businesses are better protected (such as Aena, which operates the Spanish airport system and is better insulated from traffic flows with the Middle East), while others have direct exposure to the conflict through ownership of assets in the Middle East, and significant traffic flows to and from the region (such as ADP). We also expect transport infrastructure (such as Transurban, ALX) could be affected, as higher petrol prices and outright shortages of fuel have an impact on travel patterns on toll roads in the near term. However, it should be noted that historically, toll road traffic has shown little impact from fuel price increases and while we have seen a sticker-shock effect, we expect this will normalise quickly in the absence of fuel shortages.

Rail infrastructure is also more exposed. For rail (for example, CSX), the short-term impact can actually be positive, whereby higher oil prices can support a modal shift from trucks to rail. However, as a supply-side shock feeds through to weaker economic activity, there is a negative cyclical impact on freight rail volumes.

For communications, particularly US tower companies that have largely fixed-price escalators, higher energy prices are a headwind as they push through to higher inflation that affects the value of real earnings.

Other subsectors are resilient in the face of a supply-side energy shock: Regulated utilities are in this group. This set includes transmission and distribution companies such as National Grid, gas utilities such as Italgas, US integrated power companies such as CMS Energy and water companies such as United Utilities. These businesses are regulated, earning an agreed rate of return on their capital invested. They also experience dependable demand throughout economic cycles; for example, with residential demand for electricity typically holding firm even as energy, economic and other shocks occur.

Right now, this group – particularly US regulated electricity utilities – has a structural tailwind. Large-scale capex to build generation capacity to meet the demands of data centres, along with investment in renewables, is underway and is not expected to slow.

Resolution

Infrastructure businesses are characterised by demand consistency, and, in our definition, by consistent cash flows. By design, these businesses largely have pass-through mechanisms to recoup inflation and to generate reliable earnings. As a result, we would expect listed infrastructure to recover effectively from surging energy prices. The timing of this recovery is the key, as is the risk of rising interest rates, which complicates the outlook.

Inflation pass-through mechanisms determine the speed of resolution: In a supply-side shock, inflation rises swiftly, which can drive cost pressures for infrastructure companies as input prices jump. Infrastructure assets typically have some degree of inflation pass-through built into their concession or regulatory framework. While there is considerable variability across agreements, there are three broad groups to keep in mind when estimating the recovery profile for an infrastructure company.

The first wave comprises those companies where inflation pass-through is the timeliest. This includes those companies operating in regulatory systems that provide return allowances in real terms, escalating revenues with inflation and indexing debt costs to market yields. Systems in the UK and Australia provide this inflation coverage. The UK water sector (including Severn Trent and United Utilities) has this explicit protection. Rail infrastructure (such as Norfolk Southern and CSX) is also in this wave, reflecting the sector’s discretion to charge rates to customers that support their “revenue adequacy”. These companies can therefore pass through inflation under this standard. Their pricing power is also key.

The second wave includes those companies where inflation is recovered with a modest lag. For utilities, we mean those companies operating in regulatory structures where return and cost allowances are set in nominal terms. This system provides coverage for inflation with a lag. US utilities are in this group as are toll roads. Most toll roads’ pricing mechanisms (such as for Transurban) include quarterly or at most annual toll price reviews. Toll roads generally have low price elasticity, thus the earnings impact is mitigated or in some cases such as where debt costs are largely fixed, can actually benefit in the short term as prices rise faster than debt costs.

Airports (such as Aena and ADP) are somewhere between the first and second waves, with the regulated component of their earnings set on a multi-year basis, with some inbuilt (but not dynamic) protection for inflation. For example, Aena can cover inflation with a two-year lag as adjustments are made in the following financial year. The unregulated businesses typically have revenue-sharing arrangements (for example, for concessions on site), which benefit from retail pricing that quickly adjusts for inflation.

The third wave includes communications infrastructure companies (such as American Tower). US tower companies typically operate under long-term contracts that work largely on fixed-price escalators. Rising inflation can therefore erode real earnings. We note that outside the US, however, some tower companies have more inflation relief and are more akin to airports in terms of cover. For example, European tower company Cellnex has ~65% inflation linked and ~35% fixed-price escalators.

As a result, there is a lag of as little as a few weeks to as much as 6-12 months for an asset’s pass-through mechanism to catch up to rising inflation and then pass on these costs to end users. This is unique to the asset class and is important to charting the sector’s path out of an energy supply shock.

However, we note that this outlook assumes the energy shock is predominantly one of price, not availability. Outright supply disruptions for jet fuel, supply disruptions or fuel rationing for road transport are risks to airports and toll roads. Even if there is a CPI reset on tolling, for example, significantly lower volumes on the roads due to fuel rationing would lead to lower revenues. Such a scenario would mean the recovery takes longer, as activity normalises at the same time as pricing settings are updated.

We are watching for higher real interest rates: Higher interest rates are the second-order effect of higher inflation and have impacts on listed infrastructure companies. The long duration of infrastructure assets means that higher real rates have a negative impact on valuation. A rate-led downturn in economic activity has historically had a larger impact on infrastructure, as compared to an average downturn.

Right now, real rates look contained, and central banks are taking a measured approach to assessing growth and inflation risks stemming from the Middle East conflict. Should we see central banks commencing aggressive hiking cycles, that would have a significant influence on discount rates and asset valuations. Equally, market concerns on fiscal sustainability for major governments (such as big fiscal support packages or defence spending) are a risk to longer-term benchmark rates, should yields start to rise.

If higher rates materialise in the coming months, it is important to distinguish between share price performance and business fundamentals. Companies that are seen as ‘defensive’ are often out of favour when interest rates rise as investors prefer higher-growth sectors. However, this is often a reflection of strong demand environment, not a reflection on the quality of underlying earnings. Over time, businesses that have solid fundamentals should see this reflected in their stock prices.

Outcome

Longer term, infrastructure has sound shock absorption capacity.

This is not an easy period for markets. While uncertainty abounds, one thing we do know is that infrastructure assets have the consistency in demand and cash flows to support their recovery from an energy supply shock.

In the case of roads and airports, the near-term outlook is affected by the current conflict in the Middle East. However, once conditions normalise, we would expect to see a swift return in demand, given solid momentum in population growth and air travel demand that was in place prior to the conflict.

For communications infrastructure, the prevalence of mobile device use suggests that this sector will continue to power through near-term disruptions, with these assets hard to substitute, and demand continuing to grow.

For regulated utilities, their regulated earnings model and consistent demand support sustained cash flows and return on equity through market cycles. There is also a structural growth story in play for this sector, with large capex pipelines (owing to data centre demand and renewables build out) also supporting the outlook for earnings growth.

For our strategies, we note that we do not invest in companies with direct exposure to commodity prices, and consequently, we do not benefit from rising oil and gas prices (for example, through allocation to midstream services companies). However, the run-up in these commodity-price exposed companies is typically short-lived and is followed by a downshift in stock prices as energy markets normalise.

Navigating the impact of energy supply shock on listed infrastructure

From the Infrastructure Investment Team at Magellan Group, a sponsor of Firstlinks. This article has been issued by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 (‘Magellan’) and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs.

For more articles and papers from Magellan, please click here.