There is a point, somewhere around early August, when the global oil market runs out of road if current conditions persist. That is not scaremongering. It is arithmetic, and it is worth understanding the working.

The trigger is the double blockade of the Strait of Hormuz, the narrow waterway through which roughly 20 million barrels of oil per day would ordinarily flow. With that corridor constrained, the world is drawing down its reserves at an unsustainable pace. The clock is ticking, and the market, in my view, has not fully reckoned with what that means.

The numbers that matter

The global oil market consumes around 100 million barrels a day. Of the roughly 20 million barrels a day normally transiting through Hormuz, perhaps 5 million are being rerouted and 3 million are getting through. That leaves a shortfall of around 12 million barrels a day. Factor in approximately 2 million barrels a day of demand destruction caused by already-elevated prices, and you are still left with a 10-million-barrel-a-day hole, being plugged for now by inventory drawdowns at roughly 300 million barrels per month.

We began the year with approximately 8.5 billion barrels in storage across all definitions: crude, products, strategic reserves, pipeline fill, and refinery stocks. We have already committed to losing around a billion barrels. That brings the floor into view. Operational tank bottoms, the minimum inventory the system needs to keep functioning, sit at around 6.5 billion barrels.

If we continue drawing at this rate over May, June and July, we hit tank bottoms globally in early August. And before that, certain countries and geographies will feel the pinch sooner. Regional shortages are likely to emerge over June and July, ahead of any global reckoning.

The price needed to balance the books

Once you hit tank bottom, the calculus changes entirely. You can no longer borrow from storage. Supply must equal demand. And to close a 12-million-barrel-a-day shortfall through price alone, you need an oil price that forces significant demand destruction, particularly in emerging markets where consumers have the least capacity to absorb the blow.

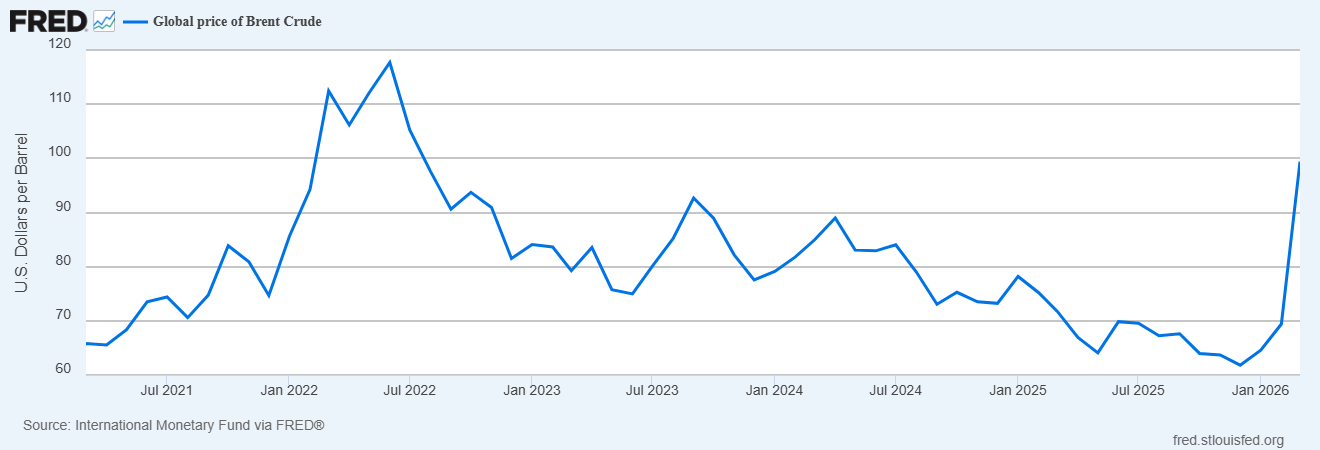

My estimate is somewhere between $130 and $150 a barrel. Brent crude is currently hovering around $107.

That is not a forecast of inevitability. A diplomatic or military resolution to the Hormuz blockade would change the picture considerably. But a solution is needed, and the longer it does not arrive, the more severe the eventual adjustment is likely to be.

Why equity investors are more cautious than you might expect

One might reasonably expect energy equities to have surged in this environment. They have not, and the reason is worth understanding.

Equity investors are wary of what I would call day-one headline risk. The moment a credible diplomatic breakthrough is announced, an estimated 120 million barrels of oil sitting in tankers behind the Strait of Hormuz could hit global markets relatively quickly. That initial price shock would weigh on energy equities, and investors are understandably reluctant to be caught on the wrong side of it.

There is also the sheer noise of the current environment to contend with. News flow is fast, contradictory, and heavily politicised. It is worth noting that when we look at the Brent oil price on screen, we are looking at the prompt month of a financial futures curve, not a physical barrel. The financial flows in these contracts run at roughly 100 times the volume of the physical market. That makes the price highly sensitive to tweets, headlines, and political messaging, some of which may well be deliberate.

The typical futures contract is also only four to six weeks out, and the market's working assumption seems to be that this will be resolved in that timeframe. In my view, the full impact of the disruption has not yet been properly priced in.

Where we are, and what comes next

Energy equities are currently pricing in something closer to $70 a barrel. I believe the mid-cycle oil price needed to balance global supply and demand over the next three to five years is closer to $80. That gap is meaningful, and for investors willing to look through the near-term uncertainty, it may ultimately represent an opportunity.

But the more immediate point is this: the oil market is not broken yet. Inventories are still providing a buffer. There is still time for a diplomatic solution to change the trajectory. What there is not, however, is an unlimited runway. The buffer is finite, the drawdown rate is high, and the mathematics of the situation are unambiguous.

The market may be used to living with geopolitical noise. What it is less accustomed to is a situation where the noise has a hard deadline attached to it.

Paul Gooden is Head of Natural Resources and a co-portfolio manager for the Global Natural Resources strategy at Ninety One.