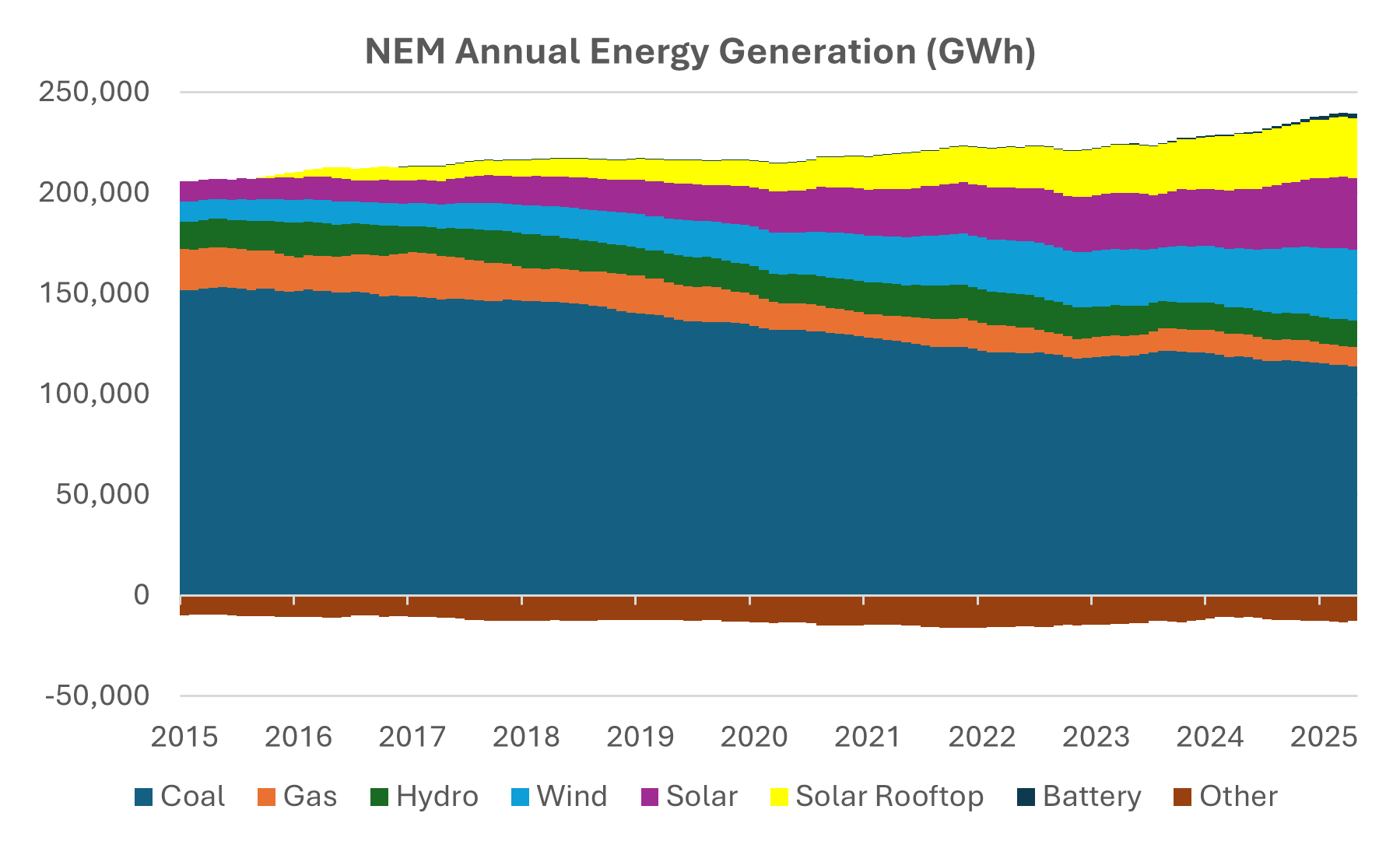

Australia's electricity mix has changed dramatically over the past decade. The chart below tells the story of coal in steady retreat and rooftop solar surging from a rounding error before 2015 to 14 percent of National Electricity Market (NEM) generation by 2025.

Source: OpenElectricity

That transformation created a new problem. A grid that generates enormous solar surpluses during the day and loses that generation as the sun sets develops a structural imbalance in the evening. The 6pm to 9pm window is the grid's critical stress point: supply falls, demand peaks, and prices spike. Two energy storage projects now define Australia's attempt to solve it. Both exceeded their original budgets, but for entirely different reasons, and one is at risk of looking like a white elephant.

Snowy Hydro 2.0: The nation-building bet

In March 2017, Prime Minister Malcolm Turnbull announced Snowy Hydro 2.0 as a nation-building response to Australia's energy crisis. South Australia had suffered a state-wide blackout in September 2016. Electricity prices were surging as domestic gas prices rose sharply after new LNG export facilities linked the east coast gas market to international prices for the first time. Hazelwood, one of the NEM's largest and cheapest coal-fired generators, was weeks from closing. The political pressure to act was intense.

The project proposed linking two existing reservoirs — Tantangara at the top and Talbingo at the bottom — via a 27-kilometre tunnel through the Snowy Mountains. The scheme uses cheap electricity during the day to pump water uphill into Tantangara, then releases it back down through turbines to generate power when electricity is expensive in the evening. At full capacity, the project would add 2.2 GW of dispatchable generation to the NEM.

The original $2 billion cost estimate was produced without a detailed feasibility study. A subsequent study revised that to $3.8 to $4.5 billion, and the project was formally sanctioned by the Morrison Government in February 2019. Construction began in 2021, and the cost estimate has since risen to at least $12 billion. Independent analysts at the Victoria Energy Policy Centre now estimate the all-in cost at $42 billion.

The Cheaper Home Batteries Program: A cost-of-living bet

The Cheaper Home Batteries Program launched in July 2025 as rising electricity bills put household energy costs at the centre of the 2025 federal election campaign. The scheme addressed a clear market failure: despite solar sitting on one in three rooftops, only one in 40 households had a battery. The high upfront cost was the barrier. Batteries offered households a direct way to reduce their exposure to retail tariffs and relieve cost-of-living pressure.

The scheme offered households a 30 percent discount at the point of installation, targeting 1 million installations by 2030 with an original budget of $2.3 billion. Within five months, 155,000 new batteries had been installed, roughly matching half the entire fleet accumulated over the prior decade. The budget was on track to run out by 2026, and in December 2025 the government responded by tripling the budget to $7.2 billion, doubling the installation target to 2 million and quadrupling the storage target to 40 GWh.

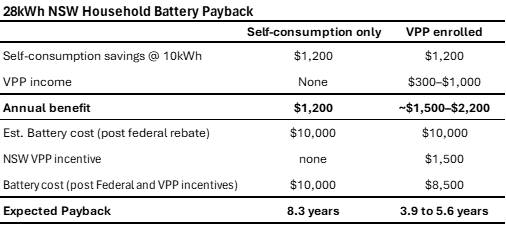

The financial case was compelling from day one. Most household batteries operate in self-consumption mode, charging from rooftop solar during the day and discharging at night instead of buying grid power at around 38 cents per kWh. Without a battery, that solar would be exported to the grid at around 5 cents. Based on typical evening consumption of around 10 kWh, the arbitrage is worth about $1,200 per year in bill savings

Some households go further by enrolling their battery in a Virtual Power Plant (VPP), a network where an operator coordinates discharge in response to grid conditions. In exchange, households earn a fee from the operator ranging from $300 to $600 annually, or on more sophisticated plans, a share of returns from capturing price spikes with the potential to exceed $1,000 annually. In NSW, the state government adds up to $1,500 upfront for connecting to a VPP on top of the federal rebate, making enrolment a compelling financial proposition.

Source: Vertium

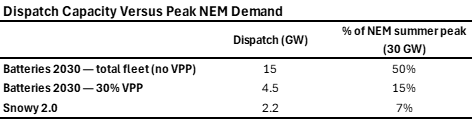

Scaled to 2 million households, those individual decisions become a grid-scale resource. At 2030 target scale, 2 million households drawing from batteries rather than the grid removes the equivalent of 50 percent of NEM summer peak demand from the wholesale market entirely. That is without any coordination. With coordination, the impact is even greater. Given state government incentives, VPP enrolments could reach 30 percent of batteries installed by 2030. Six hundred thousand batteries discharging at an average rate of 7.5 kW gives a peak dispatch capacity of 4.5 GW, covering a further 15 percent of NEM summer peak demand and about double Snowy Hydro 2.0's discharge capacity. Any price spikes that remain will be targeted by those VPP batteries, leaving little commercial headroom for Snowy 2.0.

Source: Vertium

The commercial implications extend beyond Snowy. Gas-fired peakers earn the bulk of their revenue running precisely when evening prices spike. AGL and Origin are building their own grid-scale batteries to capture the elevated prices in the evening ramp, even as distributed household batteries work to eliminate them. Origin has argued that more gas-fired peaking capacity is needed as coal retires, a position that has genuine merit for multi-day winter periods when solar is weak and batteries cannot recharge in time. That argument is harder to sustain on the daily evening ramp, where batteries are already proving their case. In Q1 2026, the peak summer quarter, AEMO reported that batteries delivered an average of 1.1 GW into the evening peak, directly reducing reliance on gas. Gas-fired generation averaged just 712 MW for the quarter, its lowest level since 1999. For AGL and Origin, the structural question is not whether household batteries affect their peaking revenue. It is how quickly that effect is felt.

Snowy faces the same commercial pressure on the evening ramp, but its position is more nuanced. Unlike gas peakers, it can store energy and dispatch it without burning fuel. But like gas peakers, it can sustain output for far longer than a home battery. A home battery is exhausted within five to six hours at full discharge. Snowy can sustain 2.2 GW continuously for approximately 18 hours to four days depending on reservoir levels, becoming genuinely irreplaceable during the prolonged overcast periods that Origin describes. That is a legitimate grid service for those rare instances, but it could easily be met by existing gas-fired peakers without costing taxpayers a cent.

Conclusion

Both schemes exceeded their original budgets, but that is where the similarity ends. Snowy Hydro 2.0 was a single concentrated bet — costed without engineering rigour, committed without market validation, and now carrying an estimated price tag of $42 billion. The home battery scheme was messy in its first iteration, but it mobilised private capital at a scale that forced the government to expand the subsidy to $7.2 billion to keep pace with demand. One budget blew out because demand exceeded expectations. The other blew out before it produced anything.

Snowy is 70 percent bored, has missed six consecutive completion deadlines, and is realistically not expected to operate until the early 2030s. By then, the battery scheme will have run its full course — 2 million homes, 40 GWh of distributed storage, and years of evening peak prices already compressed. Snowy will arrive, at extraordinary cost, to find the market it was designed to serve already transformed. That transformation has a price.

The price of that transformation: $7.2 billion. The price of Snowy 2.0 could be $42 billion too late.

Jason Teh is the founder and Chief Investment Officer of Vertium Asset Management; and a Portfolio Manager at Clime Investment Management Limited, a sponsor of Firstlinks. This article is general in nature and does not constitute or convey personal financial advice. It has been prepared without consideration of anyone’s financial situation, needs, or financial objectives. Before acting on the areas discussed and contained herein, you should consider whether it is appropriate for you and whether you need to seek professional advice.

For more articles and papers from Clime, click here.