The debate over artificial intelligence has taken a sharp turn. Initial exuberance over AI’s transformative potential sparked investor fears of an AI bubble. But that concern has now been overshadowed by anxiety that the AI juggernaut will steamroll large segments of the global economy.

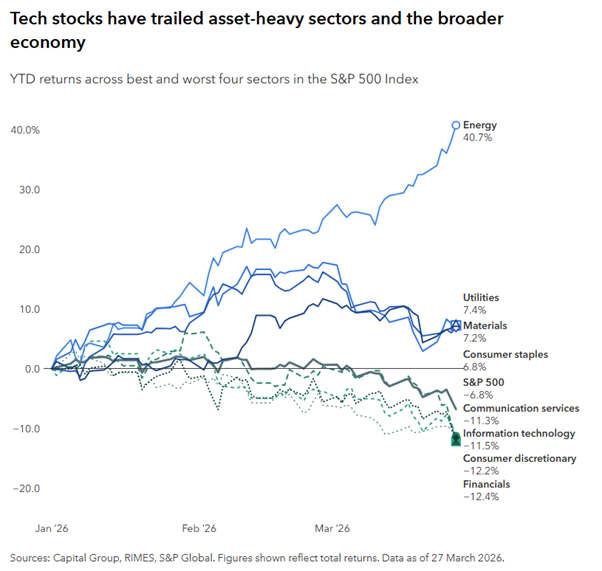

The evolving narrative has driven starkly divergent outcomes for companies. Investors have fled so-called ‘AI roadkill’ — business models such as software that are expected to be rendered obsolete by AI — favouring old-economy companies that produce physical goods. Although overall returns for the S&P 500 have been negative this year, the energy, materials and industrials sectors have generated solid gains while software and other capital-light industries have suffered sharp declines. Since the start of the Iran war, energy has continued to soar while gains in other asset-heavy industries have moderated.

How should long-term investors think about investing amid these shifts?

My colleague Brittain Ezzes, equity portfolio manager, believes that we are “in the early stages of understanding AI’s impact on business models. For some it will be highly disruptive. For others it will have a more neutral or even a positive impact. But it would be a mistake to underestimate AI’s potential to reshape the economy.”

As the AI narrative evolves, here are three areas that Capital Group are concentrating on amid the twists and turns.

1. AI immune businesses

Sectors tied to real assets and physical production — coined by Ritholtz Wealth Management CEO Josh Brown as HALO stocks (heavy assets, low obsolescence) — are perceived to have AI immunity. AI cannot, for example, make hamburgers, replace copper wiring, or ‘vibe code’ jet engines.

Arguably, we are seeing a renaissance of the physical economy. There are a number of factors that can potentially perpetuate the rally in capital intensive value stocks.

For starters, industrial and manufacturing companies appear to be emerging from a long slump. Some companies took steps to streamline operations and cut costs so they would be better positioned to participate in broader growth. For example, within the transportation industry, railroad operator Union Pacific has disclosed plans to acquire rival Norfolk Southern Railway, creating a transcontinental line that would connect stops across the US and Canada. This could help reduce transit times, boost competitiveness with trucking and lower costs for customers. Rival CSX similarly has taken steps to cut costs and boost efficiency.

Among industrials, soaring demand for air travel and rising defence budgets around the world have created strong tailwinds in the aerospace and defence industries. For example, GE Aerospace saw the order backlog for its jet engines rise to $190 billion at the start of the year. US defence contractor RTX, known for its sophisticated radar and missile defence systems, has seen orders climb as European and Middle Eastern nations seek to modernise their militaries. Some of my colleagues believe we are in the middle of a supercycle for aerospace.

Within the restaurant industry, consumers are still likely to go to restaurants to have humans serve them. Take coffee shop Starbucks, for example, which emphasises the customer experience. CEO Brian Nicole, who has a strong track record of turnarounds in the industry, has demonstrated a detailed knowledge of company operations.

The health care sector has come under pressure because of regulatory and pricing changes but it includes manufacturers of heavily regulated products that are hard to replicate. For example, Medtronic, a maker of surgical devices, operates more than 70 manufacturing plants globally. The company has taken steps to cut costs, including consolidating distribution centres and spinning off its diabetes division. Their businesses have high barriers to entry, and with populations getting older, demand for medical procedures is likely to rise.

2. Babies in the AI bathwater

Companies considered highly vulnerable to AI disruption, referred to earlier as AI roadkill, include a wide range of software, financial and consulting industries. After AI developer Anthropic said in February that its agentic AI tool Claude could automate a range of research and legal tasks, providers LegalZoom.com, Thomson Reuters and FactSet Research Systems suffered steep declines.

My colleague Mark Casey, equity portfolio manager, says that the market appears to have concluded that many software as a service (SaaS) companies will go into perpetual decline as a result of AI-enabled competition. “Probably some of them will, but others seem well insulated from AI risks, and still others seem set to benefit from AI. I am looking closely at many of these companies in search of the proverbial babies that have been thrown out with the bathwater.”

For example, Salesforce, a customer relationship management platform, has been a focal point of disruption fears and its share price has declined sharply this year over concerns that AI tools make it easier for customers and competitors to replicate its functionality. At the same time, the company is taking aggressive steps to integrate AI features into its offerings. The company’s status as a system of record and deep integration with key business workflows may provide it with sufficient advantages to fend off AI-powered competition.

IT consulting businesses such as Gartner and Accenture, which offer research and advice to businesses about technology decisions, have also come under fire.

Both companies have launched initiatives to help clients identify use cases for generative AI, adopt AI tools and integrate them into organisations. What’s more, the complexity of IT decision-making is not getting simpler in the age of AI.

3. AI picks and shovels

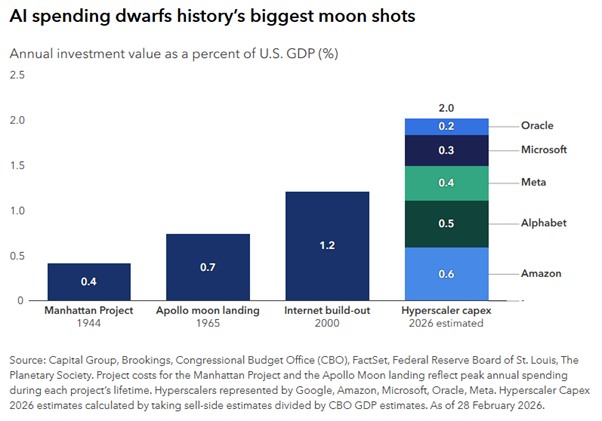

You cannot build a new economy without old economy companies. It is well known that the AI buildout relies heavily on makers of power generation and cooling equipment, utilities and mining companies. These are the proverbial picks and shovels supplying AI infrastructure.

The hyperscaler companies driving the AI revolution have committed to investing $650 billion in capital expenditures, primarily to build out AI data centres. To put this in context, it is more than 2.5 times the amount spent in 2025. The historic spending could account for an estimated 2% of GDP, far larger than other major capital projects in history, including the Manhattan Project and the Apollo space mission in 1965. Those projects led to innovations that reshaped industries for decades and led to the creation of new companies.

At the heart of the AI infrastructure build-out are semiconductors, and the flood of investment by the hyperscalers has created historic opportunities for companies across the semiconductor complex. Examples include Nvidia, which makes graphic processing unit chips essential for AI’s large language models, and Broadcom, a maker of networking chips. Both have reported record sales growth in recent quarters. In addition, Applied Materials has seen soaring demand for its equipment as chip manufacturers look to expand and upgrade facilities.

The AI spending boom is also generating growth opportunities for power generation and capital equipment companies. For example, heavy equipment maker GE Vernova has reported a multi-year backlog for its gas turbines and extended lead times for electrical equipment orders. Demand for HVAC (heating, ventilation and air conditioning) equipment has also outpaced supply, prompting manufacturers like Carrier Global and AAON to boost manufacturing capacity.

A stock pickers’ market

AI technology remains in the early stages of both development and adoption. Yet it is already emerging as a powerful force in the economy that should not be underestimated. As the AI narrative evolves, it will be beneficial for some companies and serve as a disruptive force for others.

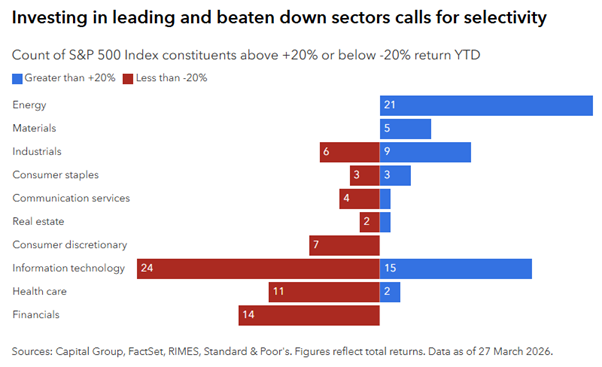

But AI’s impact will not be uniform. Both the soaring industrials sector and the beaten-down tech sector have included stocks with 20% gains as well as stocks with 20% declines in the first two months of the year. Whether an investor looks for opportunities among those companies whose shares have soared or software and consulting companies whose shares have plummeted, the key for long-term success will be selective investing supported by intensive research.

Matt Reynolds is an Investment Director for Capital Group Australia, a sponsor of Firstlinks. This article contains general information only and does not consider the circumstances of any investor. Please seek financial advice before acting on any investment as market circumstances can change.

For more articles and papers from Capital Group, click here.