Alphabet's Google changed the game of advertising as Google's seamless integration of ads into its search engine revolutionized relevance and efficiency in online advertising. Google, with its Page Rank innovation and capital-light model, became a dominant force in its industry.

Alphabet now faces a shift from nimbleness toward an infrastructure-heavy approach that slows down the very strengths that once defined its dominance. From here, Alphabet's future is likely to involve lower returns on new investments, higher spending on capital-intensive projects, and less opportunity for the effortless growth and compounding that investors have come to expect, in our opinion.

Below, we highlight three reasons we worry about the investment future of Google, Alphabet's largest subsidiary, and why we do not own the stock as of the date of this publication (23 March 2026). For full disclosure, Alphabet was among our top holdings in early 2024. While we do not currently own the stock, we may consider owning it again in the future should its fundamentals and valuations align with our investment criteria.

1. Challenges from AI and a saturating digital advertising market

After dominating the search market for years with minimal competition, Google's core search business is now under siege by a new generation of Al-powered competitors.

Google – despite owning its own Al-driven search tool, Gemini – now finds itself grappling with the rise of OpenAl's ChatGPT, xAl's Grok, and Anthropic's Claude. These competitors represent a major disruption to Google's traditional ad-driven model.

Even if Google emerges as the leader in Al search with the integration of Gemini, its business model is likely to suffer, in our view. The traditional search model relied on users clicking through to publisher websites-commonly known as "10 blue links" generating multiple ad impressions along the way. Since Google's incorporation of Al into its search results, which provides direct, synthesized answers, user click-through rates collapsed. Analysts estimate that over 50% of Google searches could now end without a single click to any website. This behavioral shift cannibalizes the primary revenue stream that built the business.1

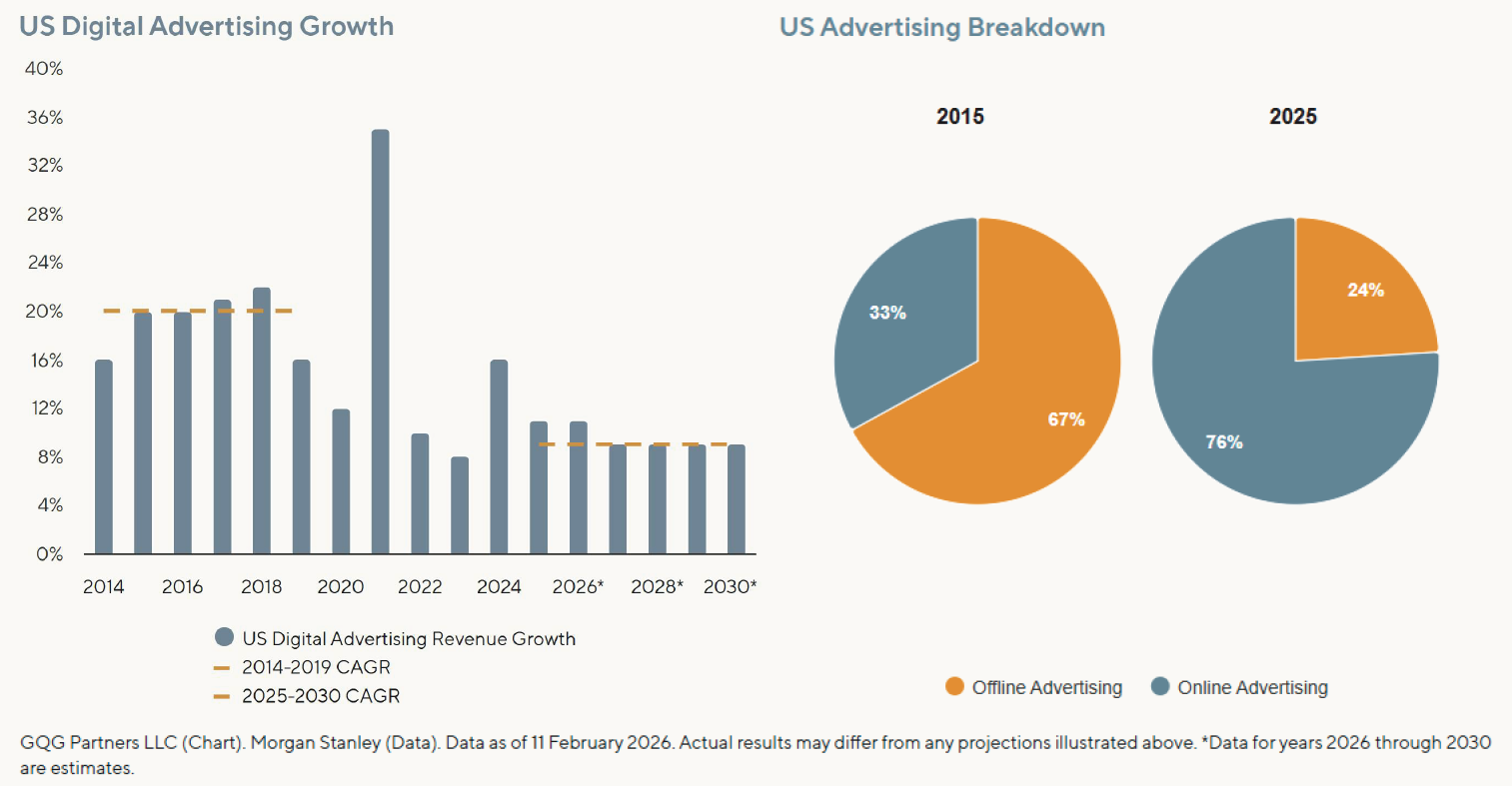

Advertising bulls argue that Al will expand the total addressable market, suggesting that greater productivity will push advertising to occupy a larger share of GDP. However, historical data argues otherwise. Despite seismic shifts in media from print to radio to television to the internet to mobile, global advertising spend has consistently remained at 1% to 2% of GDP for over a century. We think the strong growth of the 2010s was a recovery from the post-dotcom "lost decade," not a fundamental shift in the market. Today, advertising spend as a percentage of GDP has returned to its 2000 highs, suggesting little room for further expansion.

2. Escalating costs without clear returns

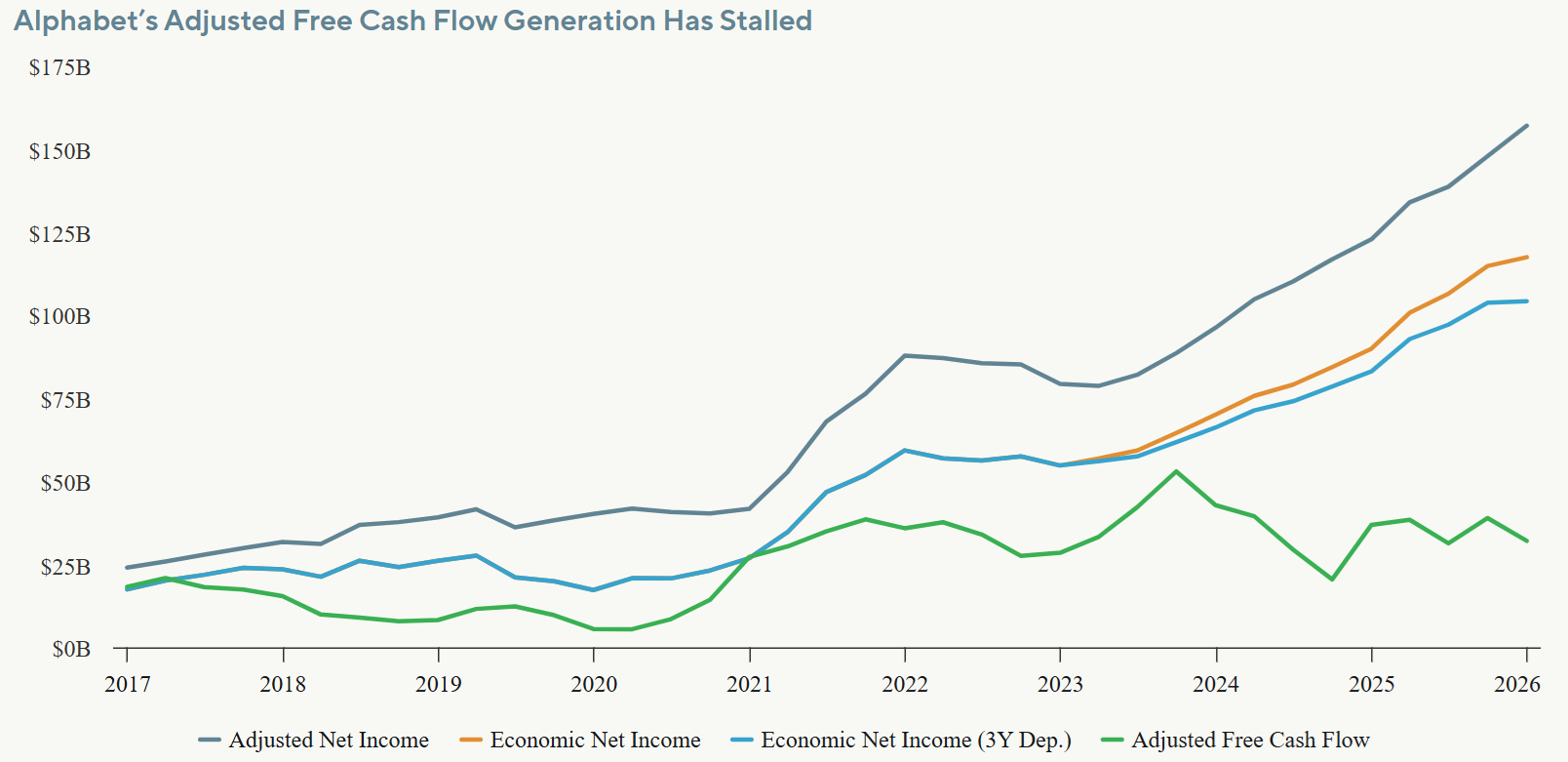

While Alphabet’s core business faces significant challenges, the company has diverted its focus to AI cloud infrastructure. Bulls argue that Google Cloud will accelerate revenue growth and deliver operating leverage. However, the mounting costs and high capital intensity offer no guarantee of a triumphant outcome. This financial strain is already evident, as adjusted free cash flow (FCF) has stagnated since 2021 and is projected to decline in 2026. We think the gap between the optimistic narrative and the sobering reality can largely be attributed to two key factors: stock-based compensation (SBC) and the accounting treatment of capital expenditures.

3. Cyclicality and overvaluation amid slowing growth

Advertising is one of the most economically sensitive line items in any budget. It tends to be the first thing companies cut when conditions tighten. As the world’s largest advertising platform, Google is a direct reflection of this cyclicality. We believe that 2026 represents a similar set up to the 2022 cycle.

A trip down memory lane

During the COVID stimulus boom of 2020-2021, businesses aggressively expanded their digital advertising. Revenue growth for Google Services (search ads, YouTube ads, network ads, and subscriptions) climbed from $152B in 2019 to $169B in 2020 (11% year-over-year growth) to $238B in 2021 (41% year-over-year growth).

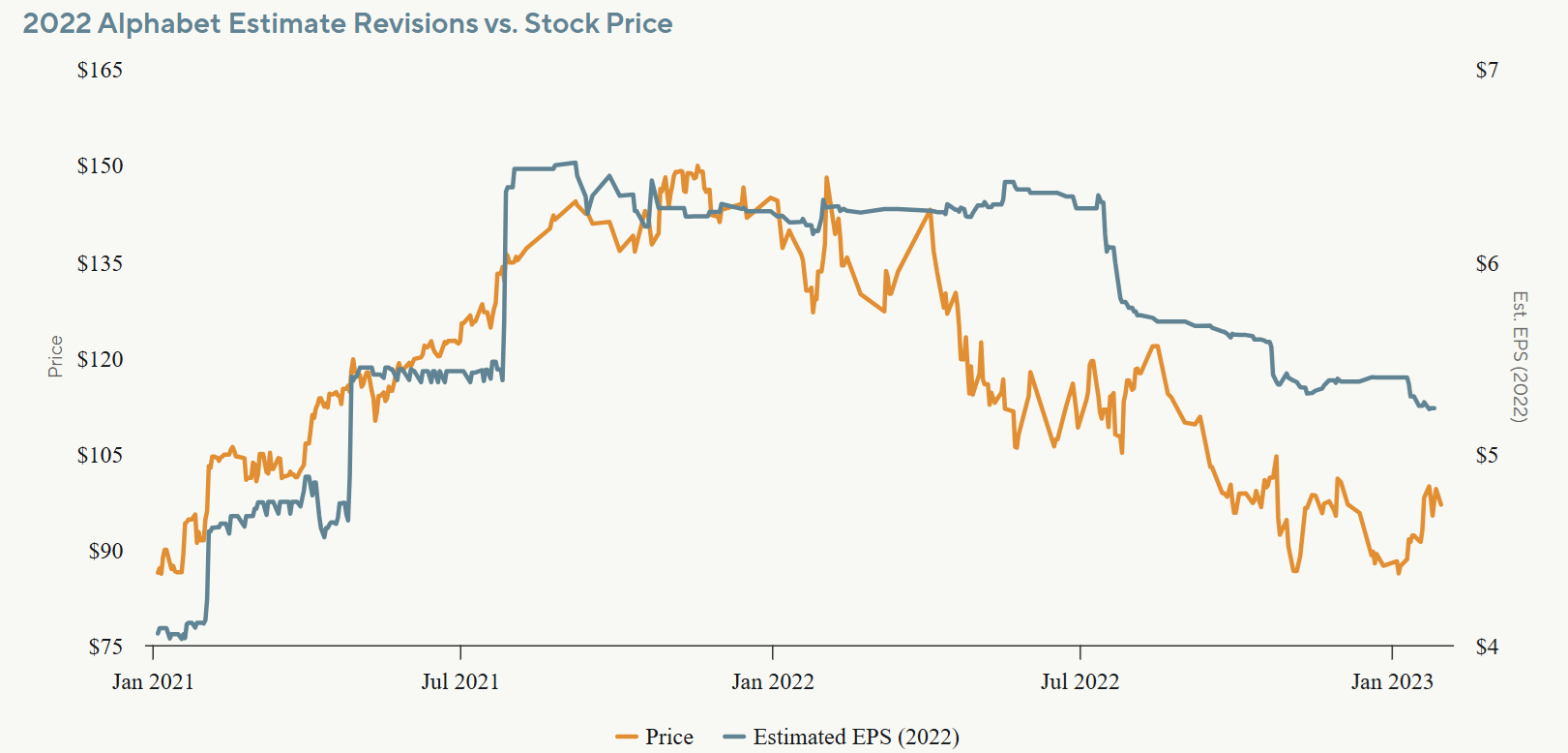

After inflation began to ripple through the economy and the Federal Reserve responded by hiking rates aggressively in 2022, the business cycle turned. Alphabet’s financial performance responded in the same cyclical fashion: Google Services’ revenue growth slowed to 6.7% year-over-year, and net income fell 21% leading the stock to plummet nearly 40% over the course of that year.

The painful irony is that management, investors, and Wall Street had been warned and still got caught. Google’s management team went on a spending spree leading into the downturn. In March 2021, CEO Sundar Pichai announced in a blog post: “We plan to invest over $7 billion in offices and data centers across the US and create at least 10,000 new full-time Google jobs in the US this year.”2

As late as February 2022, CFO Ruth Porat was confidently describing “broad-based advertiser strength and strong consumer online activity.”3 When the downturn hit, Google was forced to reverse spending plans and enact job cuts. In a May 2024 post-mortem, departing Porat admitted: “A couple of years ago we actually got that upside down and expenses started growing faster than revenues. The problem with that is – it’s not sustainable.”4

Fast-forward to today

The lessons of 2022 have already been forgotten. Alphabet has embarked on a spending binge far larger than 2021 – this time concentrated in physical infrastructure that cannot be offset by job cuts and must be depreciated over years. Compounding this, the consumer economy has weakened into a bifurcated “K-shaped” pattern, with clear stress in major cohorts. Yet, consensus still expects double-digit advertising growth into perpetuity.

Current Wall Street estimates have Google Services growing at low-double-digits in 2026, with mid-single-digit net income growth.5 If Google Services simply grows in line with the overall digital advertising market, say 8%, we project earnings growth would turn negative, just as it did in 2022. The sensitivity analysis is stark. These are not tail risks; they are realistic scenarios the consensus is pricing as near impossibilities, in our view.

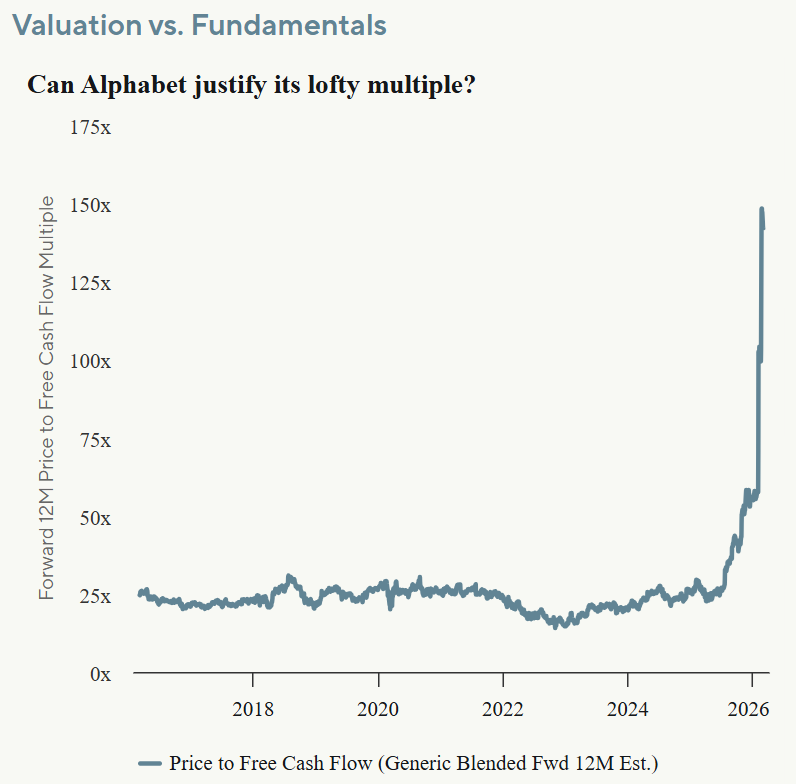

Alphabet is currently trading at roughly 27x its expected earnings for the next twelve months, which is near the top of its historical valuation range. We believe this high multiple leaves no room for the company to miss earnings expectations. The situation appears even more concerning on a cash-flow basis, as the stock trades at 133x its expected FCF for the next year – far higher than its pre-COVID multiple of approximately 20x. This is despite the fact that its FCF has stagnated since 2021.

The bottom line

We think Alphabet’s pivot from an agile, capital-light business model to one of the world’s heaviest infrastructure spenders exposes its weaknesses. The path forward for Google suggests not effortless elegance, but the grinding challenges of maturity, where the returns on effort diminish. In our view, the next few years will likely be marked by estimate cuts and multiple contractions, signaling significant challenges for Google investors.

End notes

1Chapekis, Athena and Lieb, Anna. “Google users are less likely to click on links when an AI summary appears in the results.” Pew Research Center. 22 July 2025.

2Pichai, Sundar. “Investing in America in 2021.” The Keyword. 18 March 2021.

3Alphabet Inc. 4Q 2021 Earnings Call. February 2025.

4Elias, Jennifer. “Google employees question execs over ‘decline in morale’ after blowout earnings.” NBC Philadelphia. 10 May 2024.

5Bloomberg consensus estimates. 10 March 2026.

This is an abridged extract of GQG Partners’ recent long-form article “Not Much Alpha Left in This Bet”. You can read the full article here. This article contains general information only, does not contain any personal advice and does not consider any prospective investor’s objectives, financial situation or needs. Before making any investment decision, you should seek expert, professional advice.