A Productivity Tax exists when the interplay of different taxes means high productivity businesses pay a higher tax rate than low productivity businesses.

A high productivity business is a business that grows fast, at a speed above inflation; low productivity businesses grow more slowly, usually at or below the inflation rate.

High-productivity businesses create more jobs and more economic activity. Low productivity businesses do the opposite, often shedding jobs over time.

In a profound oversight, a new economic analysis shows that the new business tax regime announced in the recent federal budget creates this exact situation.

Two identical businesses, delivering the exact same service, one highly productive, the other unproductive, will now face vastly different effective capital gains tax rates.

As the example below shows, the high productivity businesses, the business that creates more jobs and more economic growth, will pay a vastly higher rate of capital gains tax on the sale of the business than a low productivity, low growth business.

How the 'productivity tax' works in practice

There are two industrial cleaning businesses started at the same time, by two different husband-and-wife teams. Both couples are in their early thirties.

Business 1 is a low productivity business. Business 2 is high productivity.

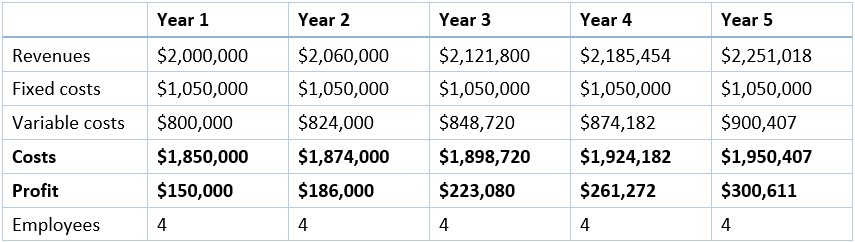

They both begin with an initial investment of $450,000. This is the life savings of both husband-and-wife teams. Both businesses generate $2,000,000 of revenue in their first year. Both have 4 employees, and both generate a profit of $150,000 in their first year.

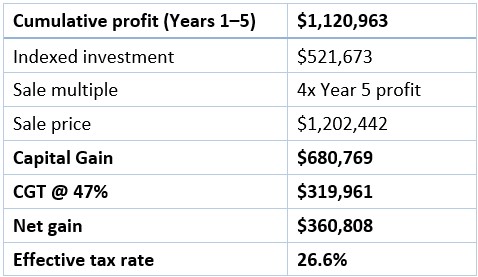

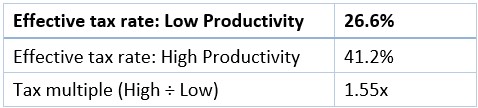

Over the next five years, Business 1 – the low productivity business – grows at 3% a year, ends up generating a profit of a little over $300,000 in the 5th year, and is sold for 4 times that – around $1.2 million. It still employs 4 people. With inflation at 3% a year, Business 1 has a taxable capital gain of $680,000. Under the new capital gains tax regime, they pay 47 cents on the dollar, or about $320,000 in CGT. That’s an effective tax rate of 26.6% of the sale price.

Business 1: Low productivity business, with a growth rate of 3% p.a., inflation rate of 3% p.a. and initial investment of $450,000:

Business 1: profit, capital gain and effective tax rate:

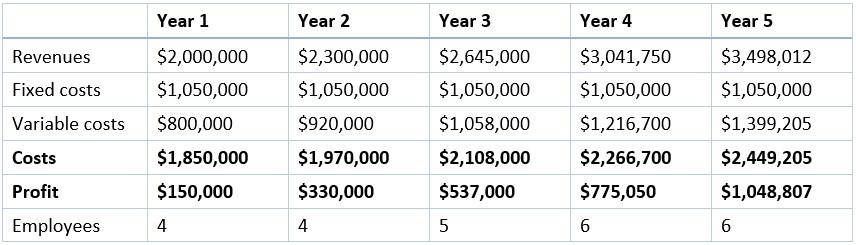

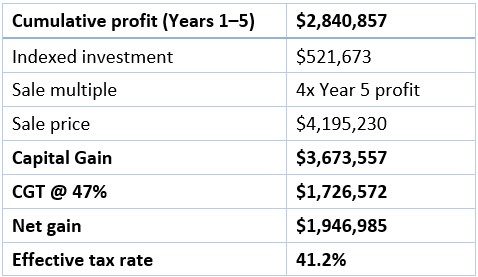

Over the same five years, Business 2 – the high productivity business – grows at 15% a year each year for 5 years. They end up employing 6 people. They also sell it for 4 times the year 5 profit of $1.05 million, or $4.2 million. They have a taxable capital gain of $3.67 million, pay $1.7 million in CGT, for an effective tax rate of 41.2% of the sale price.

Business 2: High productivity business, with a growth rate of 15% p.a., inflation rate of 3% p.a. and an initial investment of $450,000:

Business 2: profit, capital gain and effective tax rate:

Both businesses took a risk, grew a business, employed people, and paid tax, and both sold for the same multiple of profit. It’s just that Business 2 was more productive.

In return for this high productivity the couple who started Business 2 are punished with a capital gains tax rate more than 55% higher than the owners of Business 1.

In other words, the new tax system will now punish businesses more likely to create jobs and economic growth, and reward businesses more likely to shed jobs.

This is the worst possible plan for a country in need of more jobs, and more economic growth. It’s a Productivity Tax in the middle of a productivity crisis.

Unfortunately, that is the perverse logic of a Productivity Tax, they punish high productivity businesses for doing well, growing fast, and creating more jobs.

Young people will pay the biggest price for this profound policy error, because they will miss out on the jobs, growth, and prosperity that productive businesses create.

Richard Holden is Vice-Chancellor’s Professor and Chief Societal Economist at UNSW Sydney. He is also Director of the Economics Manos Institute for Cognitive Economics, and President Emeritus of the Academy of the Social Sciences in Australia.

This article was originally published by UNSW’s BusinessThink research platform.