Markets seem bulletproof. World equities have pushed to all-time highs in the face of unresolved tensions in the Middle East and associated dangers for the world economy. ‘Buy-the-dip’ is alive and well. And ‘staying the course’ in the face of evident threats has once again proven sound advice.

What if markets failed to deliver over an extended period of a decade or more? We focus on the possibility of such a scenario from a superannuation (super) perspective, although the implications go broader.

Operating on the assumption that markets will always deliver over longer timeframes is misguided. History offers numerous examples of negative real (inflation-adjusted) returns being generated over a decade or so. This has happened even for the US equity market over 10% of the time. World equity markets took over 10 years to recover their prior peak in real terms during the 1970s stagflation. The bursting of the tech bubble in 2000 was subsequently followed by the GFC such that sustained recovery did not eventuate until after 2010. Not to mention Japanese equities spending around 30 years in the wilderness.

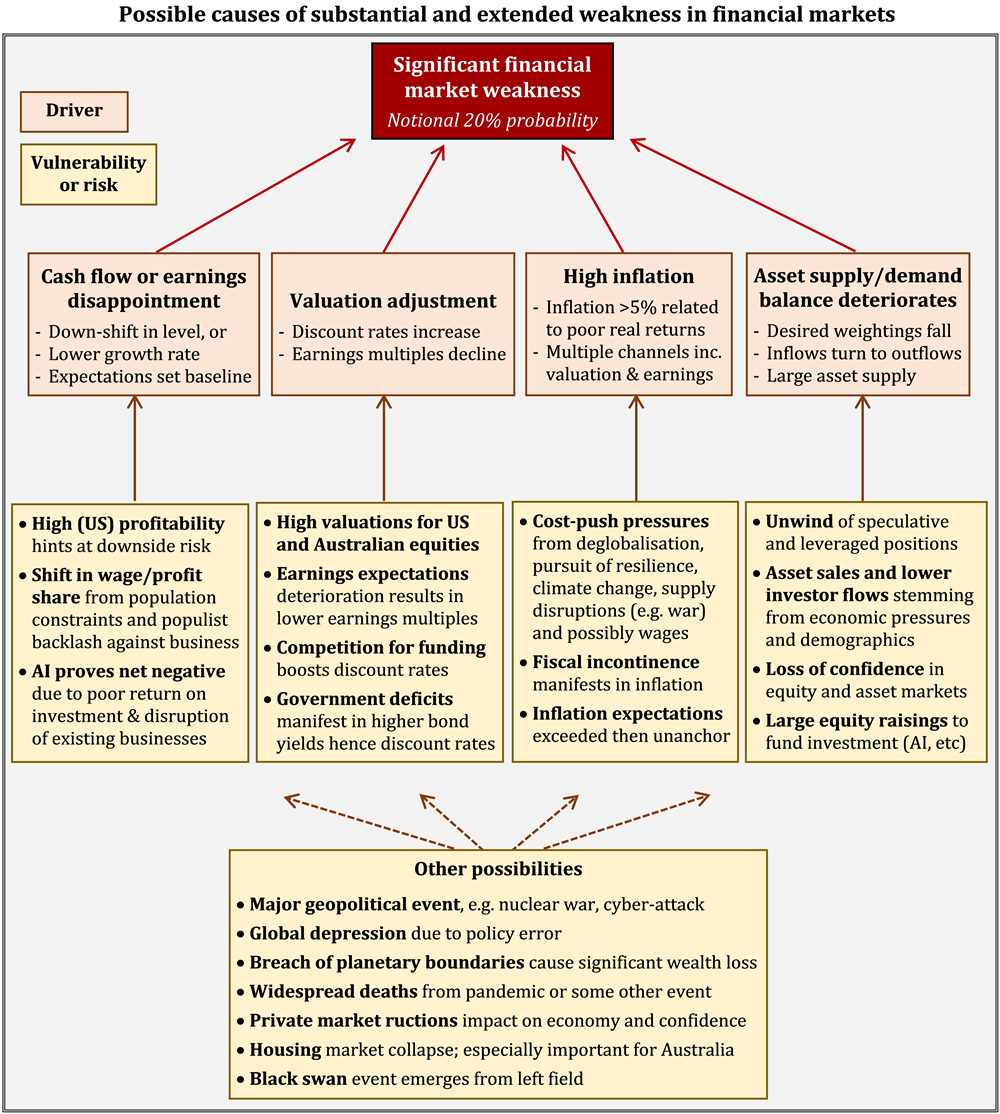

The diagram below summarises possible causes of significantly poor returns comprising a set of four drivers coupled with a range of vulnerabilities and risks that could impact through the drivers. While many items are listed, we will focus on markets being priced for things turning out fine as a set-up.

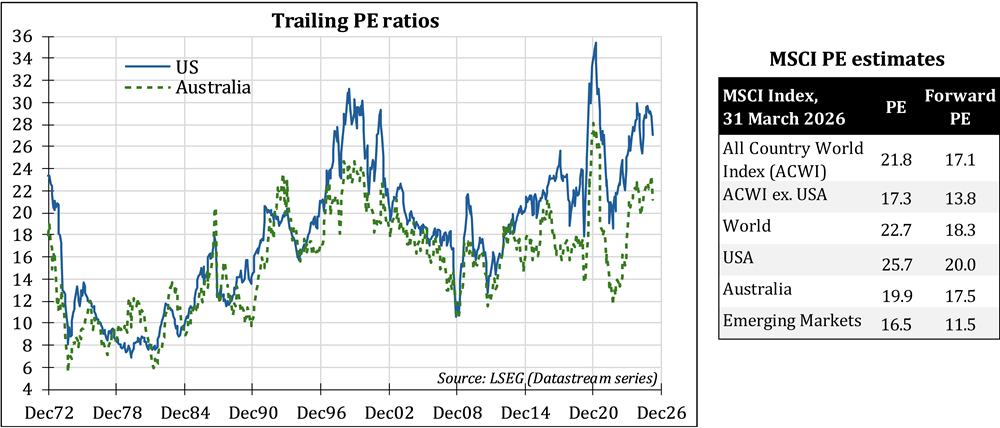

Both US and Australian equity markets appear richly priced: together they comprise around 46% of APRA-regulated fund portfolios. In the past, high valuations have preceded significant weakness by creating room for markets to swing from pricing for optimism to pessimism. The chart and table below report PE multiples at end-March 2026.

The high multiples for US equities are being placed on US profitability at or near historic highs on many measures. It is sobering that a joint reversion in the US return on equity and PE to their historical means could manifest in a price decline of around 45%–50%. Australian equities trade on relatively high multiples versus history and other markets, with the latter even more pronounced on a sector-by-sector basis (the banks are a stand-out).

Markets are also priced for inflation remaining well under control. There are various ways these expectations could prove too optimistic (see previous exhibit), triggering cascading impacts on economies and markets driven by monetary tightening and higher interest rates.

This is not to say that negative real returns over the span of a decade is the most likely outcome. We notionally give it a 20% or 1-in-5 chance, noting that there are also reasons why markets could remain resilient. The point is that an extended period of weakness is possible. And if it does happen, a range of pressures could be brought to bear on the super system and more broadly.

Obviously, super would deliver much worse outcomes than hoped and planned for. We estimate that income sourced from super could be around 30% lower if 10-year real returns turn out to be zero rather than +3%. However, the income loss is reduced to less than 10% for many members after including the Age Pension in the calculations, reflecting means testing and a higher baseline income. This implies that the implications would be more significant for wealthy individuals who are self-funding their retirement than those with lower assets that will receive the Age Pension at some stage.

The flip side is that the government budget would be hit by higher expenditure on the Age Pension as more retirees draw more heavily on the Age Pension along with lower super-related taxes. Ballpark estimates suggest that 10 years of zero real returns would cost the budget about $17 billion in real terms due to higher Age Pension payments – equivalent to about 0.5% of GDP versus existing projections for the Age Pension to cost around 2.2% of GDP.

Confidence and trust in super could be severely eroded. Super funds and the super system at large would likely receive blame from members who see their savings being eroded while being implored to ‘stay the course’. Members who have lost confidence and trust in super may set out to take control for themselves despite many being poorly placed to do so, potentially to their own detriment.

Calls for early release of super may re-emerge. Market weakness is more likely to occur when the economy is under strain and households under stress due to job losses, etc. The idea that ‘people are struggling and need their money now, not later’ could prove politically popular and hard to resist.

All this could have flow-on impacts on super fund liquidity and their market activities. A run on a fund that is considered vulnerable and has lost the confidence of members might even occur.

In short, it could get quite untidy.

What might be done to prepare, just in case? Unfortunately, attempting to avoid exposure to market weakness can be counterproductive. De-risking or taking portfolio protection typically lowers expected return and could lead to poorer long-term outcomes. Successfully anticipating and dodging sell-offs is extremely hard to do, except for the very skilled or lucky.

One could aim to build more resilient portfolios by limiting exposure to concentrated risks and enhancing flexibility. Worthwhile, but that only goes so far.

Modulating expectations is important. ‘Buy the dip’ seems to be gaining a religious fervour, while the super and investment industries typically convey the message that ‘everything will turn out fine if you just stick to the strategy’. What if (when) these strategies don’t work? Members and investors can only suffer pain for so long before disillusionment sets in and faith is lost.

We are concerned that the industry is placing itself in a vulnerable position from a trust perspective. A better approach might be to foster understanding that pursuing higher returns is a sensible strategy that brings prospects for better outcomes, but markets are risky and there are no guarantees.

Most investors have experienced the greatest asset bull market in history during which markets have always recovered to push to new highs within a reasonable period of time. It would be healthy to recognise that it does not always have to be thus.

David Bell is the Executive Director of the Conexus Institute. Geoff Warren is a Research Fellow at the Conexus Institute and an Honorary Associate Professor at the Australian National University. This article is based on Conexus Institute research summarised here.