Warren Buffett and his former offsider Charlie Munger are treated like investing royalty, and rightly so. Yet, their success also makes them valuable marketing tools. For journalists looking for headline clickbait. For fund managers looking to bask in their wisdom and afterglow. And likewise for CEOs.

It’s a newer trend which disturbs me more. That is, of growth investors selectively quoting Buffett and Munger to justify their purchases of ‘wonderful’ businesses, or compounders.

Invariably, the story is told of how Munger turned Buffett from a Ben Graham-type value investor into a growth investor. It’s supported by quotes from Buffett like these:

“It’s far better to buy a wonderful company at a fair price, than a fair company at a wonderful price.”

“If a business does well, the stock eventually follows.”

“Only buy something that you’d be perfectly happy to hold if that market shut down for 10 years.”

As well as by quotes from Munger like this:

"Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return—even if you originally buy it at a huge discount.”

Growth investors are rightly basking in a golden era where their style of investing has crushed indices. Since the GFC, growth investing has reined supreme, while the likes of value have been pulverised. Fast growing companies such as the ‘Magnificent Seven’ in the US, and Cochlear, Pro Medicus, and Technology One in Australia have delivered incredible returns for shareholders.

Yet the past isn’t the future, and one key component of Buffett and Munger’s investing is increasingly being ignored: that buying stocks at the right price matters too.

Here’s Buffett on the topic:

“Price is what you pay. Value is what you get.”

“For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favourable business developments.”

“The three most important words in investing are margin of safety.”

“Most people get interested in stocks when everybody else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.”

And here’s Munger:

“You’re looking for a mispriced gamble. That’s what investing is. And you have to know enough to know whether the gamble is mispriced. That’s value investing.”

The growth mantra

Let’s look at an example of what I’ll call the ‘growth investing mantra’. Last week, Rudi Filapek-Vandyck wrote an article for Firstlinks on the virtues of buying wonderful businesses like CBA. Rudi is a quality thinker and writer, though I respectfully disagree with some of his conclusions.

In the article, Rudi suggests that the reason that US markets have crushed Australia’s since the GFC is because they have a greater number of high-quality businesses. That’s undoubtedly correct.

He goes on to say that Australia still has some quality growth stocks. He compares CBA to the rest of the major banks. Over the past 20 years, NAB has delivered minimal returns, ex dividends.

Source: Morningstar

Westpac has done a bit better. From the bottom of the GFC, it’s risen 4.7% per annum. Including dividends and franking, brings that return up to 9-10%. Yet, most other timeframes other than from the bottom of the GFC would have delivered little in returns for investors.

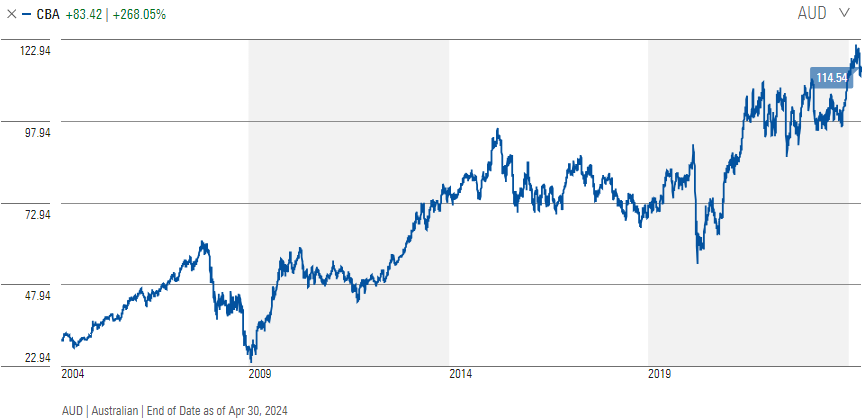

Compare that to CBA. From March 2009, it’s returned 22% per annum, ex dividends.

Source: Morningstar

It’s quite the contrast. And what accounts for the very different returns from CBA versus the other banks? According to Rudi, it’s the quality of CBA compared to the rest. And he says that CBA has been the most expensive bank throughout that 16-year period, and it’s still delivered the best returns. The lesson? Buy the best companies.

What’s missing?

What he doesn’t mention though is that earnings growth for CBA has been mediocre since the GFC. Diluted earnings per share (EPS) was 313.4 cents in 2009, and that went up to 601.4 cents last financial year. That’s an EPS compound annual growth rate of 4.4%. If we reduce the timeframe from 15 years to the last decade, EPS has compounded at an annual rate of 2.32%.

In other words, the bulk of the fantastic returns of CBA over the past 15 years has come from multiple expansion – the multiple that investors have been willing to pay for those CBA earnings.

When CBA bottomed in March 2009, it traded under $25. Then, the price-to-earnings ratio (PER) was around 8x 2009 earnings, or less than 7x 2008 earnings. The stock was dirt cheap at that stage.

Since then, the PER has risen to a peak above 20x in March this year, and it’s just under that now.

The upshot is that there is a vast difference in the valuation attached to CBA now versus 2009. Today, the shares trade for almost 3x the multiple they did back then. Your starting point today is that you’re paying almost 20x earnings for a stock growing EPS at 2% per annum.

CBA’s potential returns over the next decade

What can we expect for returns from CBA over the next 10 years? We can use a simple but useful formula:

Expected returns (nominal, annualized over the next 10 years) = Starting dividend yield + Earnings growth + percentage change (annualized) in the PER multiple.

CBA’s dividend yield is 3.78% and if we plug in 2.32% EPS growth, as it’s averaged over the past decade, that gets us to total annual returns of 6.01%.

Of course, earnings going forward are dependent on numerous things, and past earnings may not be indicative of future ones. I’d argue that the earnings assumption is probably realistic. The past decade has delivered an enormous housing boom that’s fuelled CBA’s loan book. Yet, it’s also suffered from poor margins due to low interest rates throughout much of the period. Costs have also spiked from increased technology spend and more recently, wages.

Looking ahead, margins should improve as rates stay higher, though that may be crimped by the increased competition for deposits from the likes of Macquarie. On the other hand, it’s harder to see the housing boom being replicated, and bad debts staying as low as they have been.

A big swing factor for returns will be whether CBA can retain its current PER multiple of ~20x. If it does, then shareholders can expect around that 6% in total return, provided my earnings assumption proves right. If the multiple is cut to 15x, and assuming the same earnings growth, then expected total annual returns would fall to just 3.8%.

Whether you use heroic or conservative earnings assumptions, the maths suggest that CBA won’t deliver anything but mediocre to poor returns over the next decade. And it’s principally because the current share price is exorbitant for a slow growing stock.

Other market darlings

With growth stories scarce in Australia, investors seem willing to pay up, and then some, for a select group of other stocks too. For instance, Cochlear is trading at a cool 46x next year’s earnings. That’s for a stock that’s grown EPS at 9% and 7% per annum over the past five and ten years respectively.

Source: Morningstar

Cochlear’s PER equates to an earnings yield of just 2.17% (earnings yield is the inverse of PER, or earnings divided by price). That earnings yield is under half the 10-year Australian government bond yield, or risk-free rate, of 4.5%. In other words, you can invest in a risk-free bond at more than 2x the yield that you’ll get from investing in Cochlear.

Cochlear is also trading at a steep premium to most of the Magnificent Seven tech stocks in the US, which are growing much more strongly. For example, Nvidia is trading on a forward PER of 36x, and Microsoft is at 29x.

On a lot of fronts, Cochlear’s pricing doesn’t make sense. And that will impact its future returns. If the PER drops from the current 46x to 30x, that will shave almost 5% per annum off total returns over a 10-year period. Investors will need very strong earnings growth over that period, or the multiple to stay near where it is now, for the stock to return anything close to the ASX 200 over that same period.

That also assumes that the business doesn’t trip up during that time, which is far from a sure thing.

James Gruber is an assistant editor at Firstlinks and Morningstar.com.au.