Former Treasurer Peter Costello recently published an opinion piece titled “We’ve wasted 20 years. It’s time to rebuild our great nation.” The timeframe he references coincides with the period since he left the Treasurer role following the 2007 election.

Notably, the article proposed little in the way of strategic fiscal reform beyond a call to reduce government expenditure as a share of GDP, reflecting the fiscal approach of the Howard Government (1996–2007).

It is true that by the end of that period the Howard Government had repaid the majority of the approximately $100 billion of debt inherited from the Keating Government. This outcome was achieved through a combination of reducing the relative size of the budget, selling public assets, and restraining public investment. By the conclusion of the Howard era, Commonwealth bonds on issue represented less than 10% of GDP, while remaining public assets exceeded debt.

This raises an important question considering Costello’s commentary: Did Australia begin losing economic momentum well before 2007 due to an excessive policy focus on balanced budgets and debt reduction?

How did Australia become “debt free”?

The Howard Government came to power in March 1996 and remained in office until December 2007. The fiscal trajectory over that period provides useful context.

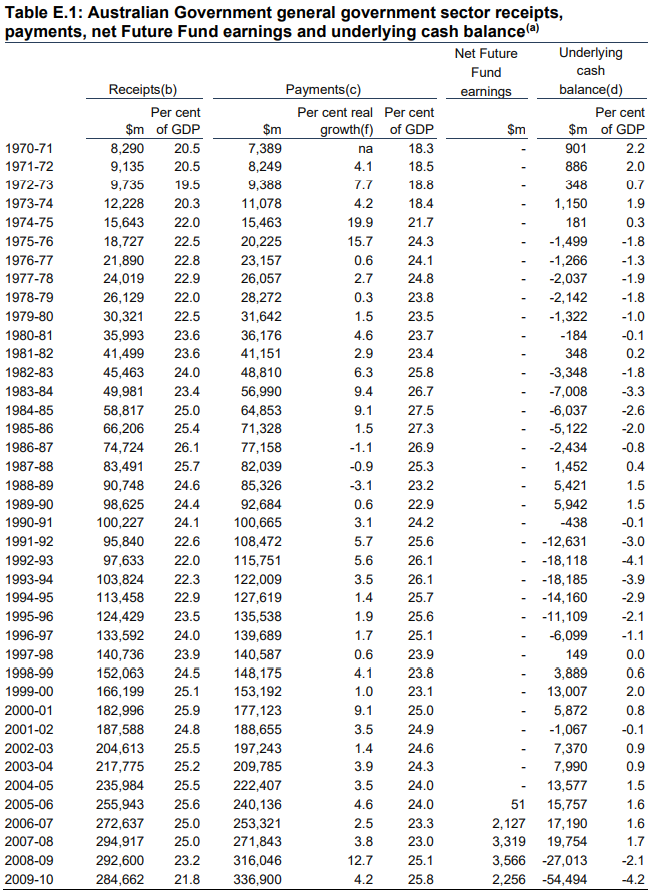

Source: budget.gov.au - Mid-Year Economic and Fiscal Outlook 2024–25, Appendix E: Historical Australian Government Data.

The first Costello budget was delivered in August 1996 (FY1997), following a Labor deficit under Treasurer Kim Beazley of $11.1 billion, or approximately 2.1% of GDP in FY1996.

At the time, Australia’s GDP was around $529 billion, and Commonwealth debt stood near $100 billion—less than 20% of GDP. By international standards this was not an elevated level of public debt. For comparison, US government debt in 1996 was approximately 64% of GDP.

Australia moved from a deficit of 2.1% of GDP in FY1996 to a surplus of roughly 2% by FY2000 as the economy recovered from the early-1990s recession. Productivity gains were supported by the adoption of computer and internet technologies that were spreading from the United States. Unemployment at that time remained around 6%.

Between FY1997 and FY2007, Costello delivered nine budget surpluses from eleven budgets, generating cumulative fiscal surpluses of approximately $77 billion.

During the same period:

- Australia’s GDP grew to approximately $1.1 trillion, representing nominal compound growth of around 6.5% per annum.

- Commonwealth asset sales totalled approximately $72 billion.

- The Future Fund was established with an initial seeding of $60 billion, including $9 billion of Telstra shares.

In effect, fiscal surpluses were largely used to repay Commonwealth debt, while asset sales provided the capital used to establish the Future Fund. The Fund was designed to meet defined-benefit public sector pension liabilities that were estimated at the time to be around $140 billion and now exceed $300 billion.

Is being debt free good public policy?

While a debt-free balance sheet is politically attractive, it is not necessarily sound economic policy if it prevents the use of public borrowing to finance productive investment for future generations.

A sustained reluctance to use government balance sheets for infrastructure investment can lead to delayed projects and higher long-term costs. Infrastructure built decades later is invariably more expensive due to compounding inflation and higher construction costs.

In several areas, Australia’s strategic infrastructure capacity has deteriorated.

For example:

- Domestic oil refining capacity has declined to roughly 10% of national liquid fuel needs and with the Iran War this has exposed our nation to a potential oil shock; and

- Energy generation and distribution has evolved into a fragmented public-private system with significant pricing and reliability challenges.

This raises the broader question: was eliminating public debt without a clear national investment strategy the optimal policy outcome?

Government debt as a structural feature

Historically, Commonwealth debt has been a normal feature of Australian economic management since the Great Depression. Every government over the past century has inherited some level of debt.

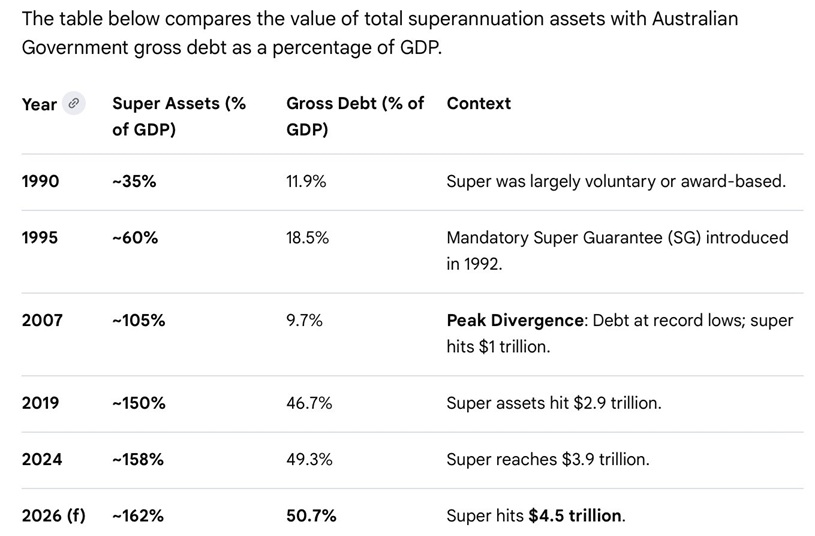

At the same time, Australia developed one of the largest pension savings systems in the world through compulsory superannuation.

However, the Commonwealth never created a meaningful infrastructure bond market to connect this growing domestic savings pool with national infrastructure investment. Instead, governments increasingly relied on asset sales—often attracting foreign pension capital—to reduce debt and fund infrastructure upgrades.

The consequence is that Australians now pay usage charges for assets that were once publicly owned, including airports, toll roads and electricity networks.

This outcome is particularly notable given the scale of domestic savings now available through superannuation.

Source: AI, ChatGPT

The missed opportunity of superannuation capital

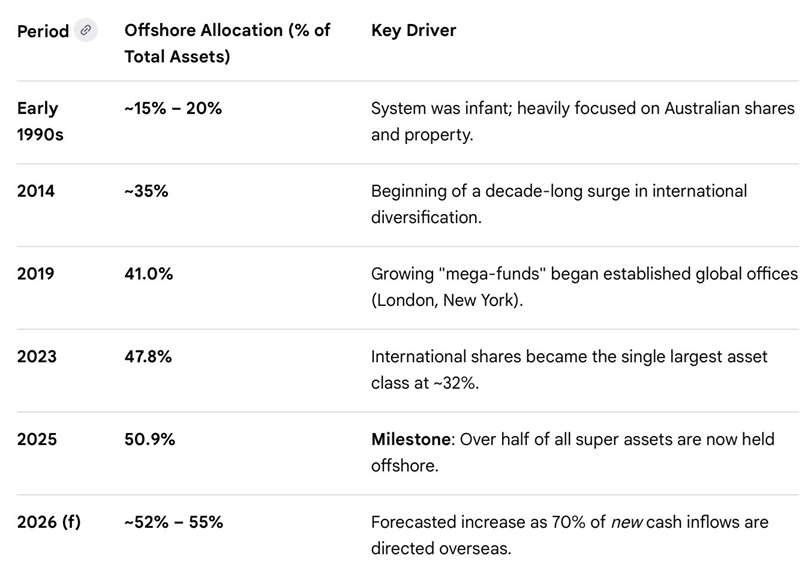

Australia’s superannuation system has grown into a multi-trillion-dollar pool of long-term capital. Yet much of that capital is invested offshore rather than deployed into domestic productivity-enhancing infrastructure.

Source: AI, ChatGPT

This represents a structural mismatch:

- Australia has abundant domestic savings.

- Australia also faces substantial infrastructure requirements.

- Yet policy settings have not effectively connected the two.

The result is that Australian retirement savings increasingly finance growth in foreign economies while domestic infrastructure investment remains constrained.

A simple example illustrates the opportunity cost. If Australia had financed major projects using domestic infrastructure bonds in the late 1990s—such as a dedicated rail link between Melbourne Airport and the CBD—the project cost would likely have been substantially lower than undertaking the same project three decades later.

The structural shift of the 1990s

The early 1990s recession was a defining period for Australia’s economic structure. Major banks and insurers faced technical insolvency and many highly leveraged property and industrial groups collapsed.

This environment created opportunities for international investment banks that entered Australia following financial deregulation in the 1980s and the emergence of large superannuation savings pools.

During this period:

- Mutual organisations and cooperatives were demutualised and privatised.

- Major Australian companies were taken private through leveraged buyouts.

- Stable companies were advised to restructure ‘lazy balance sheets’.

- Essential property assets were sold and leased back.

These activities were highly profitable for advisory firms but often transferred long-term value away from domestic balance sheets.

At the same time, government policy increasingly favoured asset privatisation. Major sales included:

- Commonwealth Bank (second tranche)

- Telstra

- Major airports

- Rail and freight assets

- Transmission spectrum

- Gold reserves

The result

Over time, these policy settings produced a structural outcome that is now increasingly visible.

Australia accumulated large private savings while simultaneously under-investing in national infrastructure and productive capacity.

The social consequences are also becoming evident.

Australia’s birth rate has been declining since the early 1990s—with only a brief interruption following the Costello ‘baby bonus’ in 2007. The long-term trend has continued downward.

Source: AI, ChatGPT

At the same time:

- Real wage growth has stagnated.

- Productivity growth has slowed.

- Younger generations face rising housing costs and declining economic security.

Policy responses have increasingly relied on higher immigration rather than addressing underlying productivity challenges.

Conclusion

The central issue raised by Costello’s commentary is not simply whether Australia has ‘wasted’ the past 20 years. The more substantive question is whether the policy framework established during the Howard–Costello era created structural weaknesses that are only now becoming visible.

The pursuit of minimal public debt became a dominant policy objective. Yet that objective was achieved through a combination of asset privatisation, reduced public investment and the failure to mobilise Australia’s growing superannuation capital toward national development.

The result was a paradoxical outcome: one of the world’s largest pools of long-term savings alongside persistent underinvestment in domestic infrastructure and productive capacity.

Rather than deploying debt strategically to fund national development, governments prioritised balance-sheet optics. The Future Fund itself illustrates this tension. While it was created to meet pension liabilities, its capital was not directed toward the type of infrastructure investment that could have expanded the productive base of the economy. It is not a true Sovereign Wealth Fund.

In retrospect, the question is not whether Australia eliminated debt, but whether the focus on doing so came at the expense of a broader national vision.

A strategy that combined moderate public borrowing, domestic superannuation capital and large-scale infrastructure investment may have produced a different outcome: higher productivity, stronger wage growth, and greater economic resilience.

The legacy of the past 30 years suggests that fiscal prudence alone is not sufficient. Without a coherent national investment strategy, a nation can maintain strong balance sheets while gradually eroding the foundations of long-term prosperity.

John Abernethy is Founder and Chairman of Clime Investment Management Limited, a sponsor of Firstlinks. The information contained in this article is of a general nature only. The author has not taken into account the goals, objectives, or personal circumstances of any person (and is current as at the date of publishing).

For more articles and papers from Clime, click here.