The following is an abridged version of Ashley Owen’s monthly snapshot. You can read the full version here.

Here’s my quick wrap-up on global markets for serious long-term Aussie investors – including shares markets, interest rates, inflation, bonds, currencies, commodities, and more, including portfolio implications.

Key points:

- Share markets around the world rebounded in April after a very brief war / inflation scare in March, but the ASX remains a global laggard.

- Investors have two positives to support their bullishness. The first is hope that Trump retreats (dressed up as an epic ‘win’ of course) because his most urgent goal is to get fuel prices down in order to retain MAGA voters in the November mid-term elections.

- The second positive is strong US profits, thanks to tech / ai, and the bonanza for fossil fuel producers like the US.

- The war continues, but is increasingly looking like a stalemate, probably with higher energy prices and inflation for a while yet. Rate cuts or rate hikes?

- Share markets everywhere (not just US tech) are still vastly over-priced on numerous measures – including and especially in Australia. A major global correction is due.

- Bond markets posted more losses again as yields kept rising in expectation of higher inflation and interest rates ahead.

- The AUD rose and US dollar fell with the share rebound, as per the usual pattern in global panics / rebounds.

- Commodities prices mostly rebounded in April, benefiting ASX resource stocks.

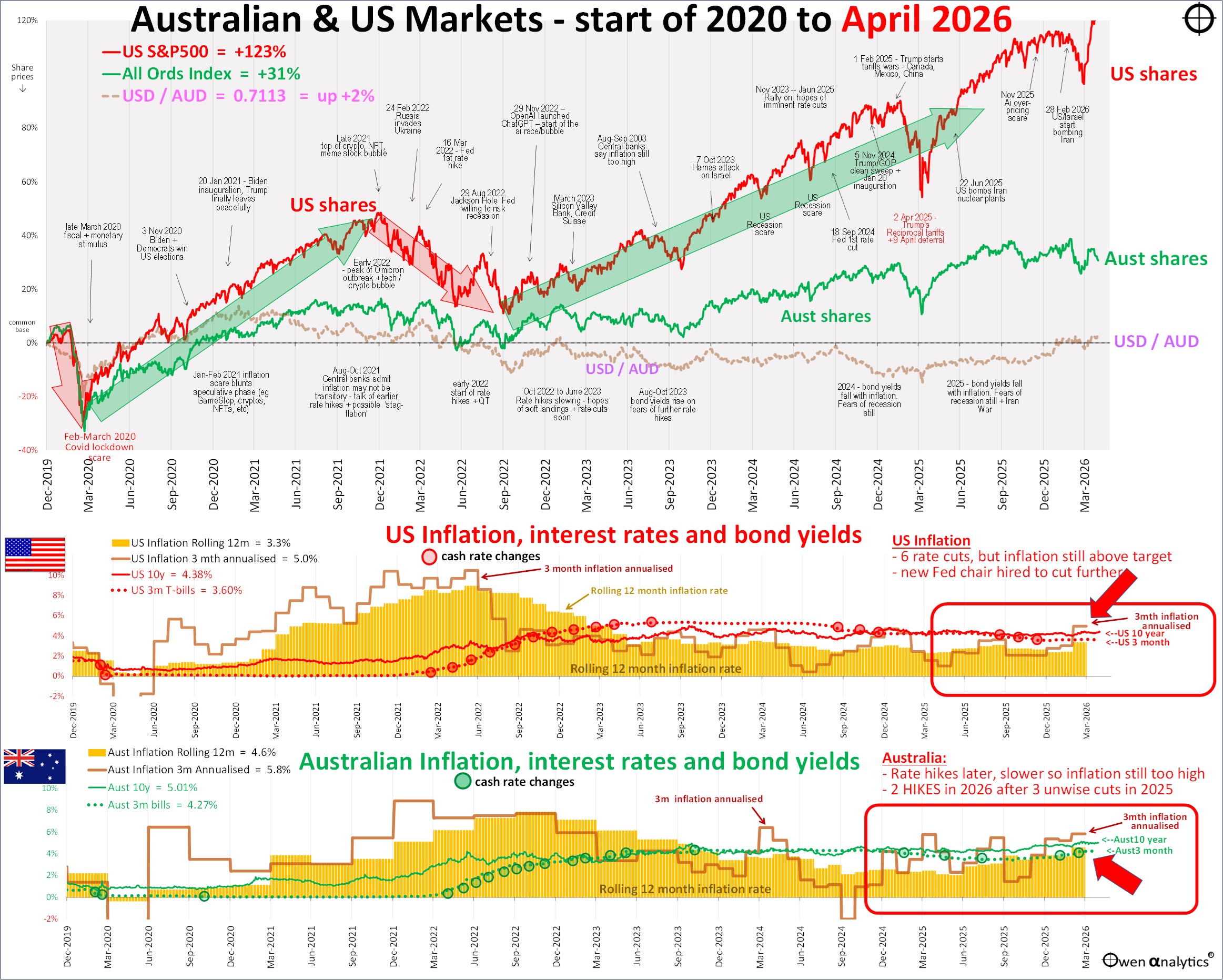

But first - my essential 1-page snapshot chart - covering Australian and US share markets, short and long-term interest rates, inflation, and the AUD/USD exchange rate. It is my go-to chart that tells me what happened when and why, whenever answering queries from advisers, investors, doing webinars, market updates, etc.

Click to enlarge

Not only does this have all the detail I need to answer investor questions from advisers, but even from the back of the room you can easily see the big picture on where we are for share markets, currency, inflation, long & short interest rates.

I will get into shares in a moment, but from the back of the room you can see that share markets had a minor hiccup in March (top right corner of the chart – red for US, green for ASX), but are back on track in April.

Bottom line – if you were rattled by the volatility and price falls in March then you ain’t seen nothin’ yet! (or you are too young to remember what a decent sell-off looks and feels like!)

Share markets

Global share markets rebounded in April after the brief sell-off in March when panicking investors sold down just about everything except for oil/gas stocks profiting from higher prices with the Strait of Hormuz closed.

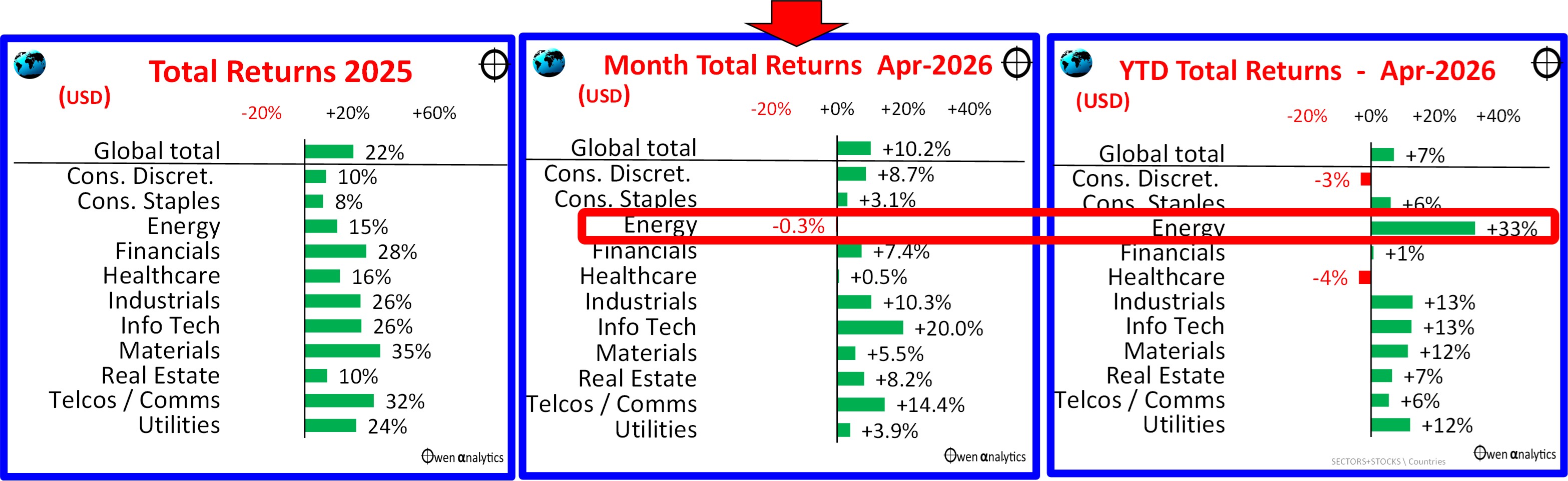

The next charts show total returns from global industry sectors for April 2026 (middle chart), calendar year to date (right), compared to 2025 (left chart):

Click to enlarge

The stand-out sector up is fossil fuels (‘energy’) – with across-the-board double-digit rises in the major stocks as they profit most from the global supply squeeze.

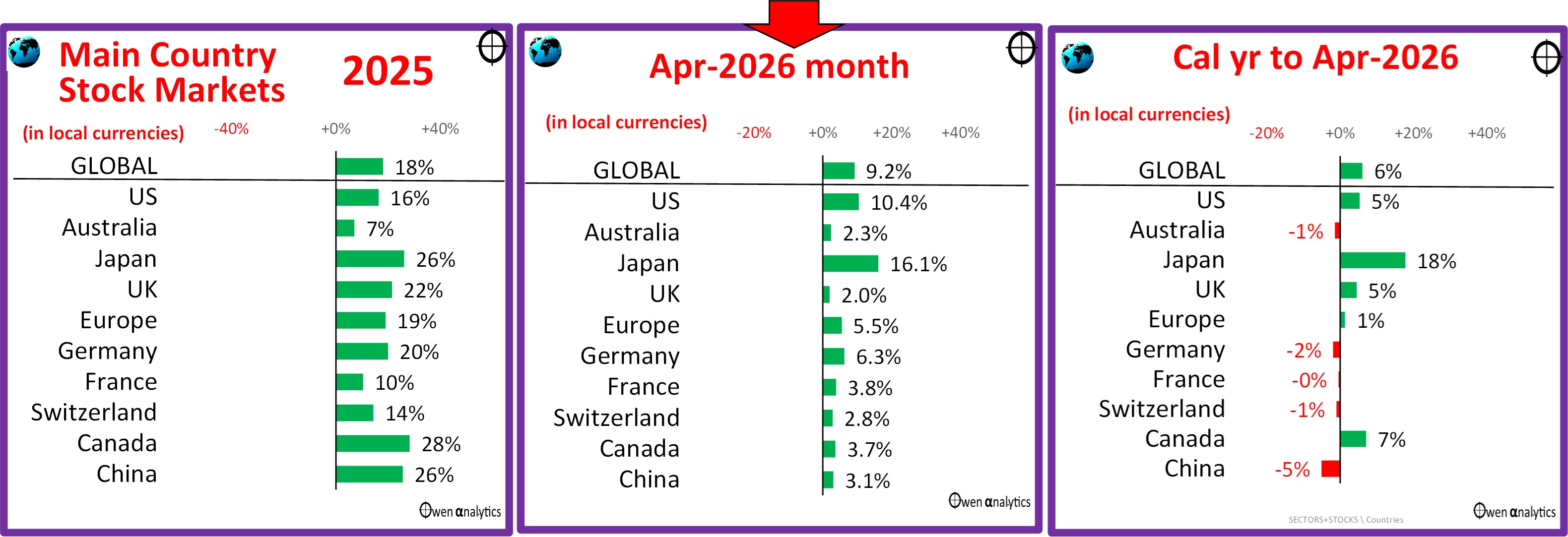

Major country share markets

Share markets almost everywhere had a great month in April. Here are the main markets:

Click to enlarge

Best of the major markets has been Japan, led by Softbank (big Facebook holding plus other US tech bets), Keyence (robotics), and Shin-Etsu Chemical (plus assisted by weaker yen). Next best was the US (tech/ai giants).

So far in 2026 global share markets are ahead by 6% (in local currency terms). This may make it a fourth good year in a row in the current boom, following three very strong years averaging +20% per year in 2023, 2024 and 2025.

Share markets everywhere (not just US tech/ai stocks) are still vastly over-priced on a variety of measures – including and especially in Australia, and we are well and truly due for a global correction. Refer to the above reports on share market pricing.

Inflation & interest rates

A stalemate in the US/Iran looking like a reasonably likely outcome would mean above-target inflation lasting longer (after short-term rises).

Despite inflation remaining sticky around the world, central banks have mainly held cash rates flat this year – taking a middle road between further rate HIKES to reduce spending and inflation, versus rate CUTS to stimulate slowing economies due to higher prices. In the US, Jerome Powell had his final meeting as Chair of the US Fed rate-setting board, which voted to keep rates flat.

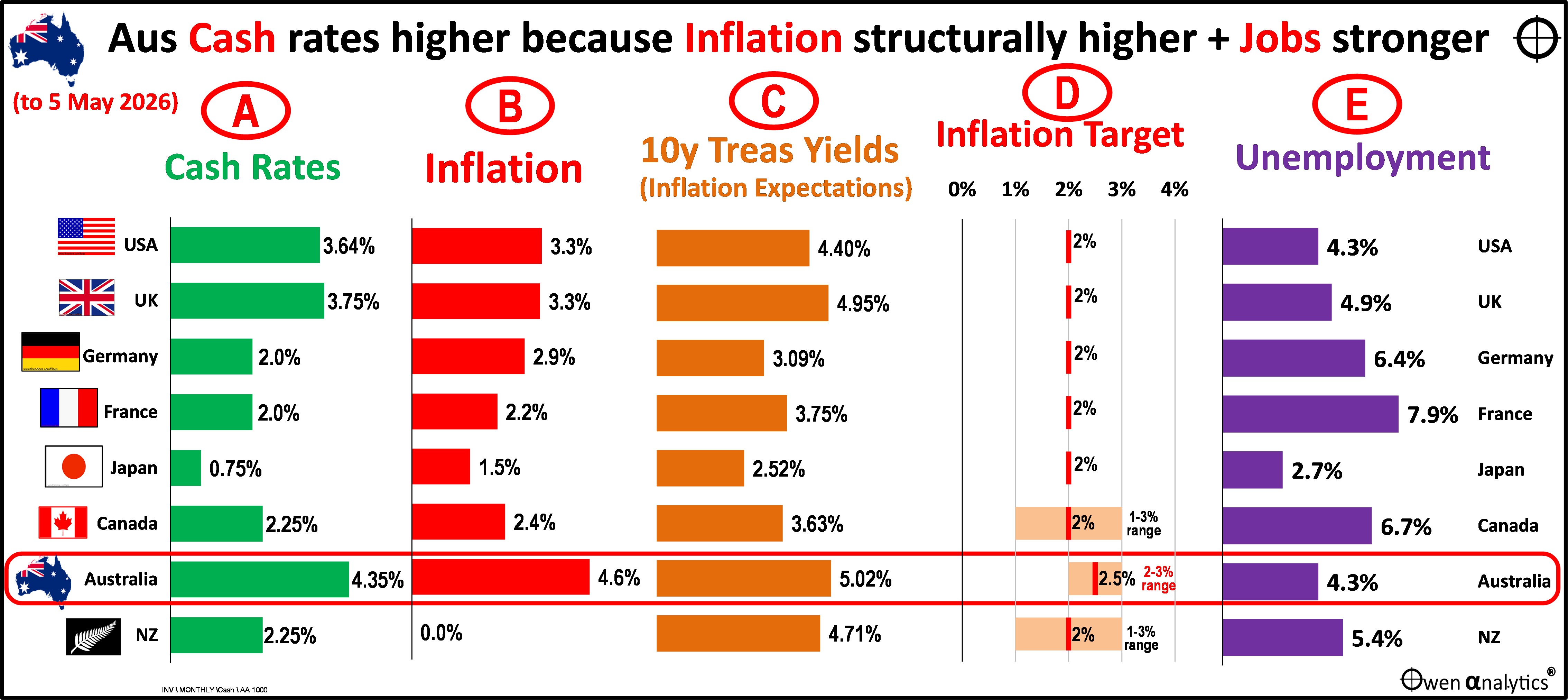

Australia is the exception of course. The RBA has been the only central bank in the world to switch from rate cuts after the 2021-23 inflation surge, back to rate HIKES – with three hikes so far this year (February, March and May).

Even before the latest war on Iran, Australia already had the HIGHEST cash rate amongst its peers – because we have the highest inflation, the highest inflation expectations (treasury yields), the loosest/highest inflation target, and the lowest unemployment rate among our peers.

Click to enlarge

It now remains to be seen how expansionary / inflationary the upcoming May Federal Budget actually is. (The budget will range somewhere between ‘highly expansionary / inflationary’ and ‘ridiculously expansionary / inflationary’). Apologies once again to my kids and future grandkids who will be paying for this chronic fiscal diarrhoea through higher interest rates and taxes for the rest of their lives.

Either way, more rate hikes are on the way if inflation is to be returned to target range.

Trump’s agenda?

The following is what I said in my end of March report:

The most important factor for the direction of short-term investment markets prices will be Trump’s twists and turns on the war front (or tariff front, or any of his other hobby horses du jour). Not even Trump knows what he will say or do one minute to the next, so it is pointless trying to guess.

However, I have two fairly sound reasons for being relatively positive for share markets in the coming months.

First - Trump probably has one central aim in the short term: to retain MAGA votes in the November mid-term elections. To do that he must (1) get oil prices down, and (2) minimise the number of Americans coming back in body bags.

This points to a relatively quick end to the war. Or at least an end to disruptions in oil/gas supplies, which means opening the Strait of Hormuz to restore normal shipping.

Second – in the event of a sharp economic recession, governments of all flavours in the US, Australia and just about everywhere else no longer have any notion of fiscal discipline. They have shown in the GFC and Covid that they will literally throw ‘free’ money at anything and everything in order to retain populist votes. Politicians no longer have the stomach nor the intellectual framework for ‘tough medicine’, ‘business cases’, trade-offs, or discipline.

The longer-term consequences and downsides will be even higher debts and widening intergenerational inequity, but it supports asset prices in the short-medium term. The current global tech/everything boom is being held up by hopes of endless monetary and fiscal profligacy.

This theory remains my Base Case scenario. Trump is desperate to get out but it must be with him ‘winning’. The problem is finding something to call a ‘win’. He is now reduced to a rather tiresome tirade of threats, then backdowns, then mysterious alleged ‘negotiations’ with nameless parties on behalf of Iran about a so-called ‘deal’, then more threats, and more back-downs.

The most likely outcome is probably yet another humiliating US withdrawal dressed up as a ‘win’, but leaving a festering mess behind.

Ashley Owen, CFA is Founder and Principal of OwenAnalytics. Ashley is a well-known Australian market commentator with over 40 years’ experience. This article is for general information purposes only and does not consider the circumstances of any individual. You can subscribe to OwenAnalytics Newsletter here.