As the budget fallout continues, Jim Chalmers gave the following reply to a post-budget question asking if the top marginal tax rate comes in at a salary that is too low:

“First of all, we have increased the top threshold in the tax system, we did that a couple of budgets ago. Secondly, we do understand how important it is that bracket creep be returned, and that’s why we’ve done it 5 times in 3 different ways. We’ve increased the threshold, we’ve cut the rates, we’ve provided tax relief via a standard deduction, and now we’re providing tax relief via a Working Australian Tax Offset.”

The “five” tax cuts he was referring to were:

1. The Labor redesigned Stage 3 tax cuts from July 2024

- Included rate cuts and threshold changes.

- This was a modified Coalition Stage 3 tax cuts package. Changes:

- proposed 30%: $45,000 to $200,000

- became 30%: $45,000 to $135,000 and 37%: $135,000 to $190,000.

- lowest marginal rate cut from 19% to 16%.

- The “we have increased the top threshold”, which was from $180,000 to $190,000, was actually a decrease from the proposed Coalition $200,000.

2. A cut from July 2026

- 16% marginal rate to 15%. A maximum tax cut of $268 per annum.

- Announced in the 2025-26 budget.

3. A further cut from July 2027

- 15% marginal rate to 14%. A maximum tax cut of $268 per annum.

- Announced in the 2025-26 budget.

4. The $250 Working Australians Tax Offset (WATO)

- Begins 2027–28.

- Announced in the 2026-27 budget.

- A fixed offset, it is worth more to lower earners and its value erodes over time.

5. A $1,000 instant deduction for work-related expenses (announced in the 2026-27 Budget)

- Up from $300.

- Chalmers explicitly included this as an income tax cut mechanism.

- A bit of a stretch counting this as a tax cut when it is really a simplification or admin measure which may benefit some taxpayers but not all.

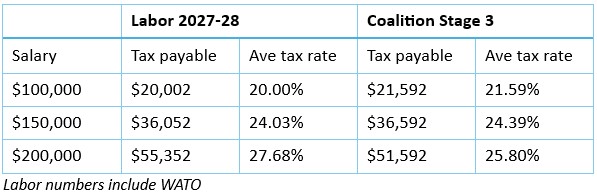

Including all announced Labor changes up to 2027-28, the following table compares average tax rates at selected salary levels, with what they would have been under the Coalition’s Stage 3 changes.

Note that under Labor, even after the “five” tax cuts, average tax rates are no better to worse than the Coalition for mid to high income earners. Lower income earners fare better with the Labor Stage 3 redesign which effectively redistributed high income tax cuts to lower incomes. Not forgetting that the Coalition had favoured lower incomes in its Stages 1 & 2 tax cuts, bringing the $100,000 average tax rate down from 24.50% to 22.97%.

The latest Labor tax cut in the form of the permanent $250 WATO goes some way towards winding back bracket creep since the Stage 3 tax cuts, but it is likely to be swamped by additional tax collected from nominal wage growth, even before it actually commences.

Bracket creep occurs when workers see an increase in their average tax rate because of nominal wage growth, regardless of real wage growth.

For example, consider a wage earner on $100,000. Current tax excluding the Medicare levy is $20,788, for an average tax rate of 20.79%. If their wages kept pace with inflation at say 3%, rising to $103,000, tax payable becomes $21,688, or 21.05%. The average rate has increased because a greater proportion of the earner’s salary is in the higher tax bracket.

Had the average tax rate not jumped, tax on the $103,000 would be $276 less, which is more than one year’s WATO. For a salary going from $200,000 to $206,000, the equivalent increase in tax burden would be $1,016, or more than four years’ WATO.

This prompts the question as to how effective tax relief in the form of offsets and irregular rate cuts compares to permanent protection against bracket creep, as proposed by the Coalition in its budget reply. It would do this by indexing tax brackets to the Consumer Price Index should it win government at the next election.

Continuing with the above example under an indexation model. The $18,200 tax free threshold would rise 3% to $18,746. The next threshold at $45,000 would increase to $46,350, and so on with the higher thresholds. Calculating tax payable according to the indexed thresholds:

16% x ($46,350 - $18,746) + 30% x ($103,000 - $46,350) = $21,412

(an average rate of 20.79% and unchanged from the average when salary was $100,000 a year prior)

That is, a system that indexes tax brackets protects workers from increased tax on nominal wage growth due to inflation.

This example also highlights the fact that bracket creep is broader than simply moving into a higher tax bracket because of increasing wages, which might be referred to as ‘inter-bracket creep’. Because it also includes the increase in tax burden when the taxpayer moves deeper into the same marginal tax bracket, or ‘intra-bracket creep’. The taxpayer is ‘creeping’ through the bracket.

Features that emerge from a tax schedule indexed to inflation include:

- If wage growth = threshold indexation rate, there is no bracket creep as average tax rates remain the same. You would always remain in the same marginal tax bracket.

- If wage growth > threshold indexation rate, there is real wage growth, average tax rates rise, and movement into a higher tax bracket is possible.

- If wage growth < threshold indexation rate, real wages retreat, average tax rates decline, and movement into a lower a tax bracket is possible. Could we call this ‘bracket retreat’?

Therefore even with an indexed tax scale system, progressivity remains if real wage growth is positive. And under a Coalition model, bracket creep would reflect real wage growth, not nominal wage growth. That would be ‘real tax creep’.

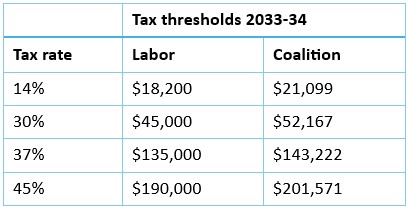

The Coalition indexation policy more specifically, would begin indexing the two lowest tax brackets to inflation from 2028-29, and the top two brackets from 2031-32. It would be instructive then to consider what happens over time with and without indexation, to thresholds and average tax rates.

We first compare what the Coalition’s indexed thresholds in 2033-34 would be, five years after the commencement of indexation, with Labor’s 2027-28 thresholds which are assumed to remain unchanged. Assuming indexation at an inflation rate of 3% p.a. would yield:

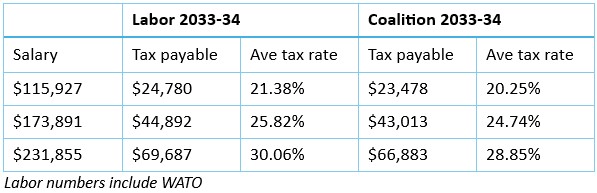

Now consider the same three salaries from Table 1, assuming 3% p.a. salary increases in the five years to 2033-34. Tax payable and average tax rates under Labor and the Coalition in 2033-34 would be:

This exercise isolates the effect of bracket creep driven by inflation. It shows that while Labor average tax rates rise from their 2027-28 levels in Table 1, Coalition average tax rates remain broadly stable. In fact, with wage growth in line with inflation, Coalition rates would be equal to the Labor average tax rates in Table 1 if Labor’s rates didn’t include WATO, and if the introduction of the Coalition policy wasn’t staggered.

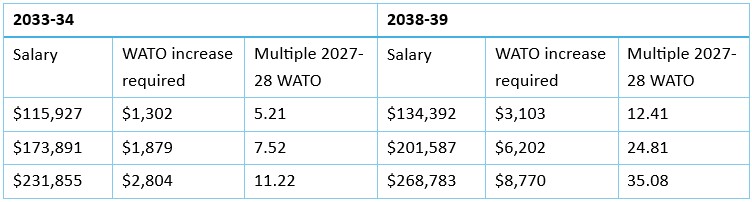

If WATO remains fixed at $250, it will offset a fraction of the increased tax burden arising from bracket creep.

By 2033-34, WATO[1] would need to increase by $1,302, $1,879, and $2,804 respectively for the three salaries (being the difference between Labor and Coalition tax payable in Table 3), to reduce Labor average rates to the Coalition levels.

And extending the exercise under the same assumptions for a further five years to 2038-39, the WATO[1] increase required to match Coalition policy would be $3,103, $6,202, and $8,770 respectively for the three salaries analysed. These amounts represent many multiples of the current $250 on offer.

Granted that while in office, Labor may return some bracket creep with more tax cuts or by increasing WATO, this analysis demonstrates that the effects of bracket creep can be profound.

Meanwhile the discussion should focus less on the number and format of “tax cuts” made to date, and more on whether taxpayers are being adequately compensated for bracket creep over time.

1 Increase in WATO required to neutralise inflation-induced bracket creep based on Labor 2027-28 tax settings.

Tony Dillon is a freelance writer and former actuary. This article is general information and does not consider the circumstances of any investor.