For decades, the investment community operated under a comfortable assumption. By blending a dominant share of growth assets with a fixed sleeve of government bonds, diversification was expected to automatically smooth out market turbulence. It was a beautifully simple framework, rooted in the predictable inverse relationship between corporate profitability and sovereign debt.

That framework rested on negligible inflation, low rates and predictable central bank liquidity. Those pillars have cracked. We now face a more volatile regime of persistent price pressures, aggressive fiscal spending and geopolitical flare-ups. Markets were used to worrying about demand shocks; today’s world is filled with supply shocks, which is an entirely different regime.

In this environment, traditional asset correlations can break down precisely when market stress peaks. Nowhere is this vulnerability more apparent than in the rigid implementation of portfolio hedges.

Many investors still treat risk mitigation as a set-and-forget defensive bucket. They allocate to a safe haven – whether long-duration treasuries, defensive currencies or gold – and trust it will work whenever equities fall. But when macro regimes shift, yesterday’s reliable hedge can quickly become tomorrow’s concentrated risk asset. Managing downside risk must be treated as an active process that moves with markets.

The trap of the static hedge

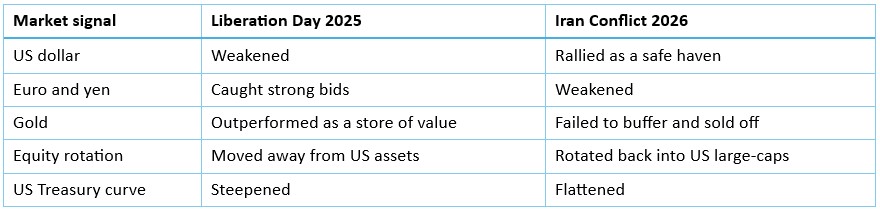

The danger of passive risk mitigation becomes clear when analysing how different geopolitical disruptions reverberate through markets. Investors who blindly apply the lessons of one crisis to the next can face severe capital impairment. The contrast between Liberation Day in 2025 and the Iran Conflict of 2026 is instructive.

Liberation Day 2025: The sell America trade

In 2025, asset prices moved with the belief that the uncertainty of a Trump presidency would lead to a wholesale reduction in US assets. The US dollar weakened, the euro and yen rallied, gold outperformed as a store of value, capital rotated into international equities, and the US Treasury yield curve steepened.

This rewarded portfolios that relied on precious metals and unhedged global currency allocations for protection. Long-duration bonds, however, became the risk asset.

Iran Conflict 2026: The playbook flips

When geopolitical tensions escalated into open conflict in Iran the following year, the same playbook hurt portfolios. The US dollar rallied, the euro and yen weakened, gold sold off, liquidity rotated back into US large-caps, and the Treasury curve flattened rather than steepened.

This divergence shows that a defensive position is only effective if it matches the structural drivers of the current crisis. Gold behaves well in a monetary debasement environment. Broad commodity baskets excel during acute supply-side shocks. Maintaining a static hedge out of habit means accepting uncompensated exposure.

Navigating bonds, commodities and FX

Portfolios cannot be managed in isolated, rigid sleeves. A more useful approach is to assess how the whole portfolio behaves when confronted by shifting liquidity, changing yields and geopolitical events.

The gold-to-commodity pivot

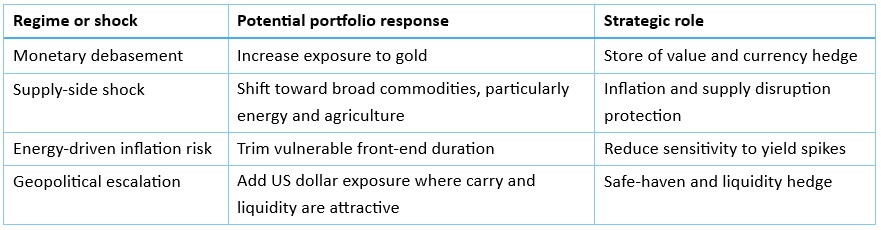

Consider the gold-to-commodity pivot. Early in the year, enthusiasm for precious metals had become immense as gold prices surged toward historic highs. Recognising that the asset was approaching a near-term ceiling, an active portfolio could crystallise gains, reduce gold exposure and reallocate into broad commodities, particularly energy and agriculture.

When the Strait of Hormuz was shut down, that pivot made sense because a supply-chain blockade is a direct supply shock that feeds commodity prices while placing short-term liquidity pressure on gold.

As immediate constraints ease, the logic can shift again. Gold may face short-term headwinds while shipping routes are under pressure, but its long-term structural tailwinds remain strong. Navigating these waves demands agility, not a passive buy-and-hold mentality.

Dynamic hedging in practice

Tactical duration and curve steepening

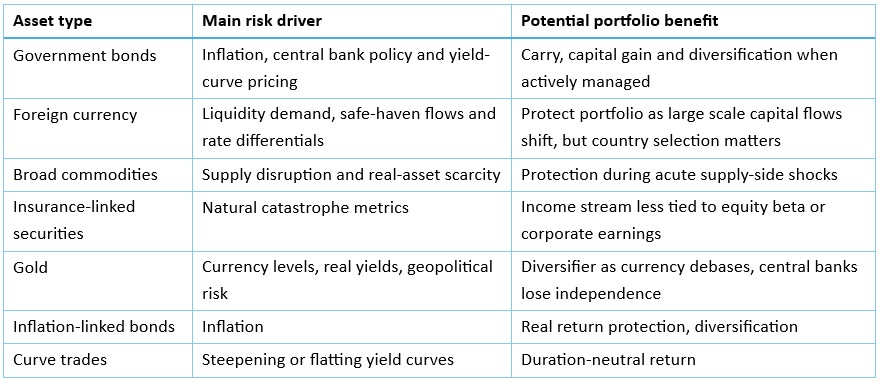

Government bonds are the ultimate casualty of a set-and-forget mindset. Treating duration as a permanent defensive anchor is dangerous when supply shocks pull yields and equity risks in the same direction. Since COVID-19, bonds have often failed to diversify equity risk.

That does not render bonds obsolete. Actively managed, they still provide carry, capital gain and diversification. The fixed income playbook needs to shift from broad macro bets toward more localised curve positioning.

When an energy shock breaks out, bonds may initially rally as markets move risk-off. That rally can be used to readjust positioning, particularly where oil supply shocks are likely to push inflation higher. Trimming front-end duration can be defensive, not merely return seeking. The key is not to abandon duration, but to recognise that its role changes as inflation, central bank pricing and geopolitical risk change.

The US dollar as a positive carry hedge

Front-end bonds also affect currencies. If a geopolitical crisis escalates, long US dollar exposure can benefit from safe-haven flows and oil-exporter dynamics, helping offset fixed-income drawdowns. Pairing curve exposure with an FX overlay can create a more coordinated defensive shield.

Despite last year’s ‘Sell America’ narrative, the US dollar provided its traditional safe-haven properties during the Iran crisis. When trade breaks down or goods and commodities must be purchased urgently, the dollar is one of the few currencies that can handle it.

Expanding the toolkit

Dynamic risk management also requires looking beyond standard sovereign bonds and currencies. Relying on high-yield credit or convertible bonds to lift income can expose investors to drawdowns when growth slows or corporate balance sheets weaken.

Insurance-linked securities, or catastrophe bonds, are one example of a less conventional diversifier. Their performance is tied to natural catastrophe metrics rather than corporate cash flows, interest rates or equity benchmarks.

Assets that offer an insulated income stream while decoupling from equity beta are examples of how modern diversified portfolios should be built.

Broadening the diversification toolkit

Portfolios must adapt

Expecting a single static asset class to perform an unvarying task - relying on equities for returns and standard bonds or gold for permanent cover - is an outdated luxury. The post-GFC period of zero inflation and unconditional central bank support was a historical anomaly, not the default setting.

Portfolio construction must be engineered around this reality: preserving purchasing power and growing real wealth by dynamically shifting exposure across growth, defensive and alternative roles. Investors should not trade for the sake of turnover. They should adjust because the distribution of macro risks changes rapidly, with even faster shifts in market pricing. To protect capital in this regime, staying static is no longer viable. Investors need the flexibility to scour the full asset horizon, and the conviction to choose their hedges wisely.

Sebastian is Head of Multi-Asset & Fixed Income at Schroders Australia, a sponsor of Firstlinks. This document is issued by Schroder Investment Management Australia Limited (ABN 22 000 443 274, AFSL 226473) (Schroders). This document does not contain and should not be taken as containing any financial product advice or financial product recommendations. It does not take into consideration your objectives, financial situation or needs.

For more articles and papers from Schroders, click here.