I like to consider myself relatively fearless. Sharks and snakes aside, a little market volatility never hurt anyone, nor do the headlines that periodically declare the end of capitalism as we know it.

I’m also a ‘passive’ investor by temperament. A few broad-based index funds, a modest satellite allocation here and there. It’s the approach I settled on after a few years of underperforming the market by picking individual companies.

A few months ago, I was sitting at an investment convention, as engaged as one can be after a long day of conference-hall haze. The panelists were deep in discussion on Australian equities while I was nursing a lukewarm coffee. Then one speaker said something that snapped me out of my stupor.

Almost a third of the ASX is a cyclical bet on Chinese demand and our second biggest company is an exploit of intergenerational inequity, acting as the intermediary between those who have capital and those who need it.

It was the kind of observation that everyone is vaguely, almost unconsciously aware of, yet we rarely hear articulated so plainly. Of course, we know not to take these words as gospel (and I have my own reservations about the recent enthusiasm for the term ‘intergenerational inequity’), but I can appreciate the blunt framing.

Many passive investors like to imagine we’ve opted out of stock-picking, that we’ve somehow been absolved of that responsibility. But every index represents a set of active decisions about which risks to accept, which sectors to overweight and ultimately, which narratives to believe.

A growing tension

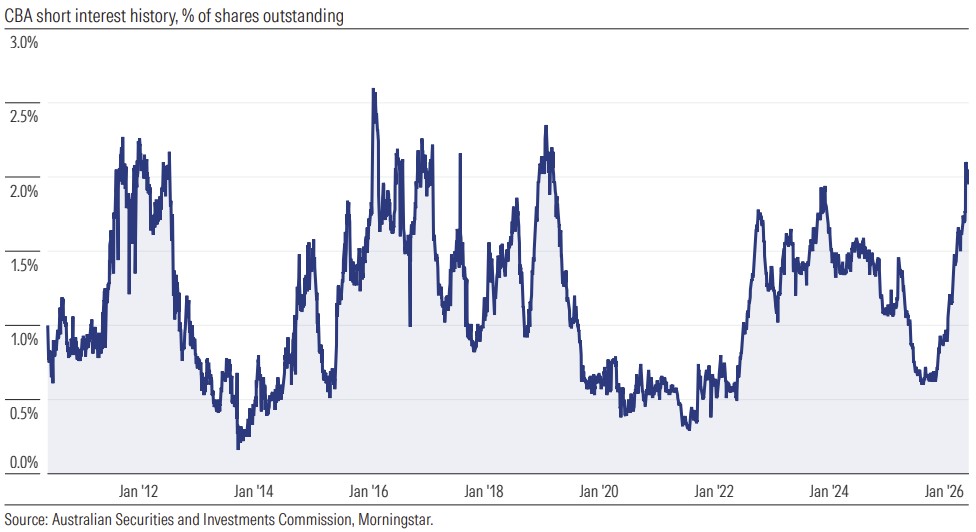

Concerns about the increasing concentration of the ASX are not new, however the current dynamics reveal a more notable conflict. On one side, several hedge funds are positioning against the major banks citing a mix of macro weakness, stalling property prices and declining credit growth. On the other hand, passive flows have been driving capital into the largest, most richly valued companies, essentially reinforcing the dominance of the same names. The market has effectively split.

Over the past decade, Australia’s market valuation has expanded meaningfully, yet earnings growth has been modest. The US has delivered robust growth driven by technology and productivity gains. By contrast, the ASX has leaned heavily on commodity cycles and the near-mythic stability of residential mortgages.

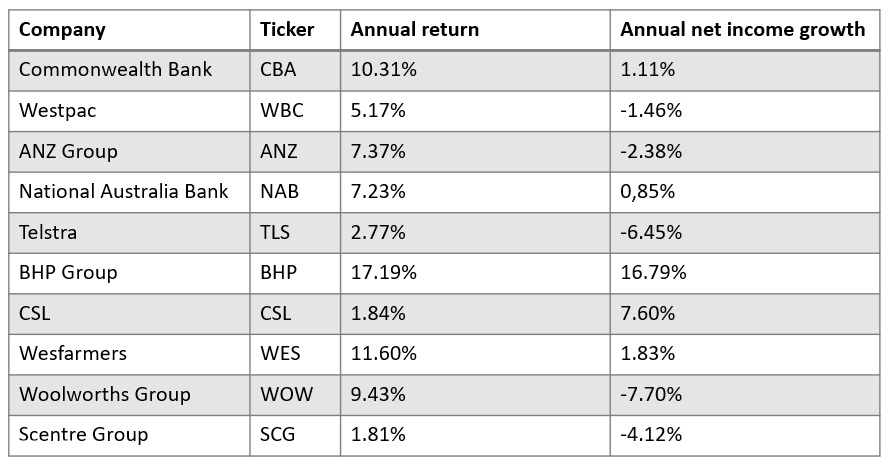

Performance of the Ten Largest ASX Companies in 2016, Annual Returns and Net Income Growth Over the Past Decade.

Source: Australian shares are falling behind the world.

Theoretically, when key drivers of economic growth such as housing begin to slow, earnings should eventually slow with them. Yet we haven't seen prices adjust in the same way. I think we’re well past the point where passive investing can be described as merely reflecting the market. There is a credible argument that it now shapes the market. Even the idea that ‘the market’ is a neutral arbiter of value, becomes less convincing when a large portion of flows are valuation-agnostic.

For some investors, this dislocation represents an immovable object. Perhaps a structural feature of modern markets that must simply be accepted. For others, the widening gap between fundamentals and index-driven pricing may present opportunity.

Where to from here?

For many investors, the ASX has been a faithful companion for decades. The banks, miners and the industrials that dominate the index have delivered income, stability and a sense of familiarity. But the country is shifting. The slow reshaping of Australia’s economic foundations has forced many to lift their gaze.

What is harder to ignore is the growing influence of passive flows in setting the prices of the heavy-weights. When money pours into index funds irrespective of valuation, fundamentals inevitably appear to play a smaller role. As a 'passive' investor myself, I find this dynamic increasingly difficult to dismiss.

Simonelle Mody

Also in this week's edition...

Treasury has confirmed the tax exemption for discretionary testamentary trusts. Rachael Rofe explores two conditions that could still leave some wills on the wrong side of the exemption.

David Tuckwell from ETFShares examines how ASX investors should think about the long-term case for lithium after its recent sell off.

Ethan Xing from Zenith models how fund turnover could become a key driver of after-tax returns under the proposed CGT reforms.

Superannuation was built around assumptions that no longer hold. Adam Nettheim discusses the key challenges he believes policymakers and super funds need to address.

Retirement looks different for everyone. Dr Joanne Earl shares an update four months into her journey.

Australian investors have rarely been asked to navigate so much at once. Arian Neiron from VanEck argues that the Federal Budget has exposed why quality investing needs a rethink in Australia.

The economics behind AI spending look increasingly questionable. Harris Kupperman from Praetorian Capital explains why he thinks today's AI boom has striking parallels with the shale bust.

Curated by Simonelle Mody and Leisa Bell

***

Weekend market update

From Shane Oliver, AMP

Global shares were mostly softer over the last week as the Iran War escalated again with oil prices up and worries remained around AI related earnings and valuations. Eurozone shares rose slightly and the US share market only fell around 0.4% but Japanese and Chinese shares saw sharp falls. The renewed surge in the oil price along with a fall in BHP shares on the back of a weak production outlook for copper and a strike at Port Hedland saw the Australian share market fall but only by around 0.3%. with gains in retail, telco, energy and bank shares partially offsetting falls in IT, mining and consumer staple shares.

Pressure remained on Korean shares which are down 25% from their high on worries about a bubble, profit taking after shares more than doubled, heavily leveraged retail investors closing positions, tightened regulations around buying singe stock leveraged ETFs and not helped by the Bank of Korea raising rates with more hikes likely. But with surging earnings the forward PE is now around 6-7 times!

Bond yields were mixed over the last week – up in Europe and Australia but down in the US and Japan. The $A rose slightly to around $US0.70 as the $US was little changed. The iron ore price rose slightly but remains around $US100 a tonne, but copper, gold and Bitcoin fell. Bitcoin continues to hold above technical support around $US60,000 but has so far failed to rise above its 50 day moving average and looks weak like its still in a “crypto winter”.

Following the end of the US/Iran peace deal and the renewed escalation in the conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Trump at one stage added to confusion with a plan to impose a 20% fee on the value of cargo on ships transiting the Strait but that ridiculous idea was quickly dropped. This in turn has seen oil prices rebound, although they are well below their highs – note that intra day Brent and West Texas spiked to around $US1.20 a barrel earlier in the War.

The resumption of the War begs the question of what has been achieved? Iran is arguably now stronger having proved it can block the Strait, its government is more hardline, there is no resolution to its nuclear ambitions and it still has missiles and drones! There are parallels with the Ukraine and Vietnam wars which showed a superior military power can be challenged – but of course they did not threaten the global economy to the same degree! The relatively moderate response in the oil price and in share markets so far likely reflects the relatively benign experience since the War started and the assumption that the same will continue to apply.

The hit to global oil production has been less than implied by the blockage of the Strait (which would normally mean a 20% hit to oil and gas supplies – ie a 20 million barrels a day reducton in oil supplies) as some was able to bypass the Strait by flowing through the Saudi East-West pipeline to the Red Sea (which has 7 million barrels per day of capacity) and the UAE’s Fujairah pipeline (1.5-2 mbd capacity) and production picked up in other countries. So the hit to production is more like 12-13mbd rather than 20mbd.

But the risk is now high for the global economy and share markets as oil reserves head even lower. The strikes on Iran are intensifying and if really pushed it may attack the UAE port of Fujairah again and could fire up the Houthi’s to block the Bab el-Mandeb Strait out of the Red Sea. Which would severely disrupt the oil bypass routes. So we are back to where we were before the peace deal in that the longer the Strait remains closed or the War escalates the greater the risk that oil prices will have to rise to around $US150/barrel to bring demand down to match the hit to supply. This is not our base case but it’s a high risk again. This leaves US and hence global and Australian shares at high risk of another correction in the seasonally weak months of August and September.

Unfortunately, Australia remains a standout in terms of core or underlying inflation, highlighting why we continue to see the RBA raising rates further this year. The money market is back to seeing a 65% chance of a hike by year end.

Latest updates

PDF version of Firstlinks Newsletter

Monthly Investment Products update from ASX

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Plus updates and announcements on the Sponsor Noticeboard on our website