For many Australians, most of their retirement wealth is tied up in their home. A simple, well-designed program to tap into those trillions in home equity could help boost their retirement incomes.

Such a program exists. However, it remains little known and underused.

The federal government’s Home Equity Access Scheme (HEAS) allows older Australians to access their housing wealth. It is open to Australian residents aged 67 or older who own real estate in Australia, regardless of whether they receive the age pension.

Similar to a reverse mortgage with a bank or specialist lender, the scheme lets older Australians supplement their retirement income through a federal government loan, secured against the equity in their home or other Australian real estate.

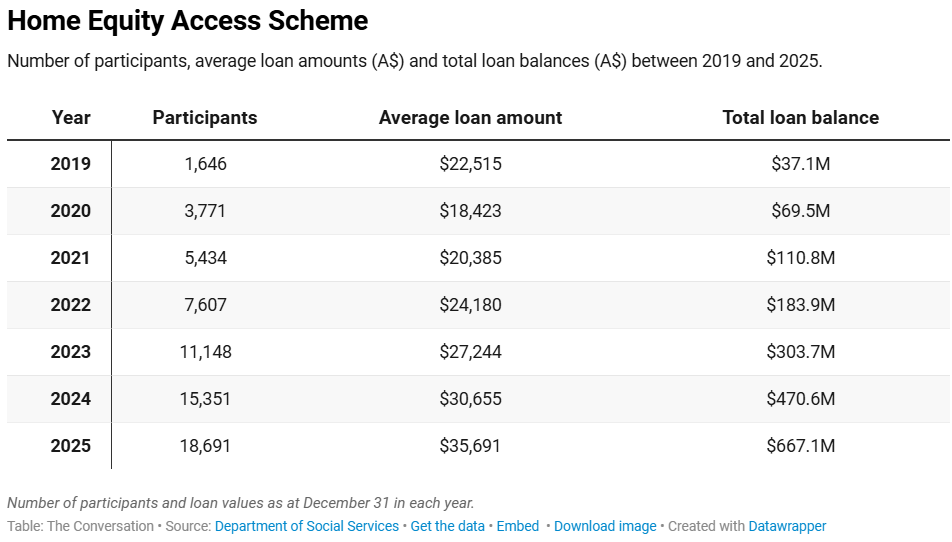

Yet government data shows just 18,691 people are currently taking part in the scheme, a relatively low take-up.

A recent report from Deloitte estimates reverse mortgages are used to access only about 1% of the A$3 trillion value of housing wealth owned by Australians aged 60 and over.

So, why isn’t the government scheme more popular?

How does the scheme work?

Retirees can ‘top up’ any pension payment they receive up to a maximum of 150% of the maximum pension rate. People who do not receive the age pension (self-funded retirees) can receive up to the same maximum.

Participants can choose to receive:

- fortnightly payments, or

- a lump sum advance.

Compound interest is charged on the loan and accumulates over the life of the loan. This is the key difference from standard mortgage loans: people are not required to make regular repayments or interest payments (voluntary repayments can be made at any time).

The interest rate on the scheme is currently 3.95% and has been unchanged since January 2022. This is below the Reserve Bank’s official cash rate of 4.1% and well below commercial reverse mortgages, making it relatively cheap compared with other options.

It was previously known as the Pension Loans Scheme and was introduced in 1985 alongside the pension assets test.

Since 2019, the government has made several changes to the scheme to make it more attractive and expand eligibility. In 2022, lump sum advances were introduced.

A “no negative equity guarantee” was also introduced, meaning participants will never have to repay more than their home is worth, even if house prices fall.

How the scheme stacks up against private lenders

The government scheme shares many similarities with reverse mortgages offered by some banks and specialist lenders.

In both cases, the payments received are added to a loan that increases over time with interest. The loan is usually repaid when the home is sold, or from the estate after the borrower dies.

Voluntary repayments can be made at any time, but are not required.

Both commercial reverse mortgages and the government scheme offer regular or lump-sum payments, and include protections such as the no negative equity guarantee.

The payments have no impact on age pension payments if the loan is taken as a regular income stream to spend on living expenses or non-assessable assets.

The main differences are:

- under the government scheme, the payments are capped at 150% of the maximum age pension rate, whereas the commercial reverse mortgages can offer higher borrowing amounts.

- but banks and specialist lenders charge a higher interest rate on reverse mortgages, currently 8–9% per year, due to higher risks and market-based pricing.

Why such a low take-up rate?

Government data on its scheme shows the average loan amount was about $35,700 in December 2025. Of those taking part, 74% received the full age pension, 17% received a part pension, and 5% were self-funded retirees.

But with only 18,691 people taking part, take-up is still low.

As a government program, the scheme is not widely advertised. So it is good to see more superannuation funds providing their members with information about the scheme.

Some financial advisers may be unsure whether they can advise on the scheme. In January 2023, the Australian Securities and Investments Commission (ASIC) clarified that financial advisers can provide advice on the government scheme without needing an Australian Credit Licence.

Behavioural factors, such as debt aversion and a preference to leave the home as an inheritance, may also explain the low take-up rate. The loan will be repaid out of the sale of the home, meaning proceeds from the sale will be reduced.

However, in our research, we argue that accessing housing wealth can allow families to bring forward bequests and reduce the uncertainty around the timing of inheritances.

Another barrier may be the perceived complexity of the scheme, particularly for retirees with limited financial literacy.

While the rules can seem complex, applications are handled through Services Australia and can be completed online via the MyGov portal, using a standard Centrelink claim process.

The home equity access scheme allows older Australians to access an affordable government loan to supplement their retirement income. It can help retirees who are “asset rich, but income poor” to improve their financial wellbeing, while allowing them to remain at home and in their communities.

Katja Hanewald, Associate Professor in Risk & Actuarial Studies, UNSW Sydney. This article is republished from The Conversation under a Creative Commons license. Read the original article.