For a quarter of a century, the discretionary trust has been the automatic structure for sophisticated property investors in Australia. Accountants defaulted to it. Investors defaulted to it. In our brokerage, we’ve written deal after deal into trust structures without the question of whether it was the right vehicle really coming up.

In the last few weeks, I’ve seen that default start to be questioned. Clients who have held property through trusts for fifteen years are now openly asking whether trusts will still be the right structure if the CGT changes go through, and whether company structures might be the better option. Look, we don’t know yet what Treasurer Chalmers will actually announce on 12 May, but the possibility of a discount cut, a full return to pre-1999 indexation, or something else entirely has been enough to put ownership structure on the table for a cohort that has not seriously revisited it since Peter Costello introduced the discount in 1999.

As director of a commercial finance brokerage, my view is from the adviser side rather than the tax policy side. And for the specific cohort at the centre of the current speculation, multi-property, top-marginal, holding for capital growth, the conversations I’m having now sound different to the conversations I was having six months ago.

The 33% number isn’t random. In my opinion, it’s structural

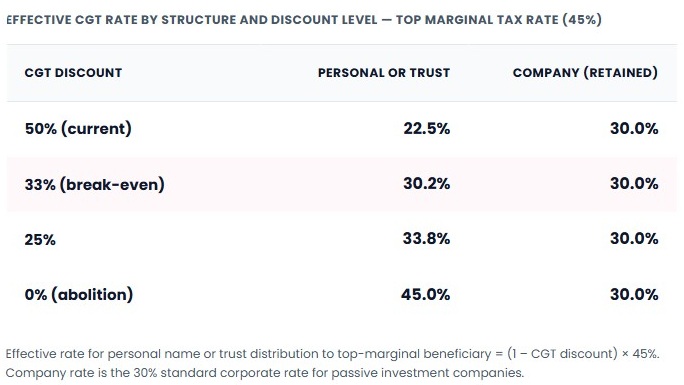

One of the rates Treasury is reportedly modelling is a reduction in the CGT discount from 50% to 33%. Interesting number.

At 33%, the arithmetic on the trust-versus-company decision for a top-marginal investor holding for capital growth sits almost exactly at break-even on new acquisitions. A single top-marginal investor in a trust pays 45% (ex Medicare levy) on 67% of the gain at a 33% discount, which works out at 30.2% overall. A company pays 30% on the full gain. Above 33%, the trust structure still comes out ahead. Below 33%, the company structure starts to compete. That comparison applies to gains retained in the entity; extraction back to the investor re-attracts personal marginal tax, which is a separate question.

33% is the precise point at which the structural case for trusts, for this specific cohort, stops being automatic.

I don’t think it’s a coincidence that 33% is the number turning up in the modelling. It sits at a threshold that matters structurally for the exact cohort the reform is aimed at, and it’s likely no accident that this is where the debate is landing. That’s my read, anyway.

What this might mean in the second half of 2026

A few possibilities seem worth watching, depending on what comes out on budget night.

If the reform lands at 33% or lower, I’d expect the trust-versus-company conversation to become a live one across the multi-property cohort on new acquisitions. Grandfathering of existing holdings would mean no mass restructuring of current portfolios, but the flow of new investor capital could start tilting toward company structures over the second half of 2026 and into 2027.

If the reform lands above 33%, the structural case for trusts holds and the conversations I’m seeing now quietens. The current uptick in client enquiries about alternative structures fades.

If the reform takes the indexation path instead of a rate cut, the arithmetic changes entirely. The break-even still exists but moves around with inflation assumptions and hold periods. Different question, same cohort revisiting it.

The broader point for readers

The public debate about CGT reform has been conducted mostly at the policy level: the right mechanism, the right rate, the right distributional outcome. That’s the conversation Treasury is resolving.

The 33% number is structurally meaningful for this cohort in a way the public debate hasn't really surfaced. That's worth knowing, whether or not the reform ultimately lands there.

I’ll be watching budget night like everyone else. And like the accountants and advisers working through these questions alongside their clients, the second read on what’s announced will matter as much as the first. That, I suspect, is where a fair amount of the real behavioural response to any reform will sit. Not in whether investors exit the market, but in how they choose to structure their next entry into it.

Nadine Connell is Co-Founder & Director of Smart Business Plans, a Gold Coast-based commercial finance brokerage. She is an authorised credit representative of LMG Broker Services (CR 553930, MFAA member). This article is general information only and does not constitute personal financial or tax advice. Readers should obtain independent professional advice relevant to their circumstances.