The ABC recently ran a series asking what, if anything, governments can do about high inflation beyond simply relying on the Reserve Bank to raise interest rates (a policy tool that every knows is cruel and unusual).

One idea that gets floated is using the GST as an active stabilisation tool, automatically increasing the GST when inflation rises, and cutting it when inflation falls.

At first glance, this sounds sensible. If inflation is too high, why not temporarily raise consumption taxes to dampen spending?

But when you actually model the idea formally, the results are surprisingly bad. Terrible in fact!

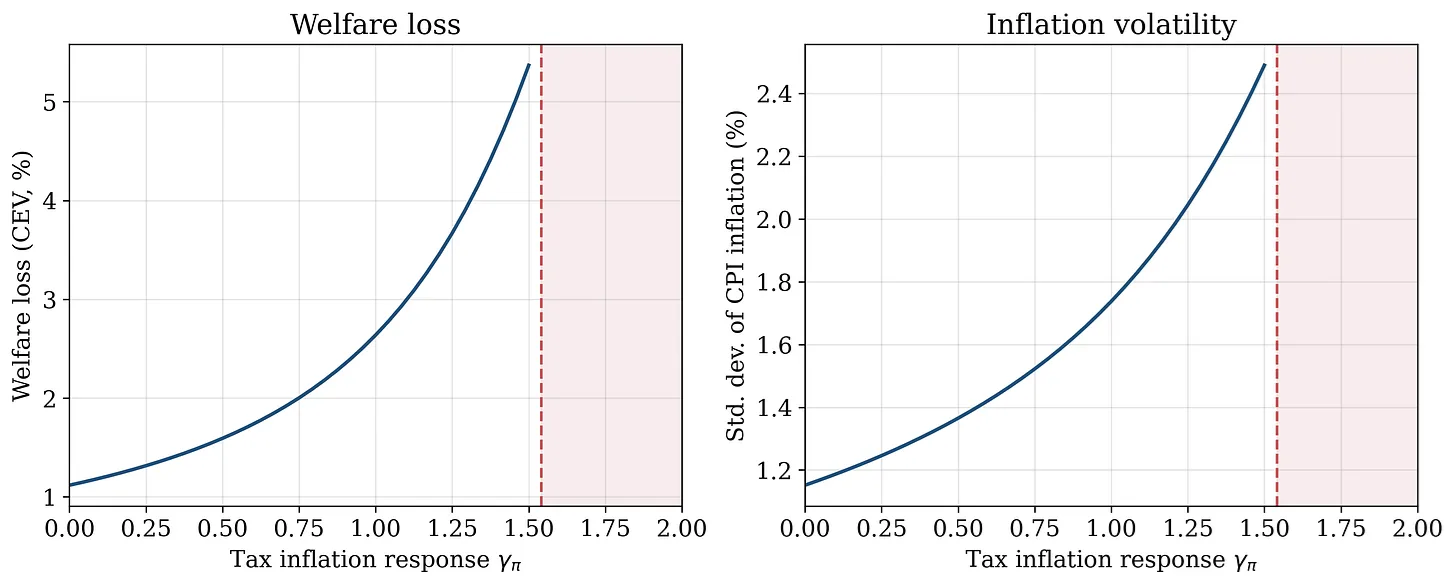

The charts below show the welfare loss and inflation volatility in an economy as a function of a single parameter: how aggressively the GST responds to inflation. At zero the GST rate never changes (the economy today). As the parameter becomes positive the GST rises automatically whenever inflation rises with greater degrees of responsiveness.

Perhaps surprisingly, welfare falls sharply (ie welfare losses increase) the more aggressively the GST responds to inflation. Inflation itself also becomes substantially more volatile. What explains this counter intuitive result!?

Downward dog inflation

Imagine we lived in a world where the GST automatically increased whenever inflation rose. If inflation jumped by 3 percentage points the GST would mechanically rise from 10% to 15%.

Now consider the sort of shock Australia has recently experienced: turmoil in the Middle East pushing up global oil prices.

To keep things simple imagine you run a yoga studio. Your business barely uses petrol directly, so the oil shock itself is not especially important for your costs.

But the GST is.

In Australia, firms typically advertise and set prices inclusive of GST. And because many firms only adjust prices infrequently — perhaps once or twice a year — they have to think carefully about where taxes and costs are likely to be over the coming year when they decide on prices today.

So what happens when news breaks of a major geopolitical conflict likely to push inflation higher?

In a world with a varying GST policy, the answer is obvious: businesses immediately expect the GST rate to rise in the near future. War today, means high oil prices in the coming weeks, which means higher inflation prints in the coming months and thus a higher rate of GST for the next year or so.

As a yoga studio owner, this matters enormously. If the GST rises from 10% to 15% while your advertised prices stay fixed, your after-tax revenue falls and your profit margins get squeezed.

So what is the rational response?

You raise prices today.

Even though the oil shock barely affects your own business directly, the expectation of higher future GST causes you to increase prices immediately in anticipation.

And once every firm in the economy starts thinking this way, the policy becomes self-reinforcing.

The initial inflation shock causes firms to expect higher GST rates in future. Firms then raise prices more aggressively today to pay for those future taxes. That additional price-setting behaviour pushes inflation even higher, which in turn triggers even larger GST increases.

Rather than stabilising inflation, the policy amplifies it increasing volatility. In fact if the GST-responsiveness-to-inflation parameter gets too high (about 1.5 in the plots above) the economy becomes “indeterminate” which is economist speak for double plus bad.

Under a constant GST regime, many firms — like the yoga studio — might barely respond to an oil shock at all. But once GST becomes an active “counter-cyclical” tool, even firms with little direct exposure to the original shock have an incentive to raise prices preemptively.

The result is higher inflation volatility, more distorted price-setting behaviour, and ultimately lower welfare across the economy.

The irony is that while counter-cyclical GST policy sounds stabilising in theory, once you account for forward-looking firms and sticky prices, it can end up making inflation dynamics substantially worse.

Dr Isaac (Zac) Gross is a lecturer in economics at Monash University. This article was first published via Zac’s blog, Gross National Product, and is reproduced with permission.