The quality factor is a defensive strategy designed to outperform during periods of heightened market volatility, lower inflation and lower growth regimes. The approach is reinforced by academic research and empirical findings.

When applied in international equity markets, quality strategies have delivered the characteristics intended: lower beta, shallower drawdowns, outperformance during market stress and defensive sector exposures. This will explore whether the quality factor can be replicated effectively in the Australian equity market.

The Australian equities market is one of the most concentrated by stock and sector. The universe is also small relative to global markets. The findings show that these nuances present challenges when assessing factor strategy efficacy.

Defining quality

Research in identifying systematic drivers of investment returns contributed to the emergence of factor indices, which track the performance of a set of companies with similar fundamentals, price behaviour, or a combination of both. This has led to the rise of factor-based ETFs which track these indices, while retaining transparency, liquidity and ease of trading for investors.

MSCI is a global leader in constructing factor index strategies. Through their research, they found companies with three fundamentals: high return on equity, stable year-on-year earnings growth and low financial leverage, exhibited quality ‘defensive’ characteristics1.

This means typically falling less in a downturn and recovering to previous highs more quickly than the broader market. When implemented correctly, a quality strategy should exhibit:

- Long term risk-adjusted outperformance (positive information ratio)

- Beta at or below 1.0 relative to the benchmark (lower systematic risk)

- Outperformance during periods of market stress (the ‘flight to quality’ effect)

- Low exposure to cyclical sectors.

Testing the efficacy of the quality factor in Australia

There are two indices that attempt to capture the quality factor in the Australian market; Solactive Australia Quality Select index and MSCI Australia IMI Quality Index. These both select companies using MSCI-defined quality fundamentals. To test their efficacy, we apply the same tests used to qualify the international quality factor to assess whether these indices deliver the characteristics investors should expect in the Australian share market.

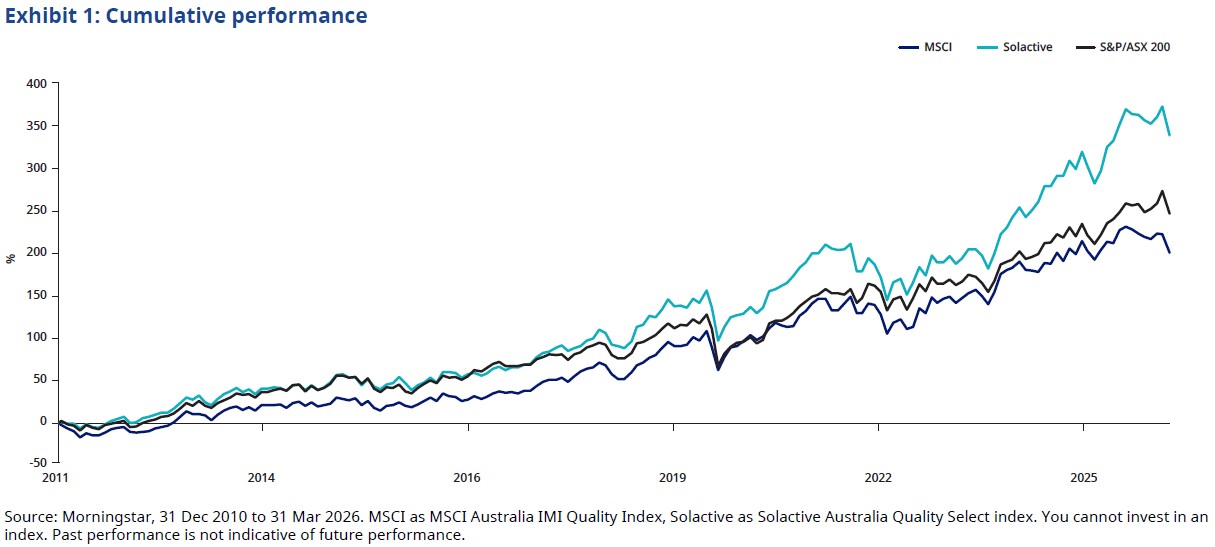

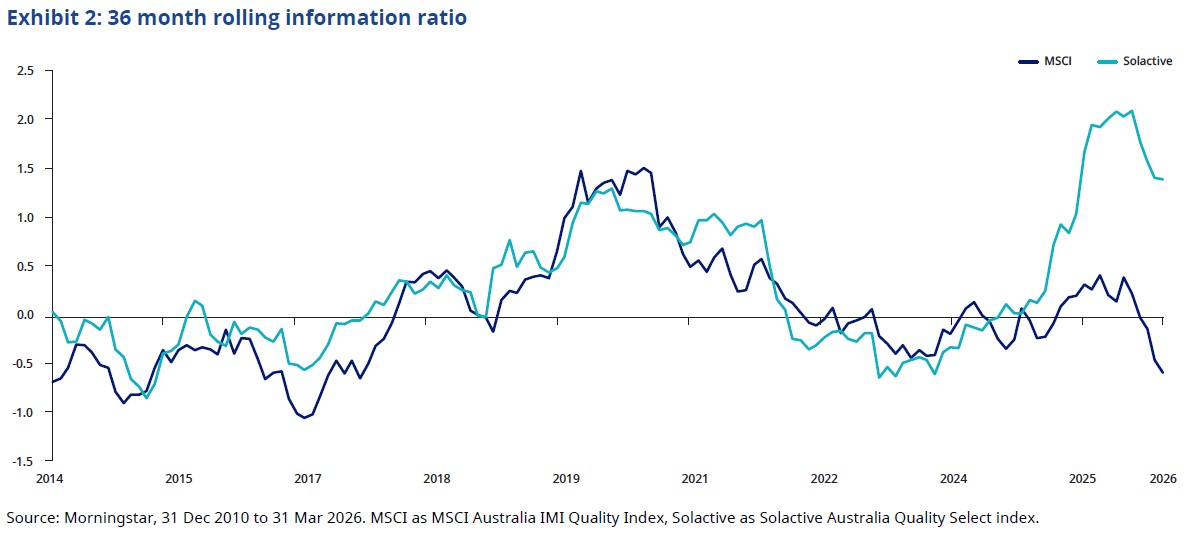

Mixed performance

Despite targeting the same quality fundamentals, the performance results are materially different. The Solactive strategy has outperformed but has not been consistent on a risk-adjusted basis. The rolling three-year information ratio has oscillated between positive and negative territory and has had prolonged periods below zero. The MSCI strategy has underperformed. The inconsistency suggests that any outperformance is episodic rather than structural.

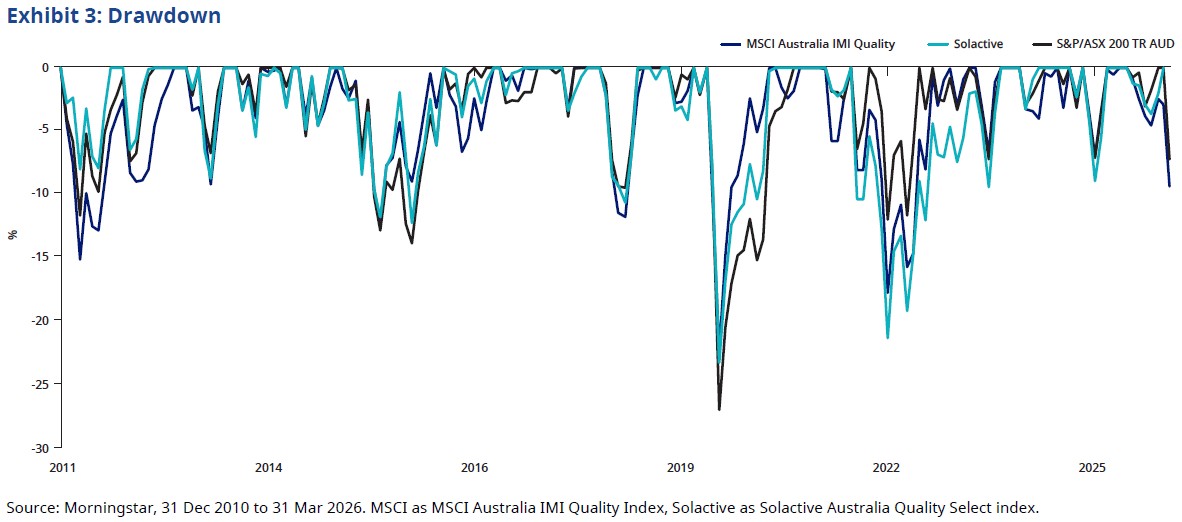

Inconsistent drawdown protection

A quality strategy should typically provide consistent downside protection during market stress. But neither strategy has. During several stress event periods including the 2018 US/China trade war, 2024 yen carry trade and 2025 US liberation day events, the drawdown for both strategies was larger than the S&P/ASX 200.

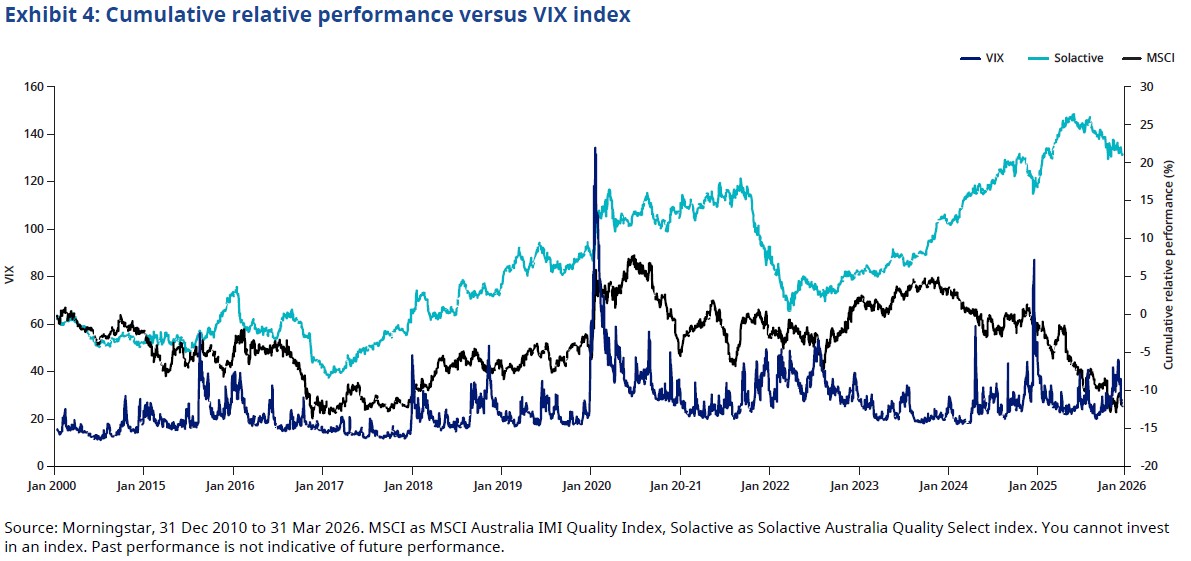

No flight to quality during stress events

Neither strategy shows a definitive positive correlation between VIX spikes and the index’s relative performance versus the S&P/ASX 200.

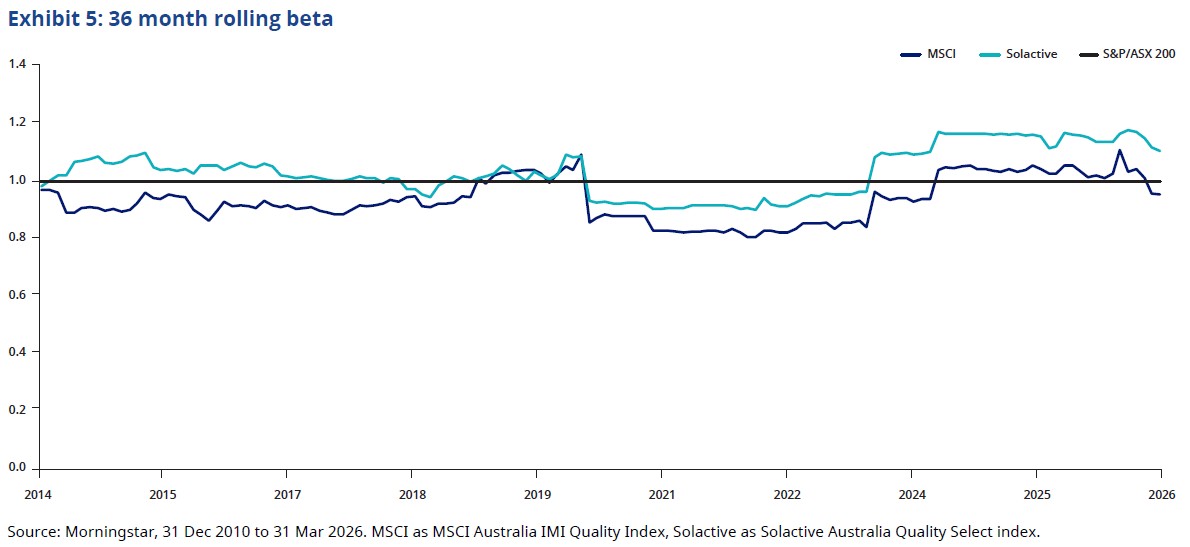

Higher beta

The MSCI strategy has demonstrated a lower beta. However, the Solactive strategy’s higher drawdowns and upside capture ratio has culminated in a rolling three-year beta persistently above 1.0 relative to the S&P/ASX 200, reaching levels above 1.15 in recent periods. This characteristic is more akin to the growth factor rather than quality.

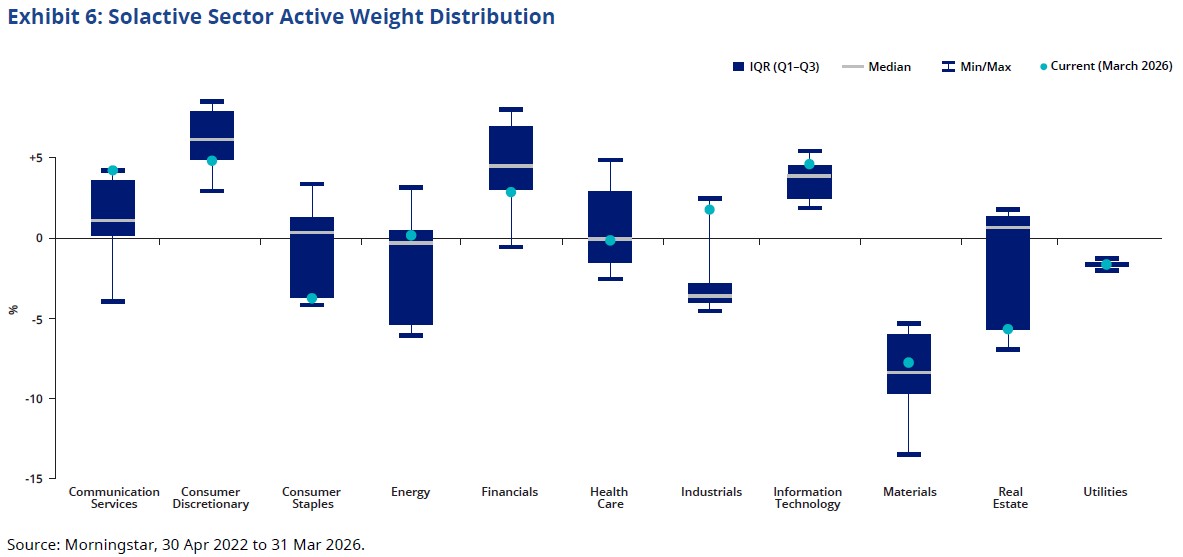

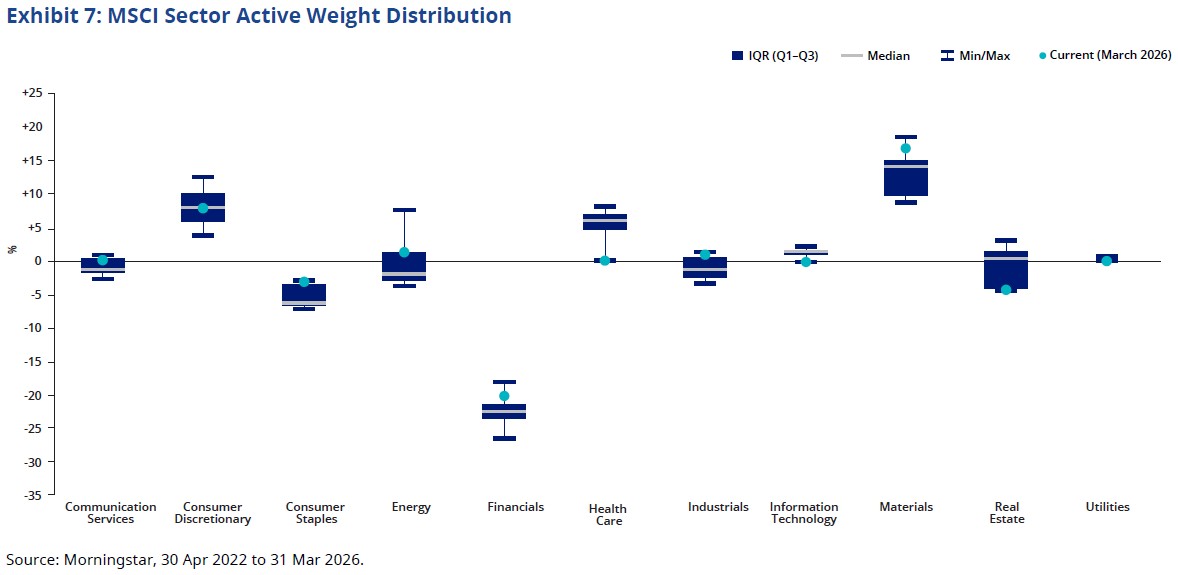

High exposure to cyclical sectors

The sector composition tells a different story to what the international quality strategy delivered. MSCI and Solactive Australian quality strategies maintain a persistent overweight to financials and materials respectively and to consumer discretionary, which is cyclical. Both strategies have been underweight the defensive sector, consumer staples.

Inconsistent factor exposure

We applied the same multi-linear regression analysis against market beta, size, growth, value and momentum. Regression analysis is a statistical method used to explain why something happened in relation to something else. The results showed that both strategies had a higher proportion of performance unexplained by factors. The Solactive strategy had a higher correlation to growth but, uncharacteristically, also a high correlation to smaller companies.

These examples and metrics confirm, in our view, that a single quality factor approach in Australia does not behave as investors would expect.

Why can’t the characteristics of international single factor strategies be replicated in Australian equities? It is worth, then, to consider the characteristics of the Australian equities market and the companies included.

The Australian concentration conundrum

The Australian indices’ failure to deliver genuine quality characteristics is not unique. It is a structural problem inherent to the Australian equity market. In our research paper The Australian Concentration Conundrum, we showed that single factor strategies applied in Australian equities fail to achieve factor efficacy for three distinct reasons: high stock and sector concentration, and smaller starting universe. The annual rebalance of the Solactive index also poses a challenge.

Stock concentration

The S&P/ASX 200 is one of the most concentrated equity markets in the developed world. The top 10 stocks account for almost 50% of total exposure. This concentration limits the ability to construct a meaningfully differentiated factor portfolio.

Sector concentration

Financials and materials account for more than 50% of the S&P/ASX 200. These sectors behave differently to other sectors. Banks are highly leveraged and miners have volatile earnings, lacking quality characteristics. This means constructing a benchmark-aware strategy dilutes exposure to the quality factor.

Small starting universe

With only 200 stocks in the S&P/ASX 200, constructing a portfolio subset based on factor scores increases idiosyncratic stock exposure, limiting systematic factor exposure.

The annual rebalance amplifies the challenge

The Solactive strategy rebalances annually. An annual rebalance means the portfolio is therefore slow to respond to deteriorating factor signals. This is more prevalent given the more cyclical nature of the Australian equities market.

Conclusion

The quality factor in international equity markets has been an effective defensive strategy over the long term, delivering risk-adjusted outperformance, lower beta, shallower drawdowns and outperformance during periods of market stress, and lower inflation and growth regimes. However, when a single factor quality strategy is applied in Australian equities it fails to achieve factor efficacy for three reasons: stock concentration, sector concentration and a small starting universe.

This does not mean quality cannot be achieved in Australian equities, but rather that a pure single-factor quality approach is unlikely to be the most effective implementation in a concentrated, cyclical market such as Australia. The more effective path is an index that places quality characteristics at the centre of construction and uses complementary characteristics to manage the sector and concentration risks that undermine single factor approaches in this market. Identifying the most effective implementation approach is a priority within our ongoing research.

Investors seeking true quality equity exposure should look beyond the Australian market to international strategies where the universe offers the breadth and depth of companies to perform as intended.

For those seeking diversified exposure to Australian equities, alternative strategies such as a quality plus approach or equal weighting are worth considering.

1. Eugene L. Hung, R., et al (2015) Flight to Quality, Understanding Factor Investing.

VanEck is a sponsor of Firstlinks. The above excerpts have been adapted from VanEck’s White Paper ‘The limits of quality in Australia’. Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.