As private markets continue to evolve, we explore three themes shaping the landscape today: how to navigate an expanding range of investment structures, where we see the private equity cycle heading into mid-2026 and what AI disruption means for private companies.

- Making Sense of an Expanding Market: Private equity and private credit vehicles now come in myriad structures with various return and risk profiles. We compare key differences and take a closer look at flows.

- The Cycle: Fundraising, Exits and Distributions: Top U.S. private equity sponsors continue to attract capital, portfolio backlogs may drive a rebound in exit activity and distributions seem to be recovering from their 2022 – 2023 lows. We examine what this means for investors.

- Decoding the “SaaSpocalypse”: We believe nimble private equity sponsors have the potential to capitalize on recent AI-driven market dislocations within the software sector.

The private markets landscape

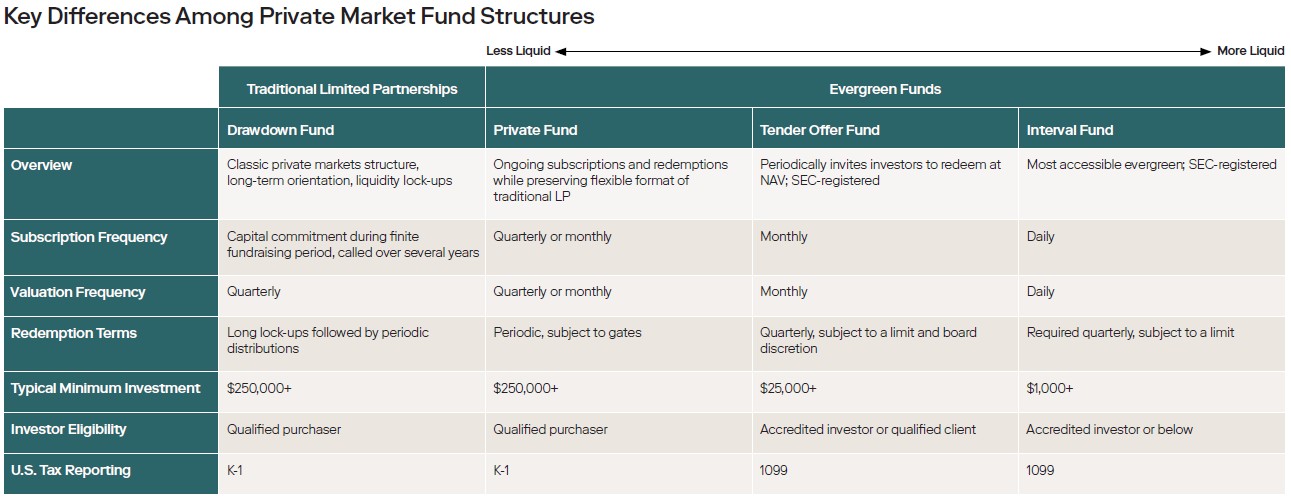

There are now many ways to gain exposure to private markets, from traditional drawdown funds to a variety of evergreen vehicles. Strategies are more widely accessible, and more varied in how they are delivered.

In this expanding market, we believe investors and advisors should seek to understand key characteristics of different structures—including portfolio valuation frequencies, redemption terms, investor eligibility and more—when assessing suitability in meeting long-term objectives.

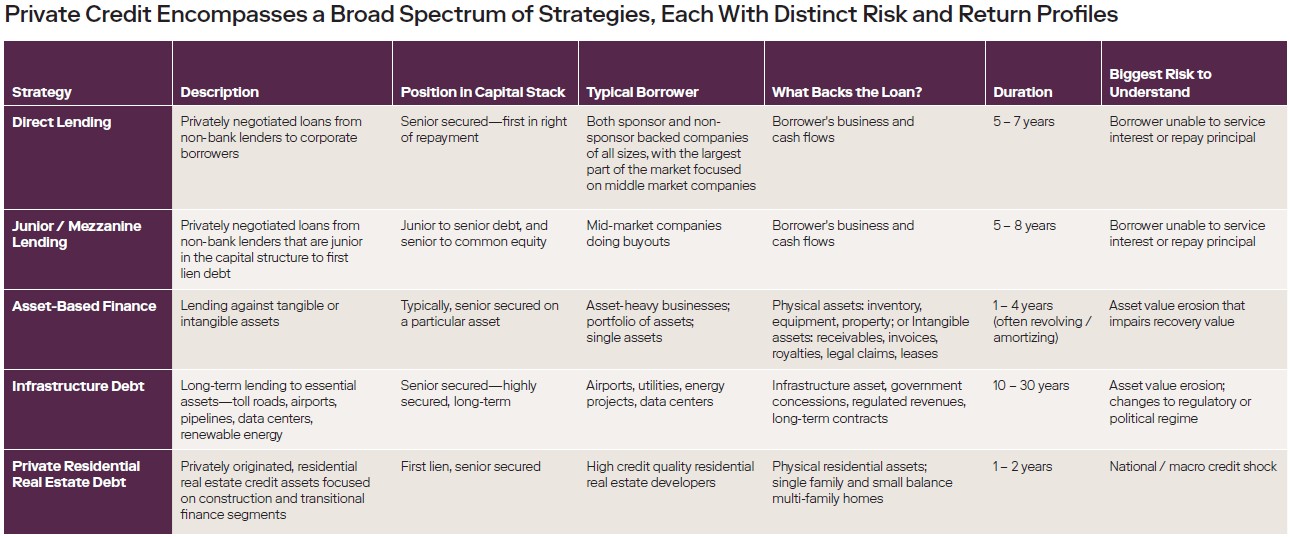

The private credit landscape

Private credit connects borrowers directly with private capital, bypassing traditional banks and generating income for investors through contractual coupon payments. Loans can be structured with varying levels of seniority and collateralized by a borrower’s cash flows, assets or projects.

Direct lending is what many investors think of when they hear “private credit”. However, private credit is a fast-growing and increasingly heterogeneous market offering a range of strategies with complementary risk, return and borrower profiles.

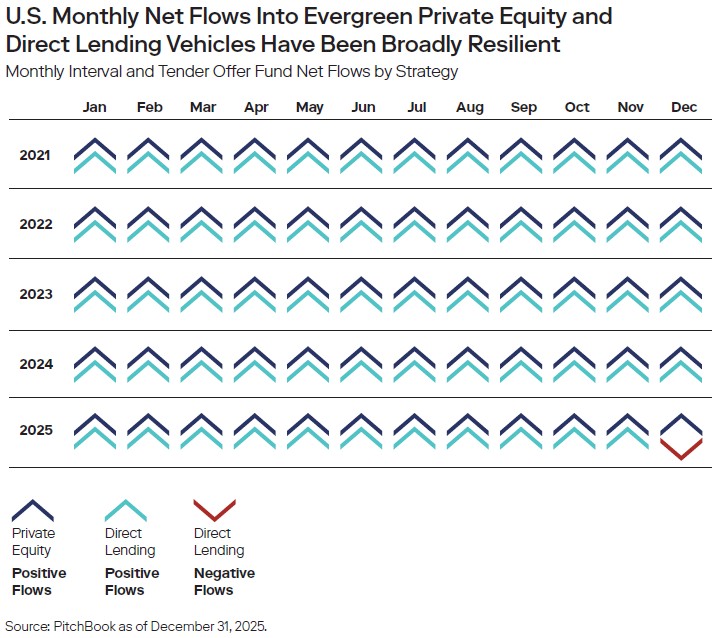

Despite the headlines, evergreen funds continue to attract capital

Some media outlets have warned that recent redemptions at certain private credit evergreen funds could have a cascading effect. However, overall net fund flows into U.S. evergreen strategies have in fact been healthy.

Evergreen private equity strategies reported positive net flows for 60 consecutive months through December 31, 2025.

Evergreen direct lending strategies did nearly as well, reporting positive net flows in 59 out of 60 months during the same period.

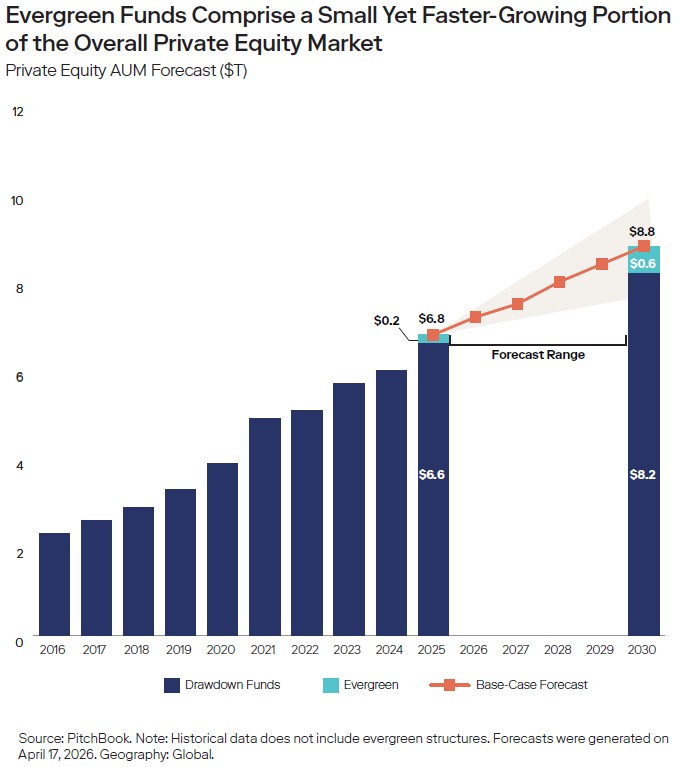

Private equity fundraising: Evergreen AUM projected to grow

While evergreen vehicles are expected to expand at a faster rate than traditional drawdown funds, we believe they will likely still represent a relatively small share of the overall private equity market in the near term.

Meanwhile, private equity capital is increasingly concentrating among larger, more experienced managers. In 2025, firms commanding at least $5 billion in assets accounted for roughly half of all capital raised, the highest share since the 2008 financial crisis.1

We believe this trend is likely to persist as investors increasingly focus on manager selection, reinforcing the importance of access to well-capitalized, top-tier sponsors.

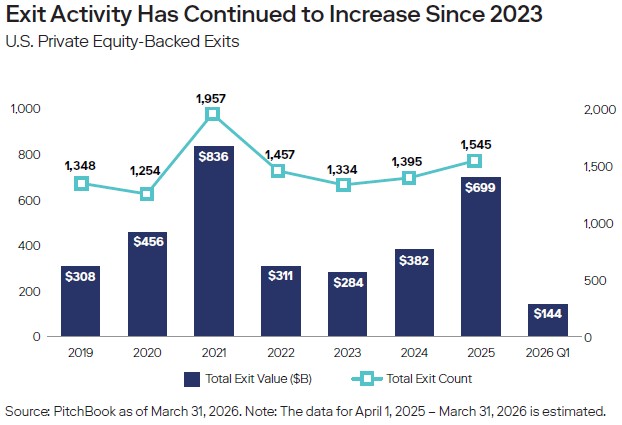

Private equity exits: Conditions support continued activity in 2026

U.S. private equity exit activity—defined as the cash generated from initial public offerings, sales to strategic acquirers and sales to other private equity firms—gained momentum starting in 2024 and continued through 2025, with particularly strong activity in the second half of 2025.

Exits matter because they can help validate private equity valuations, and recent transactions indicate that companies are generally selling close to prior marks, supporting investor confidence and cash generation.

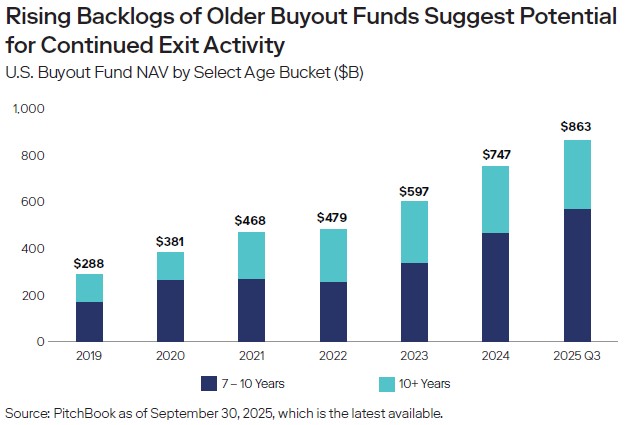

We believe the growing backlog of older private equity-backed companies suggests exit activity may remain elevated. Holding backlogs, measured by Net Asset Value (NAV), for buyout funds aged seven years or older reached $863 billion as of September 2025, highlighting growing pressure from investors wanting distributions.

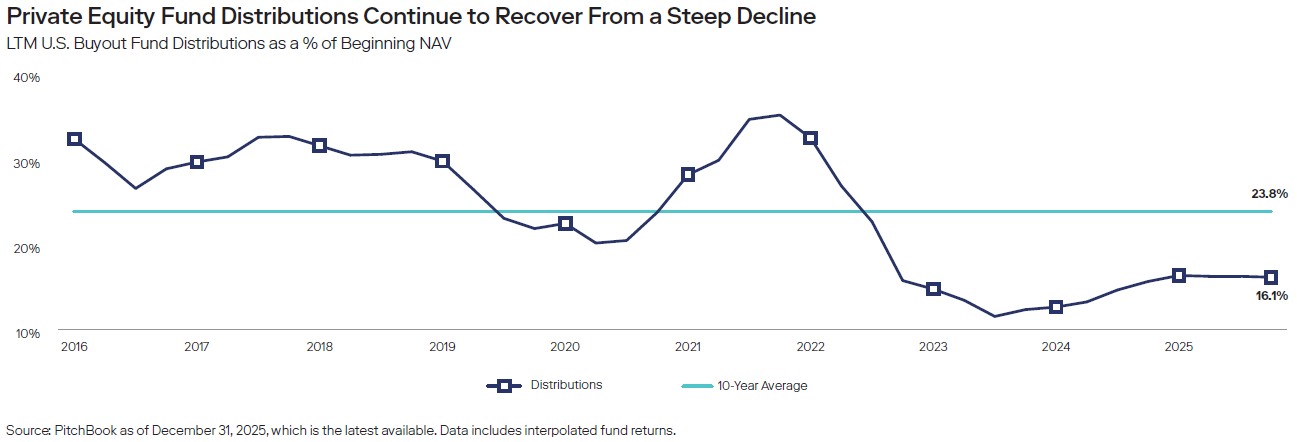

Private equity distributions: The recovery continues

Fundraising, exits and fund distributions are linked in a virtuous cycle: exits drive distributions, which can then be recycled into new private equity funds and investments.

After a sudden decrease in the second half of 2021, distributions from buyout firms to their investors began to recover near the end of 2023, yet still remain below historical averages. We expect a pickup in exit activity to flow through to fund distributions—an important link in the private equity capital cycle.

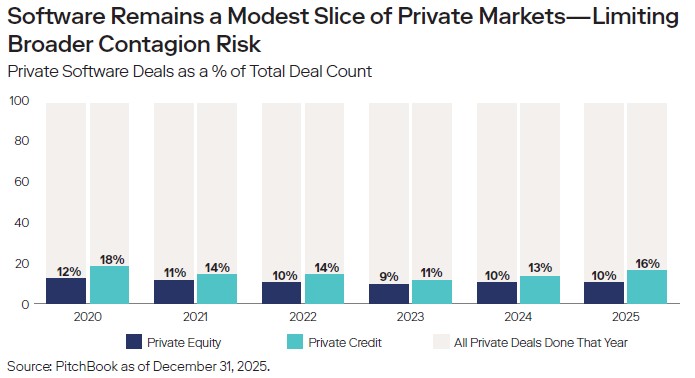

Decoding the “SaaSpocalypse”

The rise of agentic AI has contributed to an increase in redemption requests at certain private credit funds exposed to private software companies. However, the data suggests the impact may be more limited than initially feared. Software has represented less than 13% of all private equity deals annually from 2020 – 2025, with private credit exposure similarly accounting for 11% to 18% of annual deal activity.

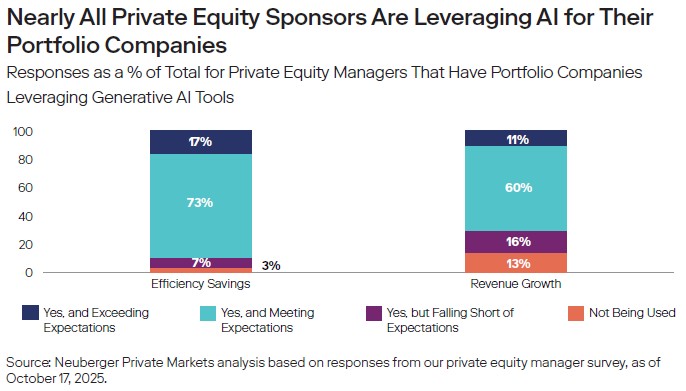

While AI is undoubtedly disruptive, a recent Neuberger Private Markets survey shows that most private equity sponsors are already deploying the technology across their portfolios in practical, value-enhancing ways. This reinforces our view that AI-driven disruption is unlikely to be uniform—and that market dislocations may create opportunities for nimble sponsors and well-positioned lenders.

1 Source: PitchBook as of January 30, 2026.

Neuberger is a sponsor of Firstlinks. This material is provided for general and educational purposes only. This material should not be construed as investment advice or an offer or solicitation to buy or sell securities. You should consult your accountant, tax adviser and/or attorney for advice concerning your own circumstances.

For more articles and papers from Neuberger, click here.