I used to believe the process of investing was all about selecting the right stocks, locking in a great return, rinse and repeat. Stock picking intuitively aligns with the way many people imagine investing works. While it might be easy to blame the glamour of Scorsese’s Wolf of Wall St, most financial commentary tends to focus on individual companies and quirky market personalities. It’s certainly more entertaining to read about what Elon Musk has said this week than to dive into the merits of Modern Portfolio Theory.

In reality, the most important investment decision you’ll ever make probably won’t be that speculative small cap bet or the hot stock tip your neighbour was talking about. It is far more fundamental than that.

Your asset allocation decisions will always be the biggest driver of long-term returns, and therefore your investment success. One of the most cited studies in modern investing is Determinants of Portfolio Performance by Brinson, Singer, and Beebower (1991). The research estimates that asset allocation explains 94% of a portfolio’s return variability over time. Your mix of growth and defensive assets will dictate not only long-term returns, but also how you align your investment strategy to your goals and manage risk appropriately.

Why it matters

If investors could look into a crystal ball and be told which asset class was going to outperform each year, asset allocation decisions would be easy. But this is far from reality. There is a degree of randomness inherent in determining which assets perform best on a short-term basis.

The chart below demonstrates how difficult it is to consistently pick winners and losers. Allocating capital across a range of asset classes helps investors avoid anchoring their portfolio to a single narrative.

Source: Vanguard Asset Class Tool.

But most retail investors don’t ponder correlation metrics over breakfast. They’re focusing on outcomes like purchasing a home, generating a steady income or retiring comfortably. The fuss over asset allocation is justified. It is the primary mechanism that turns goals into a sound investment strategy.

For instance, a long-term goal e.g. a comfortable retirement with decades to run, means an investor may allocate higher exposure to growth assets. On the other hand, if an investor is looking to purchase a home in the next three years, they may favour a larger allocation to defensive assets to manage risk and achieve this goal.

The subtle differences

Many casual investors demonstrate lower levels of engagement with their asset allocations, especially when it comes to super. For example, AustralianSuper currently has over 90% of members in the balanced option, which targets a 75/25 split between growth and defensive assets. Given the average age of an AustralianSuper member is around 42, one could argue that a significant portion of investors may be positioned more conservatively than their time horizon requires.

Even small differences in allocation can compound into surprisingly large gaps over time. No allocation is inherently ‘wrong’, but it may not be optimal for every investor and the cost of being misaligned can accumulate over decades.

The key point is that your allocation should be an intentional decision that reflects your goals, risk capacity and ability to withstand short-term fluctuations. Most investors will need some level of equity allocation to achieve their long-term goals, but determining the ‘right’ level will be highly personal.

The part investors often miss

There is no perfect formula to determine your asset allocation. Traditional frameworks can provide useful guidance, but they cannot fully capture the personal nature of the decision.

An overlooked implication is that market dynamics are constantly shifting. The risk profile of asset classes and the correlations between them are not static. But that doesn’t mean investors should attempt to time the market. Instead, it highlights the importance of understanding how the landscape has evolved.

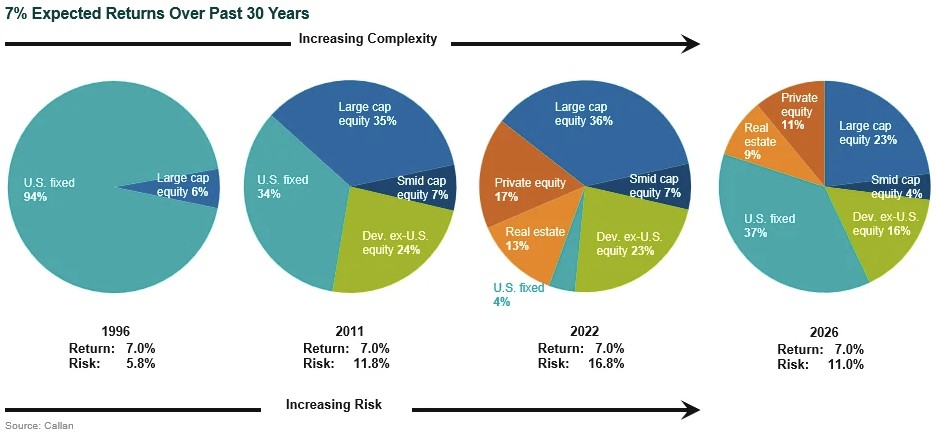

I believe The Callan Institute illustrates this point well. Their research suggests that investors are required to take on almost twice the risk they did 30 years ago to achieve a nominal 7% expected return in the next decade.

Source: The Callan Institute. 2026.

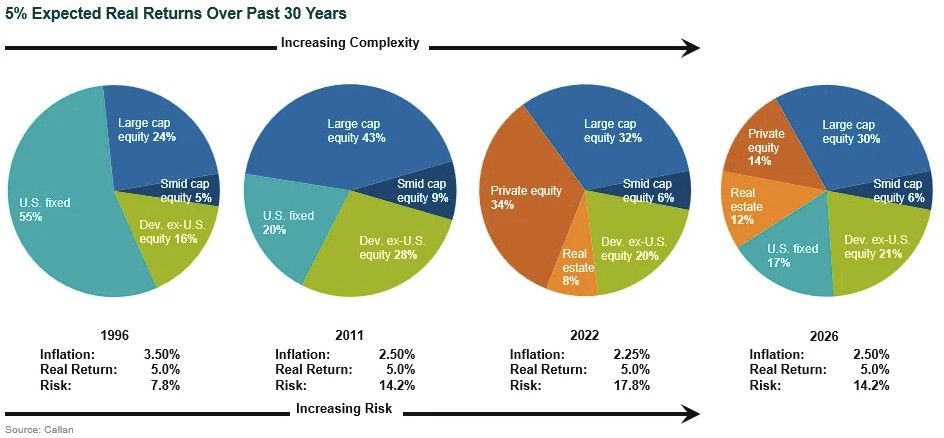

Although, the report notes that the mid-90s were uniquely characterised by not only higher fixed income yields but also higher inflation. To adjust for this, researchers looked at what it would take to earn a 5% real return instead. The figure below shows that the conclusion remains similar.

Source: The Callan Institute. 2026.

Market dynamics don’t just change over the long-term either. The environment has shifted even in the last few years. Achieving a 7% expected return is now far more feasible than it was in 2022. Back then, an investor would have needed to allocate ~96% of their portfolio to growth assets to reach 7%. In 2026, Callan believes over a third of a portfolio can sit in fixed income whilst still maintaining the same expected return.

The broader takeaway is that the mix of assets required to meet return objectives evolves over time. Investors today face an increasingly complex landscape. It is difficult to set an asset allocation and expect it to remain appropriate in the long-term.

Simonelle Mody is an Investment Specialist at Morningstar Australia. She writes for retail investors and financial advisers on topics spanning portfolio construction, market trends, ETFs and investor behaviour.