(This article was available to Morningstar subscribers on 14 October 2020 and some prices have changed in the week since).

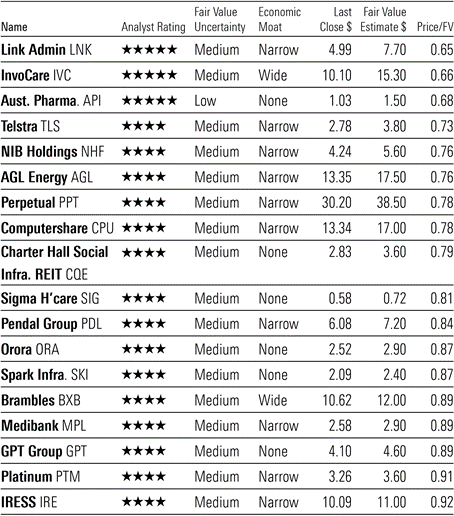

Takeover target Link Administration, funeral home operator InvoCare and Australian Pharmaceutical Industries head a list of stocks trading at discounts of up to 30% and in most cases a competitive edge of a decade.

Eighteen companies under Morningstar coverage are trading at discounts of between 10 and 30%, with mostly 'medium' uncertainty ratings, a Morningstar Premium stock screener reveals.

More than half the names on the list have narrow moats, which implies a ten-year competitive advantage. Two names have wide moats—or 20-year competitive advantage: InvoCare and pallet maker Brambles.

Following is a snapshot of some of the companies mentioned. As always, we invite you to click on the links to get a fuller picture of Morningstar analysts' take on the pros and cons of each.

18 undervalued Australian equities under coverage

Source: Morningstar Premium. Data as at 3pm, 14 October 2020.

Most discounted

Link Administration is one of the three Technology names on the list. It has created a narrow economic moat in the Australian and UK financial services administration sectors via its leading positions in fund administration and share registry services. Client retention rates exceed 90% in both markets.

Link surged 25% last week on news that it had received a conditional, non-binding indicative proposal from a consortium comprising Pacific Equity Partners, Carlyle Group and their affiliates to acquire all of Link. Morningstar equity analyst Gareth James, who foresaw the takeover, says the $5.20 offer undervalues the company. “The offer is well below our $7.70 fair value estimate, meaning we’re unlikely to recommend shareholders accept,” James says. “Although the offer is at a 30% premium to the last closing price before the offer was announced, the shares are still 13% below where they were at the start of 2020.”

Wide moat InvoCare is the largest funeral, cemetery, and crematorium operator in Australia, New Zealand, and Singapore. InvoCare owns a portfolio of 60 brands, including three national Australian brands: White Lady, Simplicity Funerals, and Value Cremations. 2020 has been a challenging year for InvoCare. Social distancing and an increased focus on sanitation amid the covid-19 pandemic has led to a benign flu season and a lower death rate. However, Morningstar analyst Mark Taylor expects InvoCare to gradually increase its market share and sales to grow at a mid-single-digit pace for the next five years. “Over the longer term, we expect the ageing and growing population to boost case volumes,” says Taylor. ABS data suggests this is likely to accelerate after fiscal 2024, peaking at between 2 and 3% by 2032. “In our opinion, InvoCare is well positioned to capitalise on this growth, given its dominant position in the domestic market and its wide economic moat,” Taylor says.

Australian Pharmaceutical Industries is the franchisor of the Priceline Pharmacy network and directly owns and operates stand-alone Priceline stores which sell personal care and beauty products. In an effort to diversify away from the highly regulated low growth and low margin pharma distribution business which contributes 75% of revenue, API is growing a consumer brands portfolio and also recently acquired Clear Skincare, a skin treatment chain. API carries a low uncertainty as Morningstar expects no anticipate any regulatory changes in the Pharmaceutical Benefits Scheme or pharmacy ownership legislation.

Cross-section of sectors

Telstra, Australia’s leading telco provider, rose almost 4% during the compilation of this survey, but it remains materially discounted, according to the valuation of Morningstar equity analyst Brian Han. The nbn’s $3.5 billion upgrade last month will affect Telstra and its rivals but it’s too early to quantify, Han says. Telstra gained 3.96% to $2.89 on Monday after chair John Mullen told its annual general meeting the board wants to ensure investors' payout is not cut. The board is prepared to waiver some rules to maintain the full-year 16 cents per share payout.

Telstra generates around 40% of group operating earnings from the mobile telephony division. Its mobile subscriber base has ballooned from 12.2 million in fiscal 2011 (40% market share) to 18.8 million in fiscal 2020 (44% share). “The growth has been driven by the superior quality, speed and coverage of its mobile network,” Han says, “one that is capable of offering triple plays (mobile, data, audio-visual media), further enhancing its competitive positioning compared with peers.”

Financial services

Financial Services companies account for almost a third of the names on the list. And within that sector, three asset managers appear. In order of biggest discount to Morningstar fair value estimate, they are: Perpetual, Pendal Group and Platinum Asset Management.

Perpetual recorded a sluggish fiscal 2020, but Morningstar director of equity research Adam Fleck says investors should look past that as the future holds the prospect of stronger earnings growth. Key to this will be a couple of acquisitions it made this year: the 75% acquisition of US asset manager Barrow Hanley will help ward off index funds, while the acquisition of Trillium boosts its ESG credentials. It’s also worth noting that Perpetual is the biggest shareholder in Link Administration.

Insurers NIB Holdings and Medibank Private round out the names within Financial Services.

Technology

Alongside Link Administration, two other narrow-moat-rated Technology sector names appear: Computershare and IRESS. Computershare has grown via global acquisition to become the world's leading provider of share registry services, which constitutes about 60% of earnings.

Morningstar’s James says cost-cutting measures will help Computershare increase its pre-tax earnings from 22% in fiscal 2020 to 33% by fiscal 2030.

“The capital-light business model should enable regular dividends, the elimination of net debt within the decade, and a return on invested capital that exceeds the weighted average cost of capital for the foreseeable future,” James says. “The recurring and defensive nature of earnings influences our medium fair value uncertainty rating.”

Healthcare

In Healthcare, the other name alongside API is pharmaceutical distributor, wholesaler and pharmacy franchisor Sigma Healthcare. It is also the only name on the list that carries a Poor stewardship rating. The company has been slower than peers to diversify itself away from the low margin, low growth pharmaceutical distribution business, says Morningstar’s Han. On a brighter note, however, covid-19 has had little impact, highlighting the inelasticity of demand for health products. “The firm expects a recovering EBITDA to better fiscal 2019 levels by fiscal 2023 and we share similar optimism,” Han says. He retains his long-term estimates and forecasts a five-year EBITDA compound annual growth rate of 15%.

Real estate

Two real estate investment trusts make the cut. One is Charter Hall Social Infrastructure REIT, which is trading at a 21% discount to fair value. The other is GPT Group, which is Australia’s oldest listed property trust (1971). GPT remains dominated by retail malls that generate about a third of its revenue, and another quarter from office.

However, the group’s office portfolio is not as exposed to the immediate threat from the coronavirus, says Morningstar analyst Alex Prineas. “There has been very little new office supply in the Sydney or Melbourne central business district in the past five years so 2020 began with very tight supply, which we anticipate will loosen.”

Utilities

Among the Utilities sector, two names feature: AGL Energy and Spark Infrastructure Group.

Morningstar equity analyst Adrian Atkins recently trimmed his valuation for AGL on lower expected wholesale electricity prices. However, he still considers the low-cost energy producer and retailer to be attractively priced with a solid balance sheet and dividend potential.

“Based on the current share price, we forecast an average dividend yield of 5.5% over the next five years,” Atkins says, “with solid longer-term dividend growth as earnings recover. Dividends should be mostly franked except for during the next two years as historical tax losses reduce tax payments.”

Spark Infrastructure owns 49% interests in three electricity distribution companies: Powercor, servicing western suburbs of Melbourne; CitiPower, servicing Melbourne's inner suburbs and central business district; and SA Power Networks, servicing South Australia. Powercor and CitiPower are collectively known as Victoria Power Networks. It also owns 15% of TransGrid, the main electricity transmission network in NSW. Atkins says that while Spark pays healthy distributions it is heavily regulated and faces a tough outlook as the Australian Energy Regulator seeks ways to reduce utility bills.

Lex Hall is Content Editor for Morningstar Australia. This article is general information and does not consider the circumstances of any investor.

Full reports and a free trial with instant access are available on Morningstar Premium at this link, including the portfolio management service, Sharesight. Premium includes Morningstar research on hundreds of stocks, both Australian and global. Firstlinks is a Morningstar company.

Try Morningstar Premium for free