Intergenerational bickering continues and with over 50% of voters in the Gen Z and Millennial cohorts, Canberra is listening to the grievances from young Australians.

Allegra Spender the independent member for Wentworth released a 75-page tax reform white paper and Treasurer Jim Chalmers has announced there will be significant tax changes included in the budget.

Proposing bold plans gets media attention but that doesn’t mean radical change is the best way to address concerns in different parts of the electorate.

The generational dispute

For young voters the narrative is clear. Housing prices are being boosted by entrenched tax incentives that benefit older homeowners while pricing new homeowners out of the market.

Meanwhile stubborn inflation and stagnant wages are lowering living standards while assets overwhelmingly owned by older Australians continue to appreciate.

Conversely, older generations feel attacked for simply having done the right thing by saving, investing and building equity in their homes. Now the rules are being changed after they’ve gone down a prescribed pathway.

On better days it is an informed debate about the best approach. On other days selfish and lazy are lobbed back and forth between younger and older Australians.

Firmly entrenched in middle age I can understand and sympathise with the frustration of both sides. As an incrementalist at heart, I’m less inclined to support radical changes to tax law. Given the complexity of incentive structures these radical changes often prove counterproductive.

I’ve proposed three changes that could help over the long-term and might assuage some of the generational anger as conditions change. However, none of these changes will address the source - property prices.

For many young people my proposal won’t be enough. But the only way to make housing more affordable is to make a concerted effort to lower prices. That takes a good deal of political will, and as New Zealand has demonstrated a recession will likely follow. A long recession won't help any generation.

Index income taxes

The age pension and the general transfer balance cap for super pensions are both indexed to inflation. This makes sense as it protects retirees from rising prices and maintains the inflation adjusted value of one of the central tax benefits of super.

What isn’t indexed to inflation are the marginal tax brackets that determine how much working Australians get to keep from their salaries. Even if salary growth keeps up with inflation working Australians are worse off on an inflation adjusted basis.

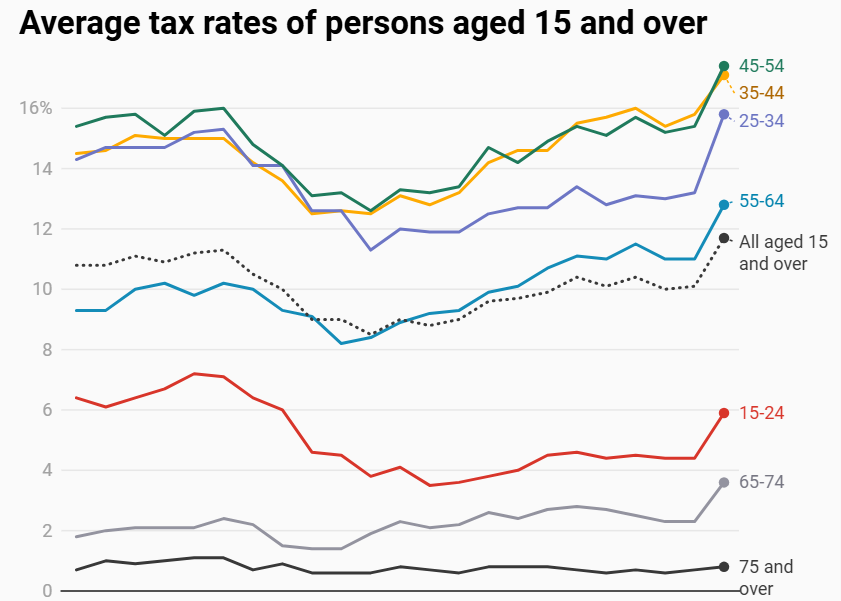

Bracket creep disproportionately impacts Australians that are in the prime of the careers with 35- to 54-year-olds paying the highest average tax rates.

The following charts shows the average tax rate between 2001 and 2023 from the Household, Income and Labour Dynamics in Australia (HILDA) survey.

Not having marginal tax rates indexed to inflation provides two benefits to the government. It is a stealthy way of increasing government revenue without announcing new taxes. It also provides the ability to announce ‘tax cuts’ which are popular with voters even if they are simply retrospective corrections for bracket creep.

Since 2011 successive governments have chosen to use salary inflation to increase revenue. There has been a steady increase in the average tax rates despite three ‘tax cuts’ which occurred in 2012 / 2013, 2020 / 2021 and 2024 / 2025.

Against this backdrop of bracket creep wages are growing slower than inflation – especially for private sector workers whose wage growth has fallen behind the public sector.

Does indexing solve all the issues? Not even close. But it is a simple step that applies a consistent approach to working age and retired Australians. It also aligns Australia with the globe as 60% of of OECD countries have indexation built into their tax laws.

Rental protections

The focus of much of the generational anger centres around housing. I recently covered the folly of trying to make housing more affordable without resorting to policies designed to bring house prices down. A deliberate attempt to reduce property prices is politically perilous which makes it unlikely anything meaningful will happen.

Stronger rental protections could be an easier way to enact a middle ground measure. Many Australians view housing as a pathway to building wealth but home ownership also provides peace of mind and security. Many renters have less financial security and protecting them is worthwhile.

I don’t ever envision Australia looking like Germany where over half the population rents but caping annual rent increases and facilitating longer term leases could bring more security to many Australians.

Eliminating negative gearing is popular with a portion of the electorate. While this may lower property price appreciation it would likely result in higher rents. Adding stronger rental protections is a way to support the most vulnerable Australians in exchange for the benefits already bestowed on investment property owners. This seems like a compromise that many Australians would back.

Grandfathered changes to the age pension

The age pension is vital to the welfare of many retired Australians. Today’s retirees didn’t have compulsory super for much of their careers and I’m not suggesting making changes for any current retirees or anyone close to retirement.

However, at this point compulsory super has been around for 34 years. It took years for the contribution rate to become meaningful but as the next generation retires, there is the opportunity to change the eligibility criteria for the age pension. Announcing changes early will allow people to plan adequately for retirement.

The change I’m suggesting is to no longer ignore the value of the primary residence in the means test for the pension. In a country where so much wealth is tied up in housing it makes little sense to completely exclude the primary residence from the means test.

There are several ways this could be done. Only a portion of the value of a primary residence above a certain value could be included in the means test and provisions could be made based on the property prices in the area a house is located.

The goal should be eliminating the perverse incentives where wealth remains trapped in homes during retirement while taxpayers foot the bill for day-to-day expenses of retirees. Those homes are then passed tax free to heirs.

In some cases the exclusion of housing in the age pension means test is part of an estate planning strategy. The financial advice industry provides guidance to this end. This is legal but changing the incentives can lead to better outcomes for the country.

Retirees have contributed years of taxes to fund the pensions they are collecting but as a society we all need to determine if there is a better way to spend the $65 billion that goes to the pension annually. The age pension is the second largest government expenditure and makes up nearly 8% of the budget.

I know this is a bitter pill to swallow for many and this is the most extreme of the policy changes I’ve proposed. The goal is not to take homes from people but instead to recongnise the value of the wealth held in homes and extract it to support retirement through measures like a reverse mortgage.

If done thoughtfully it can be used to lock in other parts of the retirement system like the current tax incentives in superannuation which are in the political crosshairs.

There are two ways to lower the disparity in tax rates across the age spectrum. One is to raise taxes on super, eliminate negative gearing and increase capital gains taxes. That seems to be the route the government is going down. The other is to find ways to fund tax reductions for struggling working age Australians. To do that in a fiscally responsible way means finding the money to offset tax reductions. The age pension is one way to do that.

Final thoughts

Not everybody will agree with what I’ve proposed. Any change in government policy generally favours some voters and disadvantages others. That is just life.

The longer the status quo persists which a major portion of the electorate deems untenable the more radical the eventual policy response. Now is the time to start taking steps to address the grievances of young Australians.

Mark LaMonica, CFA, is Director of Personal Finance at Morningstar Australia.