Every retirement financial plan includes a variety of assumptions, as nobody knows what life will throw at them. Retirement often comes with the added uncertainties of a loss of income from work, ongoing health problems and greater flexibility in using time. In a world where headlines prefer gloom over optimism, retirees face perhaps 30 years of investing not knowing the returns or risks they face. However, while ‘failing to plan is planning to fail’ is an exaggeration, a long-term plan can draw on the past to make more informed decisions.

Each year, Vanguard releases an Index Chart which shows the performance of major asset classes over the previous 30 years. It is an appropriate period for retirees and advisers to judge long-term investing plans and outcomes as it also coincides with the likely period of retirement.

Balaji Gopal, Head of Financial Adviser Services at Vanguard Australia, says:

“While investors shouldn’t rely on past performance, 30 years of market history has proved that the impact of geopolitical, economic and social events on performance is usually short-lived, and markets will typically recover and rise over time. Looking back over the last few decades, bear markets on average last only 0.9 years and are generally followed by a bull market, averaging 6.5 years. Investors who stay invested through downturns are therefore best poised to benefit when markets inevitably bounce back.”

Let’s first look and how long people are likely to live then check the asset performance numbers.

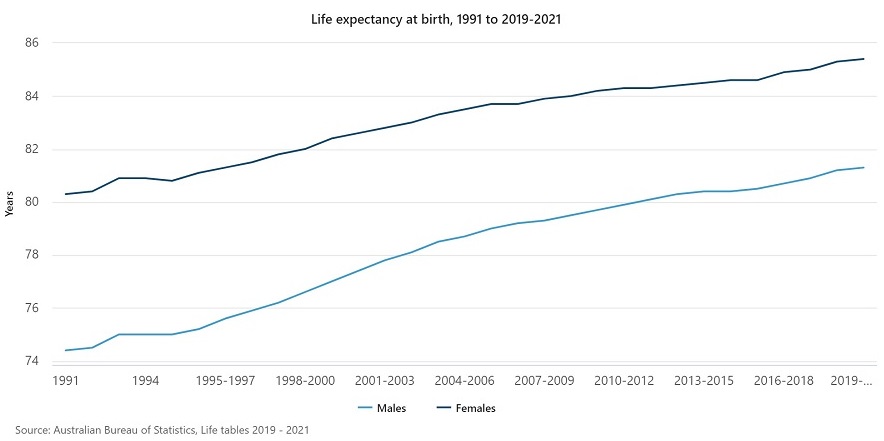

Life expectancy at 65 is not the same as at birth

There is a common misunderstanding about life expectancy as quoted in the Life Tables issued by the Australian Bureau of Statistics (ABS). The latest ABS release shows life expectancy at birth is:

- In 2021, 81.3 years for males (in 1991, 74.4 years), and

- In 2021, 85.4 years for females (in 1991, 80.3 years).

In the 30 years since 1991, the gap between male and female life expectancy has narrowed from 5.9 years to 4.1 years. Males are living 6.9 years longer than in 1991, rising at the rate of a year of life expectancy for every four to five years. Perhaps add another seven years of life expectancy over the next 30 years, although diet and the pandemic may compromise long-term trends.

But these numbers are life expectancy at birth, while life expectancy generally is defined as:

“The average number of additional years a person of a given age and sex could be expected to live, assuming current age-sex specific death rates and experienced throughout their lifetimes.”

Here’s the common mistake. The ages above should not be used when planning the retirement spending and savings of a couple retiring at age 65. They have the benefit of not dying between the ages of 0-65, and the relevant statistics for them are life expectancy at age 65. A male aged 65 is not expected to die at age 81 nor a female at 85 and anyone planning for only 16 to 20 years of retirement is likely to underestimate.

How long will most people spend in retirement?

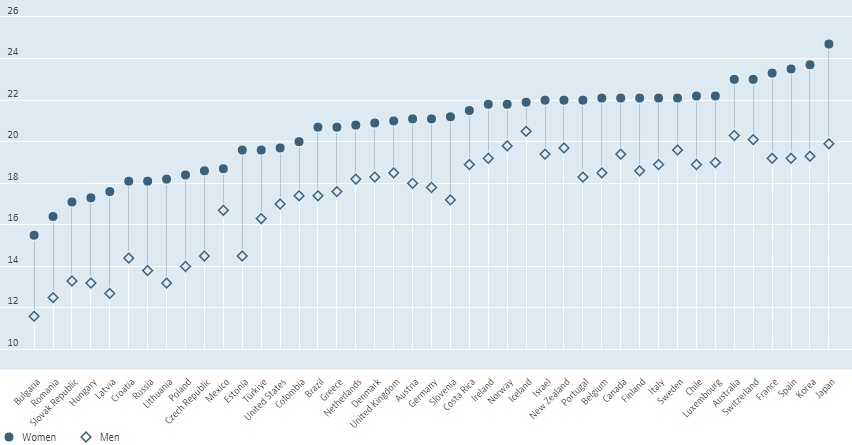

The latest OECD statistics for life expectancy at 65 show Australia is near the top for both men and women, in a group of six at least a year ahead of other countries. The longest, as shown below, are Japan, Korea, Spain, France, Switzerland and Australia. The y-axis is number of years of life expectancy at 65.

For Australia, the statistics for life expectancy at age 65 are:

- Men, 20.3 years

- Women, 23.0 years

Which suggests men will live to about 85 and women to 88 on average.

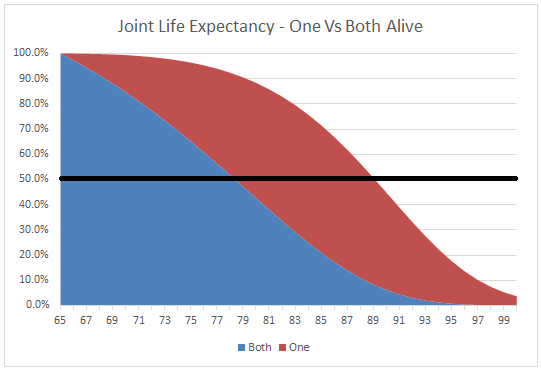

But that’s half the story. Life expectancy is based on the 50th percentile, meaning there is a 50% chance of living beyond the average. Plus most people enter retirement as a couple sharing income and expenses rather than as two individuals. Life expectancy plans for a couple need to head towards the ages of 95 to 100, as shown in the following table (based on US data) by Michael Kitces, a leading US financial adviser and consultant to the advice industry.

There is a useful overlap between the investment planning horizon for an Australian couple of 30 years after retiring at 65, and the Vanguard data of 30 years.

Retirement planning is not only about savings

A reminder that Australia’s retirement system includes three components, and I argue, a fourth for most people. They are:

- Savings inside the superannuation system

- Savings outside the superannuation system

- Age pension and other social security benefits

- Access to equity in the family home.

A complete picture of all components should be included in any comprehensive retirement plan, bearing in mind there will always be calls for the age of access to the age pension to push out. Recent research includes:

“With protests against raising the pension age raging in France, statistical modelling from the Macquarie Business School suggests Australia’s optimal pension age should be increased to 68 by 2030, 69 by 2036 and 70 by 2050.”

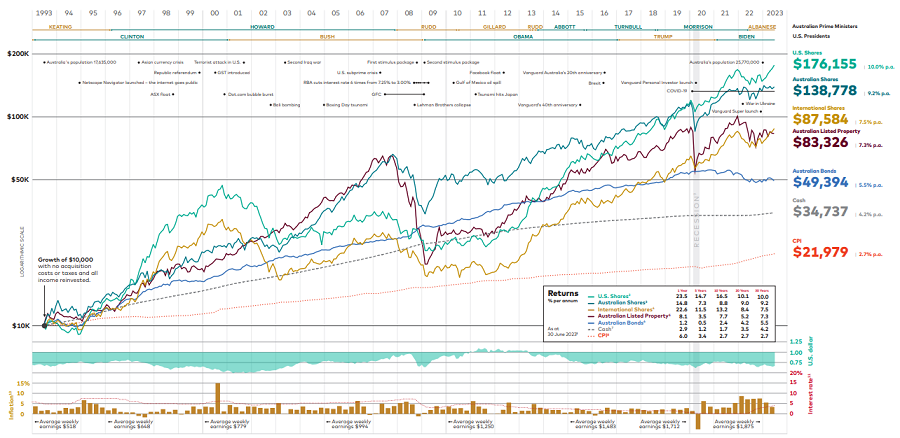

Investment performance over the last 30 years

Over the last 30 years, Australian shares on average have returned 9.2% per annum, with a healthy 14.8% in 2022/2023 in contrast to a sobering -7.4% the previous year. All asset classes except cash delivered negative returns in 2021/2022, including an unusual correlation between equity and bond returns. Defensive assets generally did not provide protection, although usually, diversification reduces market volatility.

Vanguard provides the following chart on the performance of an initial investment of $10,000 invested in the major asset classes, with US shares winning handsomely. In the past, therefore, taking equity risk has been rewarded for those who can tolerate the greater risk, and there is a cost to pay for cash’s defensive qualities. Note these are nominal not real returns, so there is no adjustment for inflation.

The Vanguard chart is detailed, click here to view or download a larger version.

|

$10,000 invested in 1993

|

Accumulated investment value at 30 June 2023*

|

% returns per annum

|

|

Australian Shares

|

$138,778

|

9.2%

|

|

U.S. Shares

|

$176,155

|

10.0%

|

|

International Shares

|

$87,584

|

7.5%

|

|

Australian Bonds

|

$49,394

|

5.5%

|

|

Australian Listed Property

|

$83,326

|

7.3%

|

|

Cash

|

$34,737

|

4.2%

|

*with no acquisition costs or taxes, and all income reinvested. Source: Vanguard

Check the fees

As a major provider of funds based on various indexes, Vanguard makes the case for investing in index funds to reduce costs, but investors should note that Exchange Traded Funds are not all index funds, and neither are managed funds all active. Check the fee and don’t assume ETFs are always cheap as some are actively managed with high base and performance fees.

For example, Morningstar data on Australian ETFs, as shown in the table below, shows the weighted average cost of passive (index) ETFs is 0.24%, while active ETFs are at 0.65%. The simple average (all funds given equal weight regardless of size) is 0.92% which shows some active ETFs are as expensive as managed funds.

Fee Comparison for ETF Cohort

|

ETF Cohort

|

Simple Average

|

Asset Weighted Average

|

|

Pure Passive ETFs

|

0.44%

|

0.24%

|

|

Strategic Beta ETFs

|

0.43%

|

0.36%

|

|

Sustainable ETFs

|

0.57%

|

0.48%

|

|

Active ETFs

|

0.92%

|

0.65%

|

Source: Morningstar Direct, Morningstar Research. Data at 31 December 2022.

Would you bank these returns for the next 30 years?

Given the chance to earn these returns for the next 30 years, how many investors would say earning 9-10% (in nominal terms, not adjusted for inflation) on their equity portfolio throughout retirement is adequate and bank that level now? It’s my guess that the vast majority would accept. I would, but the numbers come with the benefit of only considering the handsome 30-year returns and not the volatile journey endured to get there, including losing half the value of shares during the GFC.

A qualification is that there are always reasons to argue future returns will be lower. We could now say that past returns benefitted from cheap energy while the future of energy transition will cost trillions, that past Chinese growth will be replaced by a stagnating economy, that the Ukraine war will disrupt for years, that demographic changes and an ageing population will hit growth, etc, etc. But stockmarkets have delivered opportunities for centuries, and the more optimistic outlook is to place faith in the ingenuity of people to solve problems.

Most retirees find the volatility of a 100% exposure to equities unacceptable, so some mix into other asset classes is required to manage the risk. The results show that staying invested for the long run is likely to be rewarded, although investing broadly and diversifying is a safer route.

Graham Hand is Editor-At-Large for Firstlinks, and this article is general information and does not consider the circumstances of any investor.