The conflict in the Middle East, along with developments in artificial intelligence and its potential impact on existing business models, has led to a repricing of many securities in recent months, particularly in mid and small capitalisation companies.

Following several years of strong performance, the mood has changed from optimism to extreme pessimism, which is being reflected in valuations. But not all companies will be impacted in the same way, and we see opportunities for investors willing to do their due diligence and thorough company research.

A market divided

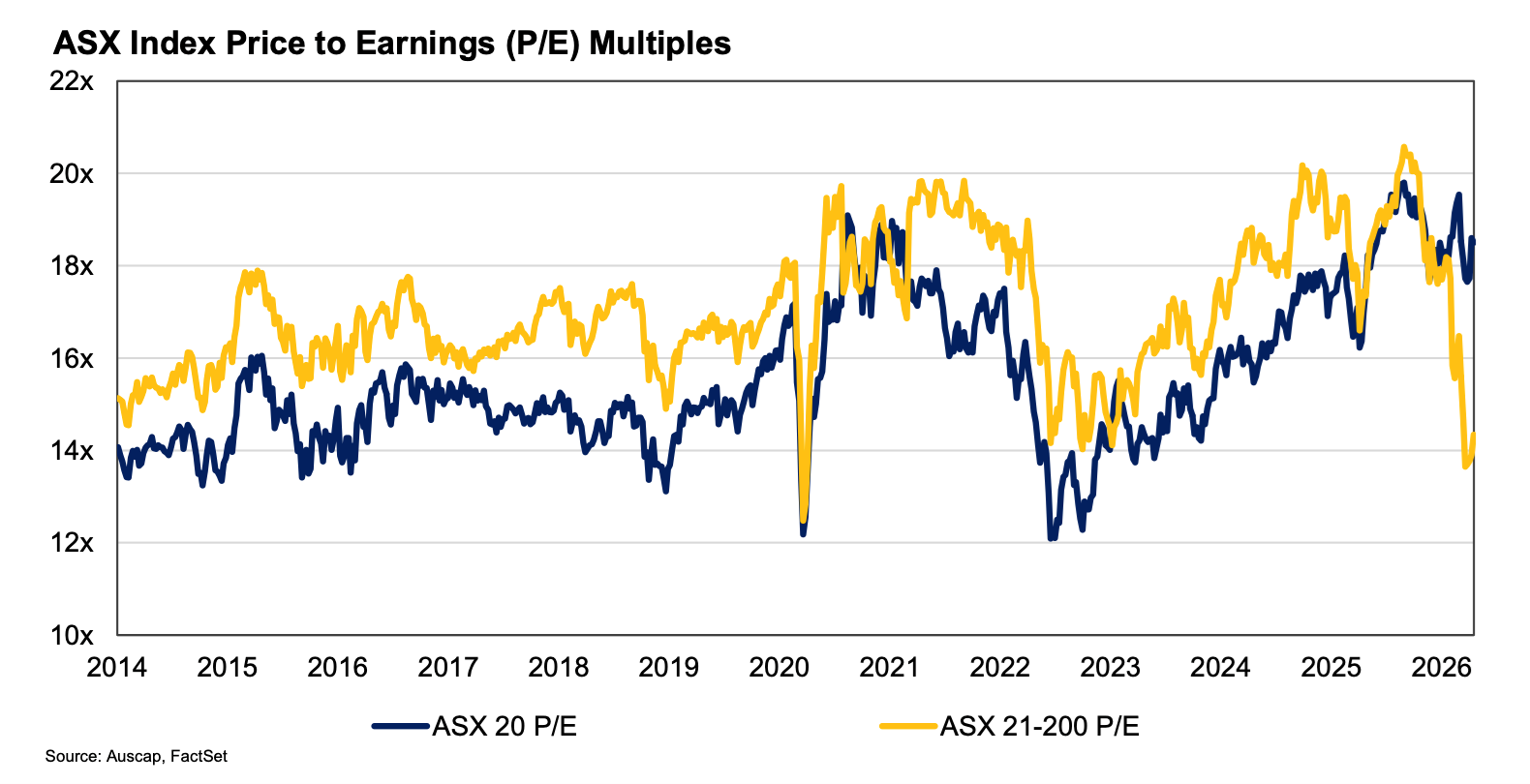

The market has certainly become bifurcated in 2026. But larger Australian companies have been less price sensitive to recent developments than the rest of the local share market.

The 10 largest companies in the S&P/ASX 200 by market capitalisation now account for 49.1% of the S&P/ASX 200, while the 20 largest companies (the S&P/ASX 20) account for 63.3%. The S&P/ASX 20 has been, until recently, trading on a near record multiple of one year forward earnings, as seen below.

In contrast, the smallest 180 companies in the S&P/ASX 200 are trading on a forward price to earnings multiple that was last seen very briefly during the COVID-19 panic of 2020.

This is also a reversal of trend as historically the companies outside the S&P/ASX 20 have traded on a higher multiple of earnings than the companies in the S&P/ASX 20.

This likely reflects the expectation that these businesses will deliver greater earnings growth over time than their larger counterparts. Over the past decade the S&P/ASX 200 has delivered earnings per share growth of 0.8% per annum. The companies in the S&P/ASX 200 excluding those in the S&P/ASX 20 have delivered earnings growth of 4.9% per annum.

It is difficult to argue that the continued resilience of the largest companies in the market is based on a superior earnings outlook. We would suggest that the recent and ongoing trend towards passive investing results in capital flowing into companies according to their current size, rather than the prospects for the business, leading to distortions as to how companies are priced.

This is only exacerbated by investor and regulatory pressure for institutional managers to not underperform their benchmark which leads to index replication. This has prompted some of the largest, and most sophisticated, pools of capital in the Australian market to move toward passive investing.

Where are the opportunities?

One factor that has led to lower multiples over the past few months is concerns around developments in artificial intelligence. Artificial intelligence has the potential to upend established business models.

The combined market capitalisation of technology related businesses assumed to be at risk from these developments fell from over $200 billion to less than $100 billion in just a few quarters from mid-2025 to early 2026.

But not all technology-based businesses will face the same level of risk, and we think this indiscriminate selloff is creating opportunities. To work out whether a business is exposed, investors need to understand the nature of the economic moat that allows the business to generate strong returns on capital compared to peers. If this is simply a technological solution to a problem, the value of that solution may well be diminished by technological replication at low cost.

But there are many technology related businesses where the technology is not the ongoing and only source of competitive advantage. It may be a key part of the offering, but it no longer represents the sole reason the business is able to generate superior returns on capital compared to peers.

The opportunities for investors therefore are in finding businesses that have seen their share price fall, but for which the chances of disruption appear overstated based on current information.

These kinds of companies may include:

- Businesses that operate in highly regulated markets and/or are systems of record

- Businesses with valuable proprietary data that cannot be scraped or replicated

- Two-sided marketplaces with strong network effects where benefits flow from the aggregation of buyers and sellers

- Businesses that are deeply integrated in client workflow where the risks of error outweigh the potential cost savings, particularly where the technology is adjacent to the product/service, and

- Relationship based industries where the human contact is likely to be an important ongoing feature for clients.

Companies that we believe show some of these characteristics include CAR Group (ASX:CAR), REA Group (ASX:REA), Life360 (ASX:360), and AUB Group (ASX:AUB).

Are there large caps at risk?

In terms of large company valuations versus small, we think the outlook over the next decade for some of the largest domestic companies is increasingly challenged.

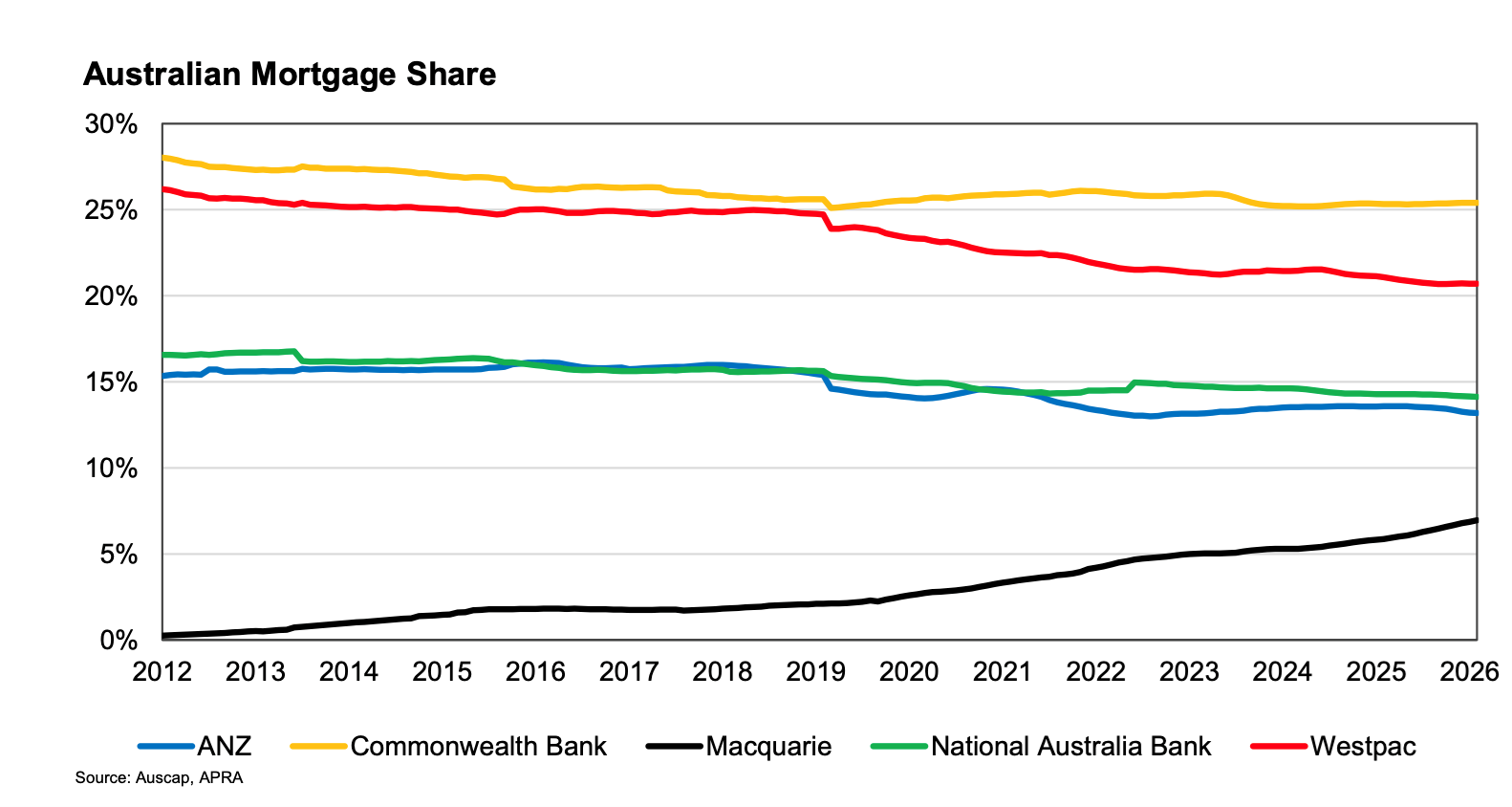

The financial sector is a good example of this. The largest four domestic banks, Commonwealth Bank, Westpac, NAB and ANZ, account for 23% of the S&P/ASX 200. But they are likely to be increasingly challenged by Macquarie, especially in the mortgage market.

Macquarie is in the unusual position of having a natural competitive advantage despite being the challenger. It has a modern technology stack based on one data platform, a streamlined online-only business model with no legacy branch network costs, and a much lower cost, scalable business model compared to the majors. This is enabling Macquarie to offer considerably better value to both deposit holders and borrowers.

Macquarie’s growth looks set to challenge the revenue and earnings of the major banks in the years to come. That the banks are trading on lofty price to earnings multiples at a time of imminent potential disruption speaks to the weight of capital flowing passively into the market. This situation cannot continue indefinitely and reminds us of the German proverb, “trees don’t grow to the sky”.

Looking ahead

Rather than panic, investors should see the market for what it currently is. There are high quality, competitively advantaged businesses with strong prospects for growing earnings at rates well above the market currently on sale.

Investors who do their research at a company level, and look beyond the largest 20 listed companies, may well be surprised by the long-term returns that can be generated in this environment through patient and rational investing.

Tim Carleton is the Chief Investment Officer and founder of Auscap Asset Management. This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person.