In October 2025, after a string of poor election results, the Liberal Democratic Party (LDP) chose Takaichi Sanae to become Prime Minister - Japan’s first female PM. Within months of her ascent, PM Takaichi went to the people and achieved a staggering result – a supermajority of more than two-thirds of the lower house. We believe her election success could underpin an increasingly confident path forward for Japan.

Japan today faces three key challenges:

- Regaining economic vitality as it emerges from an extended period of deflation

- Managing geopolitical challenges including tension with China

- Long term demographic headwinds.

Takaichi PM recognises these issues are best addressed by creating incentives for the private sector to invest and raise productivity. Her reformist policies are pro-business, with focused fiscal stimulus and a dovish approach to monetary policy.

Growing Japan’s economy

Upon her appointment, Takaichi PM wasted little time, announcing a capable cabinet and several councils that are pursuing a growth agenda. Her government has unveiled reform proposals designed to encourage higher corporate capex, such as tax incentives for growth investments and R&D. These incentives set return hurdle rates of 15%, so should promote genuine growth.

To help secure supply chains, Japan’s Growth Strategy Council announced a roadmap for public and private investment in 17 strategic areas including shipbuilding, aerospace, quantum computing, fusion energy, automation and AI.

Most notable is a decision to increase Japanese defence spending. The Takaichi government has committed to raising this to 2% of nominal GDP by the end of FY25 with a potential further increase to 3%. We think these policies are an evolving response to a more unpredictable geopolitical environment and mirror similar increases seen in regions like the EU.

Increased spending should generate new earnings for Japanese defence equipment companies. Indeed defence companies were one of the key beneficiaries of the ‘Takaichi trade’ – the jump back to a record high for the Nikkei 225 straight after the election result. It’s in defence that PM Takaichi is most likely to use her new supermajority to seek constitutional reform.

Japan is back

Takaichi PM’s critics have their concerns. They question how Japan will fund its investment commitments and election promises (including consumption tax cuts) given already elevated government debt. We believe these debt concerns have been overblown in the past and do not see any hurdle to Japan financing its plans.

Intriguingly, Takaichi has said that Japanese corporations should focus on raising wages rather than shareholder returns.1

Recent corporate governance reforms championed by the Tokyo Stock Exchange encouraged companies to reward investors with share buybacks and improved dividends. Japan’s listed companies could pay out 20 trillion yen (US$127 billion) in dividends for the year to March 2026 – double what they paid ten years ago.2 This has been a key driver of Japan’s strong stock market. But do Takaichi’s comments signal a backpedaling on the governance reforms so crucial to Japan’s recent strong sharemarket performance?

Durable growth?

In a word, no. That Rubicon has been crossed and strong corporate governance is now a feature of Japan. It is uncommon to find corporates that do not take their governance obligations seriously. We think corporates will increase business investment, focusing on productivity, growth and business resilience, but not at the expense of shareholder returns.

As we’ve written before, the higher shareholder returns seen in recent years are but a prelude to the main event, namely a deep-seated reconfiguration of Japan’s industrial structure that could underpin prosperity for decades to come.

In our view, shareholder returns delivered without a long-term competitive vision are counterproductive. Therefore, boards should return excess capital to shareholders only if they can’t find compelling opportunities to invest in future growth.

We welcome higher returns, but we prefer to see firms use their capital to secure long-term growth to restructure their business portfolios, secure supply chain resilience and retrain their workforce. We think this is how Takaichi’s comments should be interpreted.

The technology opportunity - AI with fingers

As AI technologies mature, they can be deployed productively across Japanese enterprises, offsetting labour shortages and addressing bottlenecks. Production methods can move from manual to automated. This will require substantial amounts of R&D - and ingenuity.

Here we are upbeat about Japan’s prospects, given the industriousness of Japan’s workforce. Innovation drove Japan’s economic development in the 20th century, and we expect this century to be no different. Already we are seeing promising signs that the reshoring of manufacturing has begun, implying a new virtuous cycle of capex, job creation and higher wages.

In short, the first stage of the “Japan comeback” is now ending. The newer phase - a more innovative Japan - offers the prospect of both higher and more durable growth. And that’s good news for investors.

Morning in America meets the Rising Sun

President Trump visited Japan just a few weeks after Takaichi Sanae’s elevation to PM. Japan extended a warm welcome and in return Trump confirmed closer economic and security ties (as well as acting as a booster for Takaichi during her campaign). We have written previously around how the US/Japan relationship is mutually beneficial, matching Japanese manufacturing know-how with the US drive to rebuild their manufacturing base and boosting economic growth for both countries.

The mammoth U.S./Japan Strategic Investment Initiative, whereby Japan will invest $550 billion in US industry, is especially promising. Encouragingly, discussions are already underway on joint projects.

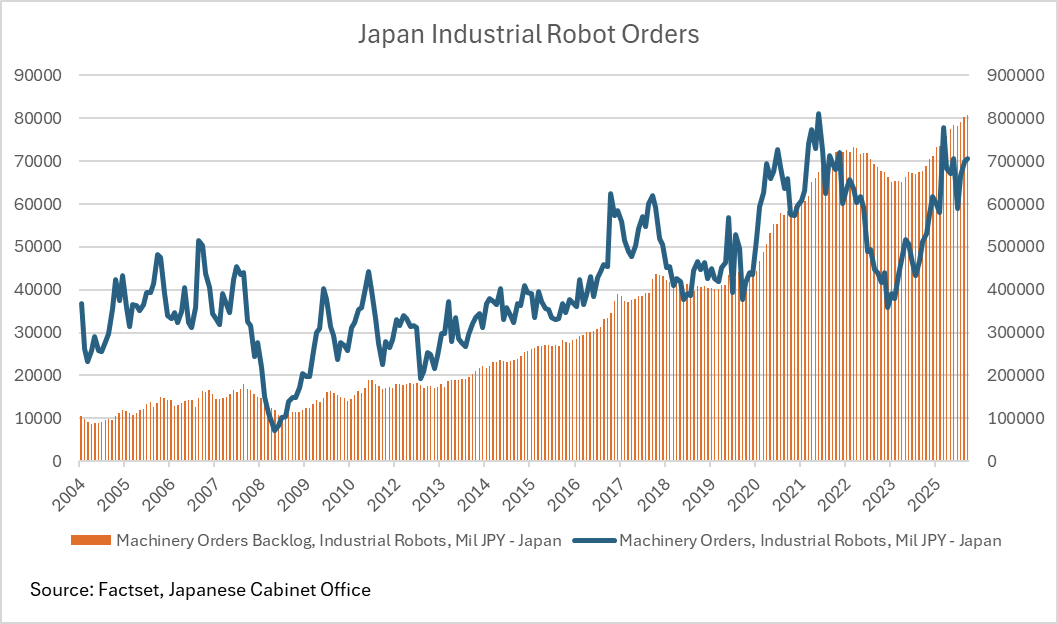

Japan has formidable manufacturing technology, particularly in precision applications like factory automation and robotics. (The chart below shows the growth in demand for Japan’s industrial robots).

Many commentators believe attempts to rebuild US manufacturing will flounder because the skills of its manufacturing workforce have deteriorated after decades of neglect due to offshoring. Some argue the US private sector doesn’t want to invest in manufacturing, preferring to fund higher return, capital-light sectors such as software.

We are more optimistic. Fortunately, Japan has an abundance of capital seeking investment, thus offering the US the funding and skills required to revive a competitive manufacturing base.

AI could play a crucial role. Today the beneficiaries of the AI boom tend to be makers of semiconductors and chip production equipment. The next phase could be deploying the rapidly improving capabilities of AI into real world applications - ‘physical AI’ – such as AI-enabled robotics and automation that augment or even replace human labour.

In early December, FANUC, the world’s pre-eminent maker of industrial robots and a key Platinum Japan Fund holding, announced a physical AI partnership with Nvidia and unveiled new open-platform, AI-enabled industrial robots that understand human language. We could be on the cusp of a new industrial revolution as physical AI pushes up industrial productivity while generating dramatically higher returns on investment.

A new competitive advantage for Japan

The implications are profound. Advanced manufacturing built on AI and robotics works for a Japan that has a shrinking labour force. For the US, it also removes a large part of the cost disadvantage of local supply chains. That upends one of the most potent arguments for offshoring to countries like China.

This move to reshore advanced manufacturing – and all the productivity gains and supply chain resilience it offers – is exactly what the US-Japan initiative is designed to encourage. This shift should boost growth at Japan’s leading companies and, with a pro-reform government equipped with a large majority, suggests to us that Japanese equities could be a good home for investors’ capital in the second half of the 2020s.

1. Shareholder returns includes dividends, share buybacks and capital gains.

2. See https://asia.nikkei.com/business/markets/japan-inc.-dividends-to-top-20tn-yen-for-1st-time-nearing-40-of-profit.

Leon Rapp is a Portfolio Manager – Japan strategies at Platinum Asset Management. This information is commentary only (i.e. our general thoughts). It is not intended to be, nor should it be construed as, investment advice. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Before making any investment decision you need to consider (with your financial adviser) your particular investment needs, objectives and circumstances.