Before the last Federal election, the Firstlinks pages were filled with policy discussions and articles generating hundreds of comments. Labor ran a large target agenda including negative gearing, capital gains tax, family trusts and franking credits. The Labor Shadow Treasurer, Chris Bowen, was so confident of election success that he responded to a question on ABC Radio on franking credits in a way he would live to regret:

"I say to your listeners, if they feel very strongly about this, if they feel that this is something which should impact on their vote, they are of course perfectly entitled to vote against us."

Any new policy has its losers who are easy to whip up into a frantic opposition. Labor policies were badged as 'retiree taxes' and 'death taxes' with fears they would destroy property values. Elections are more marketing that substance and messages on repeat, repeat, repeat. The days when governments worried about raising revenues to meet spending objectives are gone with structural deficits now stretching on forever.

Anthony Albanese would be in a lot better position today if one of his advisers had tucked this Reserve Bank graphic into his shirt pocket on Day One of the campaign.

Who can blame Labor for now avoiding controversy, supporting the handout Budget and keeping their heads down after nine years in opposition? We get what we deserve and voters don't reward policy bravery. This painful campaigning period until 21 May will be dominated by character assassinations and more handouts rather than meaningful policies, and it's hard to see how such politicking does not lead to more division.

With unlimited sources of news, we all choose our favourites, and with that comes confirmation bias. We filter out information inconsistent with our beliefs. If you watch ABC current affairs, read The Guardian and Sydney Morning Herald/The Age, subscribe to Crikey or Michael West Media, then you may think Labor is certain to win the election (at least before Albo forgot a couple of key statistics). But spend a day listening Ray Hadley on Radio 2GB, watching Sky News at night or reading The Daily Telegraph and you'll see how the other half thinks. Our carefully-chosen social media feeds and friends make it worse.

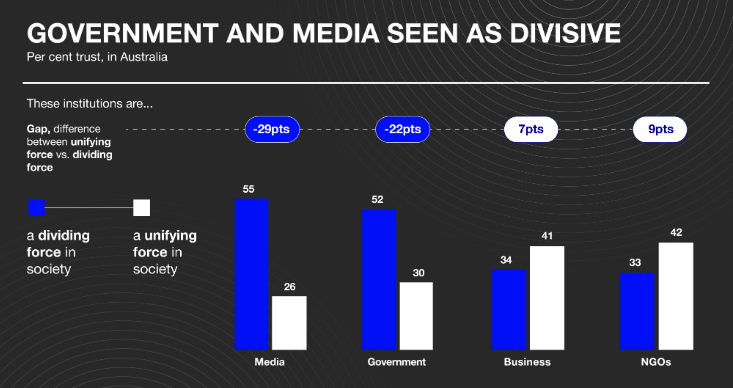

Each year for Australia, Edelman publishes a Trust Index, which this year shows most Australians see media (55%) and government (52%) as divisive rather than a unifying force. It's wishful thinking to believe there is momentum in the other direction.

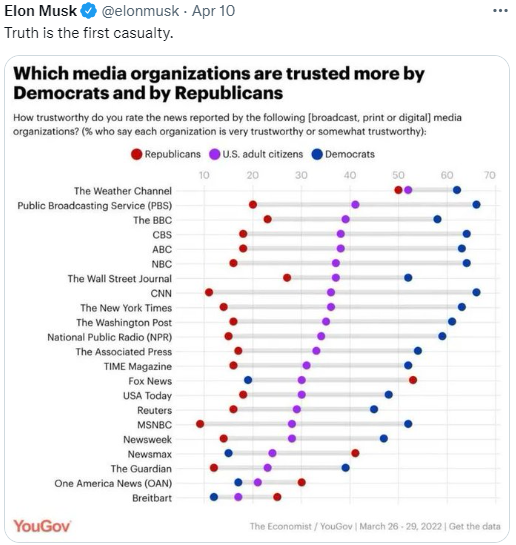

In the US, the divide between Democrats and Republicans in trust of media organisations is staggering. It's reached the point where people need to know the politics of their countrymen and what they watch before they can have a decent conversation. Is Australia heading this way, or are we already there?

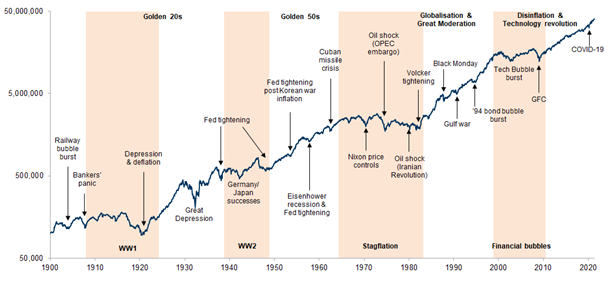

Back to investing, the impending rise in cash rates has already fed into longer-term rates, challenging portfolio construction techniques in a way we have not seen for a decade or more. The traditional 60% growth / 40% defensive portfolio has become a standard asset allocation and has paid off well since the GFC. However, as Goldman Sachs research below shows using US data, there are periods since 1900 when 60/40 in real terms delivered poor returns, shown in orange shading. The good times usually end after a strong run for equities and high valuations relative to history.

Real total returns of 60% equities/40% growth portfolio in the US

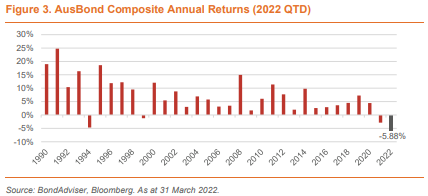

In recent years, investors who rely on the cash flow from their investments for income to live on were forced to take on more risk in equities or be satisfied with 1% on term deposits and draw down their capital. Now that's changing, and a quality bond portfolio can deliver around 5% with careful credit selection or via a bond fund. But rising rates hit fixed income portfolios that are revalued, such as bond funds, with the AusBond Composite Bond Index returning its worst loss for at least 30 years in the first quarter of 2022, and the first loss of any amount since the turn of the century.

The Roy Keenan article makes a case for floating rate exposure during rising rates, while the White Paper from IAM explains more about the 5% opportunity and shows how to judge the price risk due to a 1% rise in rates on a range of fixed rate investments.

Graham Hand

Weekend market update

From AAP Netdesk: The Australian share market has notched up solid gains before the Easter long weekend as a continuing momentum in commodity prices helped rally frontline mining and energy stocks. The benchmark S&P/ASX200 index ended 44.4 points, or 0.59 per cent, higher to 7523.4 on Thursday. It recorded a similar 0.6 per cent increase over the shortened trading week and is now fewer than 100 points from its record high achieved last August. The All Ordinaries index rose 50.2 points, or 0.65 per cent, to 7822.2.

Markets across the Asia Pacific region tracked higher on hopes that inflation may be close to peaking, and amid aggressive rate increases by major central banks in recent days. Economists expect the Reserve Bank to join the action with its first cash rate increase in June. That forecast was underlined by data on Thursday that showed unemployment stuck at 4.0 per cent, against market expectations of 3.9 per cent. Investors are focused on the first-quarter consumer price data due on April 27, which will show whether Australia's core inflation has climbed above the RBA's 2-3 per cent target band.

Firmer global crude prices due to worries about tight global supply also aided local stocks, with energy again among the top-performing sectors on the ASX.

Woodside Petroleum and Santos both climbed more than 1.0 per cent each, while Viva Energy and Beach Energy rose around a similar level.

The top iron ore miners helped underpin the gains in the materials sector, with BHP and Fortescue Metals each rising more than 1.3 per cent. They received a boost from China's announcement that authorities would cut banks' reserve requirements soon to support the COVID lockdowns-battered economy.

Travel stocks also flourished on hopes of an improved outlook after US airline Delta Air said strong demand was providing enough pricing power to make up for soaring fuel costs, sparking a rally in airline stocks globally. Qantas shares jumped 7.1 per cent to $5.45 while Corporate Travel management, Flight Centre and Webjet were up 5-7 per cent.

However, the heavyweight financials sector bucked the trend. Each of the big four banks ended in negative territory, with sentiment soured by Bank of Queensland's results. The Brisbane-based regional lender underlined the pressure on earings in the sector, reporting a decrease in its net interest margin by 12 basis points to 1.74 per cent, amid ongoing competitive pressures and higher fixed-rate lending volumes. The stock ended 6.3 per cent lower at $7.99.

From Shane Oliver, AMP Capital: Global share markets fell over the past week with concerns about inflation and monetary tightening continuing to weigh. For the holiday shortened week US shares fell 2.1% and Eurozone shares fell 0.2%. Chinese shares remained under pressure from concerns about covid related lockdowns. Australian shares rose 0.6% though with strong gains in utilities, resources and consumer staples. Bond yields continued to rise. Oil and iron prices rose, but metal prices fell slightly. The $A fell back to nearer $US0.74 as the $US rose.

Shares remain at risk in the short term, but providing US, global and Australian recession can be avoided a deep bear market should be averted enabling them to be higher on a 12-month horizon. Increasingly hawkish central banks in the face of high inflation, high bond yields, continuing uncertainty around the war in Ukraine, the risk (albeit less than 50%) of a Le Pen win in the French election and the return of possible tax hikes in the US to fund a slimmed down Build Back Better program ahead of the US mid-terms all risk making for a volatility short term ride in share markets, However, past experience tells us that if recession is avoided falls in shares should be limited and the broad trend will remain up. While Europe is most at risk of recession so far our European Economic Activity Tracker is still rising. In the US the 10yr/2yr bond yield curve has steepened again and even if it does go back to being inverted and other versions of the yield curve invert the lag to recession in the US from such an inversion has historically averaged around 18 months which takes us to late next year which is too far away for share markets to get too worried about just yet. And in Australia there is no sign of recession.

***

Also in this week's edition ...

Arian Neiron founded VanEck in Australia nearly 10 years ago, and has since introduced 30 ETFs to their suite, ranging from broad market indexes to themes and sectors. What makes the range different is a background forged in active management, but how does he select funds, which are his favourites and which does he expect to do well in 2022?

An investor named Wesley Gray created what he called ‘God’s portfolio’ which invested exclusively in the top decile of stocks based on their performance over five years. Over the 90-year investment horizon, God’s portfolio compounded at more than 29% per year yet endured the pain of drawdowns that exceeded 20% on ten different occasions. Chris Demasi writes that this is a reminder while sell-offs and drawdowns are difficult experiences, a long-term view is a critical component of being a successful investor.

Andrew Mitchell also explores market volatility by looking back at history and highlighting the journey investors should expect when investing in the share market through the seven laws of volatility.

Against a backdrop of economic and geopolitical uncertainty, rising inflation and expectations of a rate hike, Australian investors are searching for investments that can benefit from these evolving market conditions. Roy Keenan makes the case for floating rates and that hybrids are just such an investment.

There were many questions and comments on Meg Heffron's last article on future-proofing your SMSF, so this week she covers how to manage some trickier situations.

David Williams has been developing the concept of a National Longevity Strategy, and he shares his thoughts here.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Christine Benz explores four dangerous assumptions that could ruin your retirement. And Morningstar analysts believe Ryman Healthcare's share price selloff is an attractive entry point into a stock that has tripled underlying profit since 2011, writes Lewis Jackson.

We will be taking a break next week for Easter and the next edition will be published on 28 April. Hope everyone has a great Easter break!

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

IAM Capital Markets' Weekly Market Insight

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Monthly Investment Products update from ASX

Plus updates and announcements on the Sponsor Noticeboard on our website