Investors need to take a view on exchange rates in order to make currency hedging decisions on foreign assets in their portfolios. This makes a big difference to portfolio returns. It is possible for even small investors to make currency hedging decisions using Exchange Traded Funds listed on the ASX.

One crucial factor we look at is commodities prices (other factors include relative purchasing power, current account balances, foreign reserves and interest rates differences).

Australia exports rocks and other basic materials to foreigners who use them to make useful things that we then re-import back as manufactured goods at astronomical price mark-ups in terms of dollars per tonne. This is one of the many ways in which Australia is more like an ‘emerging’ market economy rather than a ‘developed’ one. (Australia did once make things out of our rocks, but only while protected from global competition behind high tariff barriers erected after World War 1 and dismantled since the 1980s).

As a result, the AUD has tended to follow the path of commodities prices.

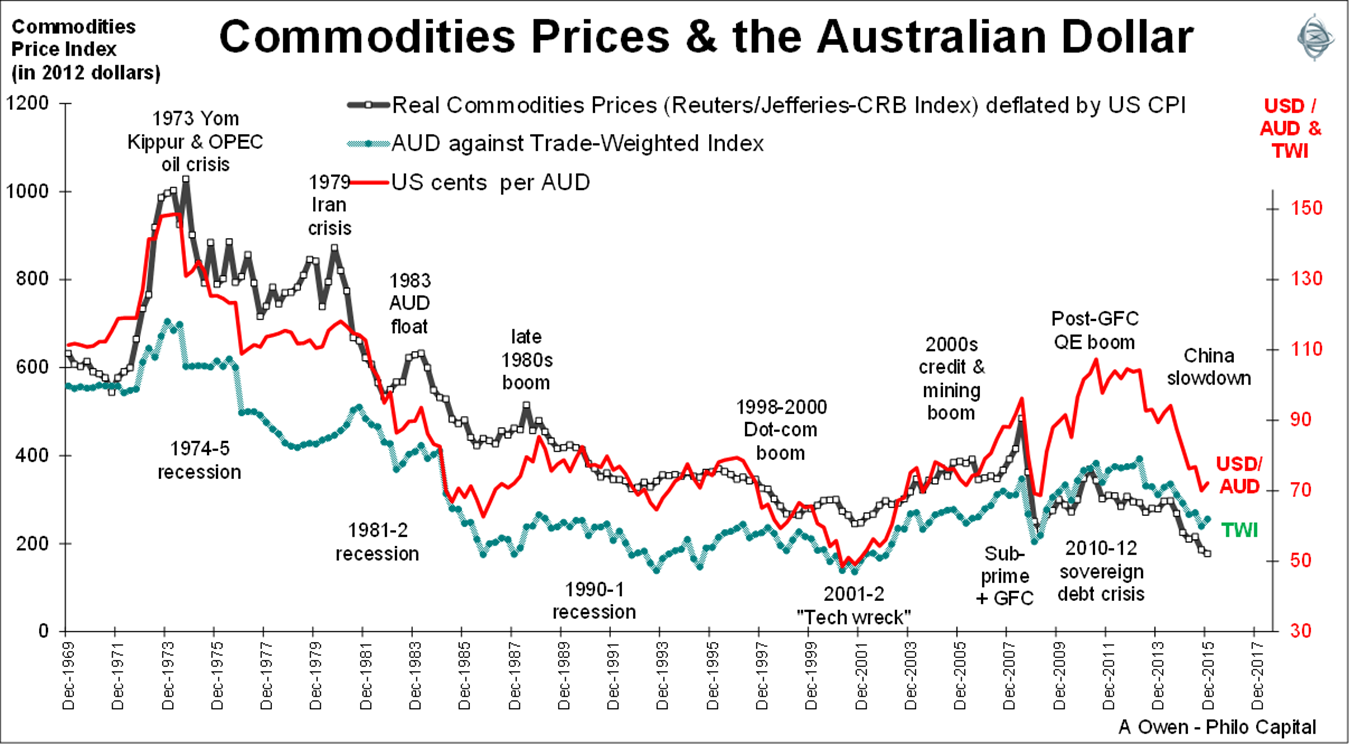

The chart shows a broad commodities price index adjusted for inflation (black line), the USD/AUD foreign exchange rate (red) and the AUD Trade Weighted Index (green) since the late 1960s, when the gold standard started to break down.

The AUD has risen and fallen with all of the major ups and downs in commodities prices over the period. The dollar was at its lowest levels during the ‘dot com’ boom and subsequent ‘tech wreck’ when commodities were considered so out of fashion and so cheap that you almost couldn’t give them away.

Commodities price cycles are more about supply than demand. Demand drifts upward over time as global population and living standards rise steadily, interrupted briefly by recessions. The problem is on the supply side and in particular the long lead times between exploration, mine development and new production (supply) of commodities. These supply cycles usually take a decade or more.

Falling commodities prices during the 1980s and 1990s meant that exploration, mine development and new production came to a grinding halt for a couple of decades.

Demand for commodities was drifting up slowly and then suddenly picked up with the Chinese manufacturing export and urbanisation boom that accelerated with China’s entry into the World Trade Organisation in 2001. The increase in demand from China plus the supply constraints from two decades of little new supply caused commodities prices to sky-rocket, lifting the Australian dollar as well.

Commodities prices and the AUD collapsed briefly in the 2008-09 sub-prime collapse and global financial crisis but then quickly rebounded in 2010. The peak of the commodities/AUD cycle was in April 2011 after the Japanese tsunami.

But every mining boom contains the seeds of its subsequent bust. Rising commodities prices in the 2000s triggered an explosion in exploration, mine development and production. Due to the long-time lags, new supply is only coming on stream now at a time when Chinese and global demand growth is weakening. The huge amount of new supply is crippling commodities prices.

The result is the same as it has been in every past mining boom cycle – prices fall, mining companies collapse, and most of the new holes in the ground are abandoned. It is happening now with iron ore, coal and non-ferrous metals, and we are about to see it in oil and LNG.

(Every boom/bust cycle is different in the details of course. This time around we have two additional negative elements. The first is the huge piles of ultra-cheap debt in many mining companies that will soon need to be refinanced at higher rates. The second is the blow-out in current account and budget deficits resulting from the collapse in commodities prices).

We have been bearish on the AUD (and unhedged on foreign shares in portfolios) since 2011. This has added 30% to returns on global shares since then. Because of the long lags involved in the supply side of mining we are still bearish on the AUD (and unhedged on global shares) as the current global over-production and over-supply of commodities is likely to swamp the modest demand growth for many years to come.

Ashley Owen is Joint CEO of Philo Capital Advisers and a director and adviser to the Third Link Growth Fund. This article is for general education only, not personal financial advice.